CWS Market Review – February 2, 2018

“It takes character to sit with all that cash and to do nothing. I didn’t get to where I am by going after mediocre opportunities.” – Charlie Munger

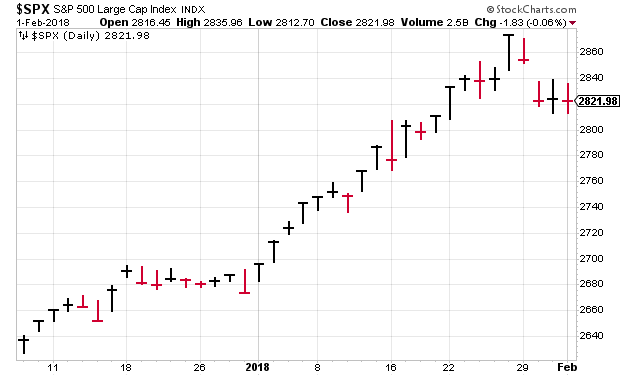

This was the best January for the stock market in 20 years. However, the end of the month was a little jarring. Monday was the worst day for stocks in four months, and Tuesday was even worse than that. That snapped a streak of 49 straight days in which the S&P 500 closed within 1% of its all-time high.

What’s happening is that bond yields are finally becoming effective competition for stocks. The 10-year yield topped 2.7% for the first time since 2014. The yield has nearly doubled in the last 18 months. It’s mostly been high-yielding stocks that have been lagging the market in recent weeks.

We’re right in the thick of earnings season. We had five Buy List stocks report this week, and we have nine more next week. In this issue, I’ll run down all of our earnings reports. We also got a nice dividend boost from AFLAC.

This issue will be all about earnings, but I wanted to mention this week’s Fed meeting. As expected, the central bank decided to leave rates alone. However, it seems fairly likely that they’ll raise rates in March, and again in June. This could dominate Wall Street this spring. For now, let’s jump into our long line of earnings reports.

Danaher and Stryker Beat the Street

Let’s start at the top with Dananher (DHR). On Tuesday, the company reported another good quarter. For Q4, DHR raked in $1.19 per share. They had previously given us a guidance range of $1.12 to $1.16. What Danaher calls “non-GAAP core revenue” rose by 5.5%.

This is a very solid company. For the whole year, Danaher made $4.03 per share. That’s up 11.5% over 2016. Non-GAAP core revenues grew by 3.5%. Danaher had operating cash flow of $3.5 billion.

Thomas P. Joyce, Jr., President and Chief Executive Officer, stated, “We are very pleased with our strong fourth quarter results. The team delivered 5.5% core revenue growth, solid margin expansion, and double-digit adjusted earnings per share growth. As we reflect back, 2017 was a year of accelerating revenue growth, solid margin improvement, continued growth investment, and great performance at our more recently acquired larger businesses. In addition, mid-teens growth in free cash flow helps position us for more significant capital deployment in 2018.”

Joyce continued, “As we look ahead, we believe that the strength of our portfolio, combined with the power of the Danaher Business System, provide us with the foundation for long-term shareholder value creation.”

For Q1, Danaher sees earnings ranging between 90 and 93 cents per share. For all of 2018, they’re projecting $4.25 to $4.35 per share. That’s a tad weak, but it’s nothing to worry about. Wall Street had been expecting 93 cents and $4.35 per share. The shares pulled back a little bit, but I’m not concerned. In fact, this week, I’m raising my Buy Below on Danaher to $105 per share.

Also on Tuesday, Stryker (SYK) reported Q4 earnings of $1.96 per share. That was one penny more than expectations. For the year, Stryker earned $6.49 per share.

Consolidated net sales of $3.5 billion and $12.4 billion increased 10.0% and 9.9% as reported in the quarter and full year and 8.7% and 9.8% in constant currency, as foreign currency exchange rates positively impacted net sales by 1.2% and 0.1%. Excluding the 0.7% and 2.7% impact of acquisitions, net sales increased 8.1% and 7.1% in constant currency, including 9.1% and 8.2% from increased unit volumes partially offset by 1.0% and 1.1% in lower prices.

Breaking down their business units, net sales for Orthopaedics rose by 8.1%, MedSurg was up 10.9%, and Neurotechnology and Spine was up 11.5%.

