CWS Market Review – May 12, 2017

“He that observeth the wind shall not sow; and he that regardeth the clouds shall not reap.” – Ecclesiastes 11:4

Earlier this week, the Volatility Index (VIX) dropped to its lowest level in more than 24 years. The stock market just ain’t doing a lot of moving around lately. Charlie Bilello points out that over the last 13 days, the S&P 500 has traded within a range of 1.01%. That’s the narrowest range for a 13-day period on record.

Overall, the low-vol environment has been very good for stocks. This week, the S&P 500 jumped to yet another all-time high. The bulls were pulling for the index to close above 2,400 for the first time, but it just wasn’t able to cross the finish line. Three times in four days, the S&P 500 closed within a point of 2,400.

Earlier this year, I said that I was expecting a modest pullback in the stock market. Nothing major, but enough to burn some of the momentum players. I’ll give myself partial credit. The market did indeed drop a bit, but not as much as I had been expecting. From March 1 to April 13, the S&P 500 lost a mere 2.8%, while I had been expecting something closer to 5% – 7%. Since April 13, stocks have been quite strong.

I have to admire the market’s resiliency, and our Buy List continues to do very well. In this week’s CWS Market Review, I’ll cover the good earnings reports from Cognizant Technology and Moody’s. We also had a 20% dividend increase from Wabtec, a company that’s quietly turning itself around. Later on, I’ll preview next week’s earnings report from Ross Stores, one of the best retailers around. But first, let’s look at the recent jobs report, and upcoming (mistaken, in my opinion) Fed rate hike.

The Jobless Rate Falls to a 10-Year Low

Last Friday, the government said that the U.S. economy created 211,000 net new jobs in April. This was a big relief for investors because the report for March was a dud: just 98,000 net new jobs.

This highlights an important lesson for investors—don’t be carried away by an outlier. Most economic data contains at least some “noise.” Traders love to pick up on one-point trends and get carried away. Instead, we want to focus on the larger trends, and the economy continues to create new jobs.

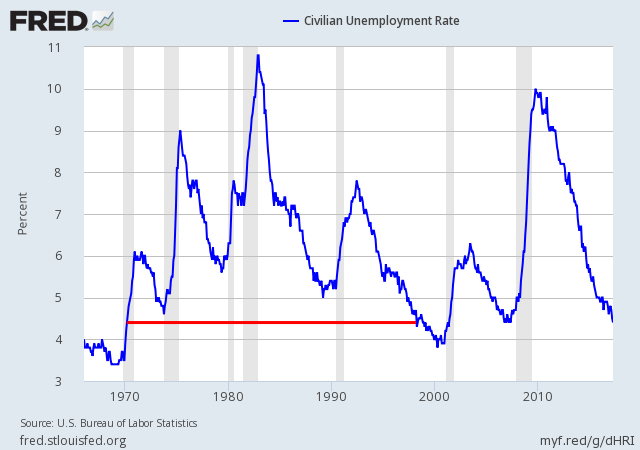

For April, the unemployment rate fell to 4.4%, which is a 10-year low. We actually came very close to making a 16-year low, but the figure for March 2007 stood in our way. Splitting out the decimals, unemployment rate is currently at 4.404%, while it was at 4.398% for March 2007. That was the low for the last cycle. The unemployment rate is lower now than it was at any point from March 1970 to March 1998.

For me, the larger issue is wages, and that’s still pretty blah. Last month, average hourly earnings rose seven cents to $26.19. The year-over-year change has decelerated, meaning the rate of growth has fallen, for the last two months.

There’s a lot of talk about the declining workforce participation rate, but that’s largely driven by demographics. More folks are retiring, and that shrinks the available workforce. Looking past the participation rate, the jobs-to-population ratio is currently the highest since January 2009. The broader “U-6” employment rate is down to 8.6%. That’s the lowest since November 2007. So there is some real improvement.

While this report was a relief, I still believe that it doesn’t warrant another Fed rate increase next month. I’m afraid my view is in the minority. According to the futures market, traders currently put the odds of a rate hike in June at 81%. What about after that? The odds currently stand at 56.5% for still another hike to come in December.

As I explained last week, the mild economic news during the first quarter should put any Fed plans on hold. I’m especially concerned about the weak wage figures. This past earnings season finally saw some revenue growth. I hope to see more, and that can be best achieved by putting more money in consumers’ pockets.

This was a pretty good earnings season for Corporate America. According to Zacks, 72.4% of reports beat expectations. Profits are up 14% from a year ago, while revenue is up by 7.9%. All 20 of our Buy List stocks beat expectations. I believe that’s a Crossing Wall Street first. Now let’s look at our last two earnings reports from this cycle.