For 2018, Stryker sees organic sales growth of 6.0% to 6.5%. They see Q1 earnings ranging between $1.57 and $1.62 per share. For the full year, Stryker expects earnings of $7.07 to $7.17 per share. Those are good numbers. I’m lifting my Buy Below on Stryker to $170 per share.

Earnings from AFLAC and Check Point Software

On Wednesday, we had two more Buy List reports. AFLAC (AFL) reported Q4 operating earnings of $1.60 per share. Remember that the duck stock does most of its business in Japan, and the weak yen knocked off three cents per share. Adjusting for that, AFLAC took in $1.63 per share last quarter. That’s an increase of 13.2% over Q4 2016.

For all of 2017, AFL’s revenues fell 4.0% to $21.7 billion. Operating earnings came in at $6.81 per share compared with $6.50 per share in 2016. The weak yen cost AFLAC 10 cents per share. Adjusting for that, operating earnings rose 6.3% last year.

AFLAC also raised its quarterly dividend from 45 to 52 cents per share. That’s an increase of 15.6%. The dividend is payable on March 1 to shareholders of record at the close of business on February 21.

I’m really impressed with AFLAC’s performance. For 2018, AFLAC is looking for earnings to range between $7.45 to $7.75 per share. That assumes a yen/dollar rate of 112.16 which was the average for 2017. I’m keeping my Buy Below at $93.

Also on Wednesday, Check Point Software (CHKP) reported Q4 results of $1.58 per share which topped estimates by eight cents per share. Previously, the company projected earnings between $1.45 and $1.55 per share, so they’re beating their own estimates. For context, Check Point made $1.46 per share in Q4 of 2016, so that’s decent growth.

Quarterly revenue rose 4% to $506 million while security subscriptions were up 18%. For the year, CHKP made $5.33 per share which was an increase of 13% over 2016. During Q4, the company bought back around 2.4 million shares for a cost of $250 million.

Now let’s look at their guidance. For Q1, Check Point sees revenues between $1.25 and $1.30 per share on revenues of $440 to $460 million. The Street had been expecting $1.32 per share on $462 million in revenue. For the full year, they see EPS of $5.50 to $5.90 on revenue of $1.9 to $2 billion. Wall Street had been expecting $5.72 on $1.97 billion. Overall, Check Point had a good quarter, and it was a nice rebound off the poor results from Q3. CHKP remains a buy up to $111.

Ingredion Missed by Two Cents

Our fifth earnings report this week was on Thursday morning from Ingredion (INGR). The plant food company posted Q4 earnings of $1.73 per share which was two cents below estimates. For the year, INGR made $7.70 per share. That’s up from $7.13 in 2016.

“We concluded 2017 with record earnings per share and operating income. Sales of our higher-value specialty portfolio grew to 28 percent of net sales for the year and the continued integration of our acquisitions of the Sun Flour rice business, TIC Gums and Shandong Huanong Specialty Corn position us for continued growth,” said Jim Zallie, president and chief executive officer. “For the year, specialty-related volume growth, as well as our global optimization efforts drove margin expansion. North America, Asia Pacific and EMEA achieved record operating income. South America, although down, completed an important organizational restructuring, enabling a more cost competitive position going forward.

Despite the miss, this was an OK quarter for Ingredion. Last year wasn’t particularly strong for them, but things seem to be improving. For 2018, they see EPS ranging between $8.10 and $8.50. The shares lost 4.3% on Thursday which brings INGR back to where it was two weeks ago. I’m keeping our Buy Below at $146.

Next Week’s Earnings Parade — Nine Buy List Stocks Report

Next week will be a busy one for us. We have nine earnings reports on tap. Let’s run down the list.

On Monday, one of our new stocks, Church & Dwight (CHD), will report. A lot of consumer staples stocks have been lagging lately. That usually happens when the economy ramps up. Last quarter, C&D beat by two cents per share. The board also authorized a $400 million share buyback program. For Q4, they see earnings of 50 cents per share. I’ll be curious to hear any guidance for 2018. I’m expecting something around $2.10 to $2.20 per share.

On Tuesday, we’ll have Becton, Dickinson and Cerner. Cerner (CERN) is normally a great stock, but they missed by a penny per share last time. What happened? Cerner blamed it on several large contracts that were expected to be signed in Q3 but were pushed to Q4.

For Q4, Cerner expects revenue between $1.3 billion and $1.35 billion and EPS between 60 and 62 cents. They also provided some preliminary numbers for 2018. Cerner sees 2018 sales between $5.5 and $5.7 billion. For EPS, Cerner sees $2.52 to $2.68.

Becton, Dickinson (BDX) is another new stock for us this year, and it’s already our second-biggest YTD with a gain of nearly 13%. In November, BDX reported fiscal Q4 earnings of $2.40 per share, two cents above expectations. For the year, BDX made $9.48 per share. For the current fiscal year, which ends next September, BDX expects earnings between $10.55 and $10.65 per share.

Wednesday will be peak earnings day for us with four reports due out. Three months ago, Cognizant Technology Solutions (CTSH) raised its full-year guidance to at least $3.70 per share. That implies Q4 earnings of 95 cents per share. On the revenue side, Cognizant expects revenues between $3.79 billion and $3.85 billion.

Fiserv (FISV) also missed earnings last season, their second miss in a row. The company narrowed its full-year guidance from $5.03 to $5.17 per share to $5.05 to $5.12. That means Q4 earnings should range between $1.34 and $1.41. Fiserv is already up 6.8% for us this year.

In November, Intercontinental Exchange (ICE) reported earnings of 73 cents per share. That beat the Street by three cents per share. ICE also approved a $1.2 billion share-buyback program. Things are looking good for ICE. The NYSE just said it had a record-breaking month for January. The consensus on Wall Street is for Q4 earnings of 72 cents per share.

Torchmark (TMK) is another one of our new additions this year. If I had to guess which S&P 500 stock had the most stable earnings line, I would probably go with Torchmark. They see Q4 earnings of $1.19 to $1.25 per share. For 2018, TMK is expecting $5.00 to $5.25 per share.

Shares of Snap-on (SNA) have pulled back lately. Barron’s ran a critical article last weekend. I’ve been concerned by weakness in their tool division. Snap-on will report earnings on Thursday. The consensus on Wall Street is for Q4 earnings of $2.66 per share.

The Moody’s (MCO) earnings are due out on Friday. Last time, the ratings agency handily beat expectations. At the time, the company increased its full-year range to $5.85 to $6 per share. This was the second time they raised full-year guidance. The higher guidance implies Q4 earnings of $1.28 to $1.43 per share. Look for an earnings beat.

That’s all for now. Lots more earnings to come next week. We also have the January jobs report coming out later tomorrow. The consensus is for 175,000 new jobs. On Monday, the ISM Non-Manufacturing Index comes out. Then on Wednesday, the Consumer Credit report comes out. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Syndication Partners

I’ve recently teamed up with the folks at Investors Alley to feature some of their content. I think they have really good stuff. Check it out!

3 Companies Working to Destroy the Blockchain with Quantum Computing

It pays sometimes to listen to what comes out of the annual meeting of the world’s elite at Davos, Switzerland. This year was a prime example.

Satya Nadella, the CEO of Microsoft (Nasdaq: MSFT), gave the stark warning that the world is rapidly “running out of computing capacity”. He added that Moore’s Law – the maxim that the power of computer chips doubles every two years – is “rapidly running out of steam.”

Nadella said the problems the world faces today need superfast quantum computers to solve them. As the head of the company’s quantum computing team, Todd Holmdahl, said to the Financial Times, “We have an opportunity to solve a set of problems that couldn’t be solved before. On a classical computer, they would take the life of the universe to solve.”

This is breakthrough technology that will change our world, making quantum computing (a subject I’ve touched on previously) a topic worth revisiting.

A Big Bank Trade Moving Into Earnings

As an options trader, earnings season is often one of the most enjoyable times to trade. During the heavy earnings periods, you often see plenty of large moves in individual stocks (for obvious reasons). Options can be a good way to capitalize off those big moves.

However, the biggest challenge with using options for earnings is that big moves tend to be built into the options prices. To make money buying options on earnings plays, you need a big earnings surprise and for traders/investors to act in a timely manner on that surprise. At times, it doesn’t work out as well as hoped.

Conversely, sometimes the best time to use options to bet on a big move is when it’s least expected. That’s when you can frequently get a good deal on options prices. I personally like to find cheap straddles on stocks which I think could move (but aren’t necessarily near an earnings period). A straddle is when you buy a call and a put at the same strike during the same expiration period. They are typically bought at-the-money or very near the current stock price of the underlying.

Posted by Eddy Elfenbein on February 2nd, 2018 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His