Earnings from Cognizant Technology Solutions and Moody’s

The last two earnings reports for this season came on Friday, just after I sent out last week’s newsletter.

For Q1, Moody’s (MCO) earned $1.47 per share, which was well ahead of the Street’s consensus of $1.24 per share. For Q1, Moody’s had revenues of $975.2 million. That’s up 19% from a year ago. Adjusted operating margin was 48.8%.

Previously, the ratings-agency firm said they expect full-year earnings between $5.15 and $5.30 per share. Now they say they expect earnings at the “upper end” of that range.

Shares of MCO initially sold off some since the report, but don’t worry. The company is doing very well. Moody’s remains a buy up to $119 per share.

For Q1, Cognizant Technology Solutions (CTSH) netted 84 cents per share. Revenues rose 10.7% to $3.55 billion. Their operating margin was 18.9%. Earlier, the IT outsourcer told us to expect earnings of 83 cents per share, and that’s what Wall Street had been expecting as well.

“We delivered solid results in the first quarter and continued to build our digital solutions portfolio, expand our skills and enhance our engagements with clients,” said Francisco D’Souza, Chief Executive Officer. “We’re making good progress in accelerating Cognizant’s shift to digital services and solutions to create value for clients and shareholders, positioning us well to achieve both our revenue and margin targets for this year.”

Now let’s turn to guidance. For Q2, Cognizant sees revenue ranging between $3.63 billion and $3.68 billion, and EPS of at least 89 cents per share. That’s quite good. For the full year, CTSH sees revenue between $14.56 billion and $14.84 billion, and EPS of at least $3.64. Wall Street had been expecting 90 cents per share for Q2, and $3.64 per share for all of 2017.

Cognizant will also pay out its first-ever dividend. If you recall, this was part of the agreement they reached with Elliott Management. CTSH will pay a 15-cent dividend at the end of this month.

Shares of CTSH rose 4.1% on Friday, plus another 1.7% on Monday. This week, I’m raising my Buy Below on Cognizant Technology Solutions to $66 per share.

Preview of Earnings from Ross Stores

Next Thursday, Ross Stores (ROST) will report its fiscal first-quarter earnings. This is for the earnings period that ended in April. The retail sector has been getting creamed lately, but Ross is one of the few that have been holding up relatively well. As I’ve long believed, Ross is a rare retailer that’s Amazon-resistant.

In late February, they reported very good earnings. For their fiscal Q4, Ross earned 77 cents per share, two cents more than estimates. Comparable-store sales growth was 4%, which is quite good.

For all of 2016, Ross made $2.83 per share. That’s up 13% over last year. Ross also increased its quarterly dividend from 13.5 to 16 cents per share. That’s an increase of 18.5%. Over the last seven years, Ross has raised its dividend by 300%.

For Q1, Ross forecasts earnings of 76 to 79 cents per share and comp-store sales growth of 1% to 2%. This strikes me as conservative.

The CEO said, “There continues to be uncertainty in the political, macro-economic, and retail climates, and we also face our own challenging sales and earnings comparisons. Thus, while we hope to do better, we believe it is prudent to remain somewhat cautious in planning our business for the 2017 fiscal year.”

Ross projects full-year 2017 earnings between $3.02 and $3.15 per share. That’s up 7% to 11% over 2016. However, the current fiscal year is 53 weeks long. The company estimates that the extra week adds eight cents per share. Ross sees same-store growth this year of 1% to 2%.

Buy List Updates

Wabtec (WAB) recently reported good Q1 earnings, although the shares have drifted a bit lower. This week, the freight-services company rewarded shareholders by announcing a 20% dividend increase. WAB’s quarterly payout rises from 10 to 12 cents per share. This is the seventh year in a row that WAB has raised its dividend. Based on Thursday’s close, WAB now yields 0.60%. Wabtec’s stock crumbled during the second half of 2015. It’s gradually climbed back.

In last week’s CWS Market Review, I mentioned the good earnings report from Continental Building Products (CBPX). The wallboard maker beat estimates by five cents per share. In Friday’s trading, the stock jumped higher by 9.6%. I’m happy to see this stock finally get some positive attention from the market. Going into the earnings report, CBPX had not been performing so well. The stock remains a buy up to $26 per share.

That’s all for now. Next week should be another fairly quiet one for economic news. On Tuesday, the Federal Reserve will release the Industrial Production report for April. The data here have improved a bit lately, but not much. The report for March was helped by a weather-driven increase from utilities. I’d like to see more improvement. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on May 12th, 2017 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His