CWS Market Review – November 30, 2018

“Interest rates are still low by historical standards, and they remain just below the broad range of estimates of the level that would be neutral for the economy.” – Federal Reserve Top Banana Jerome Powell

See those two words “just below” in bold in the quote above? Those two little words rocked the entire market this week. Thanks to “The Two Little Words” (T2LW) on Wednesday, the S&P 500 had its best day in eight months.

How could that be? In this week’s issue, I’ll explain what it all means. I’ll also take a look at three of our recent Buy List earnings reports. Wall Street was less than pleased, but I’ll break it down for you. We also got a nice dividend hike from Hormel. The Spam people have now raised their dividend for 53 years in a row. Also, ADS is planning to sell off its marketing business.

But first, let’s look at what Jay Powell had to say and why it sparked a big rally on Wall Street.

What ”Just Below” Means

Let’s turn back the clock to October 3. That’s when Mr. Powell said in an interview, “We may go past neutral, but we’re a long way from neutral at this point, probably.” That’s Fedspeak for “I will absolutely wreck this economy if I have to in order to kill inflation.” Not surprisingly, that comment really spooked Wall Street. Traders took it to mean that the Fed was going to continue raising interest rates even though the yield curve was getting close to flat. The Fed might even raise rates a lot.

By neutral rate, they mean there’s some magic interest rate out there, and if we’re below it, the economy is being helped, but if we’re above it, the economy is being constrained. The problem is, no one knows where the neutral rate is, so we have to guess. Even though we don’t know where the neutral is, we can occasionally get a faint hint as to its whereabouts. (If you want to be among the cool kids, the neutral rate is called “R-Star”.)

People were unnerved by Powell’s remark and by October 10, the market finally cracked. The S&P 500 lost 5.3% in two days, and the pain lasted during much of the month of October. Looking inside the market, we can see that much of the damage from Red October was focused on housing stocks and construction in general. This makes sense because higher rates from the Fed means higher mortgage costs, and that means few home sales. We also saw some soggy housing reports recently. In other words, footprints of R-Star.

On our Buy List, stocks like Sherwin-Williams (SHW) got absolutely clobbered in October even though there was little stock-specific news. When the earnings report finally came, it was a bit below expectations, but nothing terrible. Interestingly, the shares have been recovering quite nicely since the earnings report. I suppose true expectations were for disaster, and that didn’t come.

What was Powell thinking in being so aggressive? Sure, the jobs market was looking better, but there haven’t been signs of inflation. In fact, commodity prices have been dropping. Oil is down, and the dollar has been strong.

In September, the Fed’s “dot plot” was forecasting three more rate hikes for next year on top of one more increase next month. As recently as three weeks ago, the futures market pegged a 23% chance of three more rate increases next year.

But the stock slide has changed perceptions. President Trump has also criticized the Fed. The president told the Washington Post, “So far, I’m not even a little bit happy with my selection of Jay. Not even a little bit. And I’m not blaming anybody, but I’m just telling you I think that the Fed is way off-base with what they’re doing.”

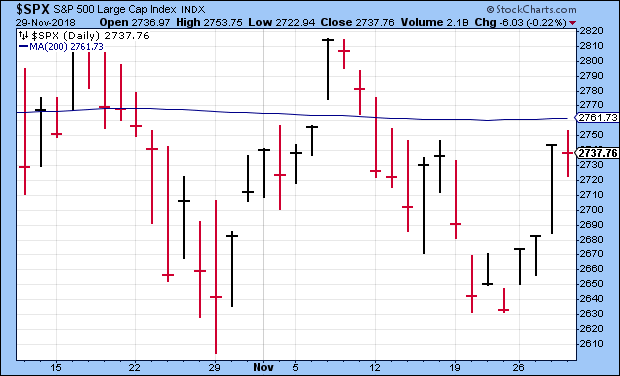

The president isn’t alone in his thinking, and that brings us to Powell’s comments from Wednesday. The Fed Chairman seems to have changed his tune by saying that we’re “just below” neutral. In other words, many more rate hikes are not coming. In fact, by looking at the stock chart, you can tell the exact moment at which Powell started speaking.

Let’s look at a possible game plan for the Fed. I think it’s very likely that they’ll hike next month, but after that, they may take a pause. In fact, I think it’s very reasonable that the Fed will hike rates just once in 2019.

A pause from the Fed is very good for stocks, and that’s what we saw. Let’s also remember that stocks had not been doing well. The S&P 500 “tested” its closing low from late October. In fact, last Friday, the index closed at 2,632.56, which is the lowest close since early May. On top of that, the stock market’s P/E Ratio has been falling for much of this year.

There’s one more hurdle left, and that’s the 200-day moving average. The S&P 500 is now less than 1% from its 200-DMA. If we can convincingly break above that, then I think we’ll see many more months of gains. Now let’s look at some of our recent Buy List earnings reports.

Earnings from Ross Stores, Hormel Foods and Smucker

Over the Thanksgiving break, we had three Buy List earnings reports. These are our three Buy List stocks that have quarters ending in October.

Ross Stores (ROST) has been in a major funk lately, which is odd because I still like the deep-discounter a lot. The stock recently fell for ten days in a row for a total loss of 22%. That’s basically the same as the entire stock market’s one-day crash in 1987.

Despite that, on Tuesday, November 20, Ross Stores reported fiscal Q3 earnings of 91 cents per share. Sales rose 7% to $3.5 billion. The important metric for us, same-store sales, rose by 3%. Going into this quarter, Ross told us to expect earnings between 84 and 88 cents per share and same-store sales growth of 1% to 2%. Wall Street had been expecting 90 cents per share.

Barbara Rentler, Chief Executive Officer, commented, “Both sales and earnings for the quarter were ahead of our forecast, despite being up against very strong multi-year comparisons. Though above plan, operating margin of 12.4% was down from last year as higher merchandise margin was more than offset by increases in freight costs and this year’s wage investments.”

Ms. Rentler continued, “During the third quarter and first nine months of fiscal 2018, we repurchased 2.9 million and 9.4 million shares of common stock, respectively, for an aggregate price of $278 million in the quarter and $807 million year-to-date. We remain on track to buy back a total of $1.075 billion in common stock during fiscal 2018.”

For Q4, which is the all-important holiday quarter, Ross projects same-store sales growth of 1% to 2%. For EPS, they see that ranging between $1.09 and $1.14 per share. That’s the same as the previous guidance, but it now includes a gain of seven cents per share due to the resolution of a tax matter.

For the entire year, Ross sees earnings of $4.15 to $4.20 per share. In the earnings report, Ms. Rentler sounded cautious: “As we enter this year’s holiday season, not only are we up against our toughest sales comparisons from 2017, but we are also expecting another fiercely competitive retail environment.”

This is basically what I expected. Their Q3 guidance was low, but that’s what they often do. The outlook for Q4 is the same as before. That didn’t stop the stock from getting hammered. ROST rebounded a little this week. I’m still a Ross fan, but I’m lowering our Buy Below to $92 per share.

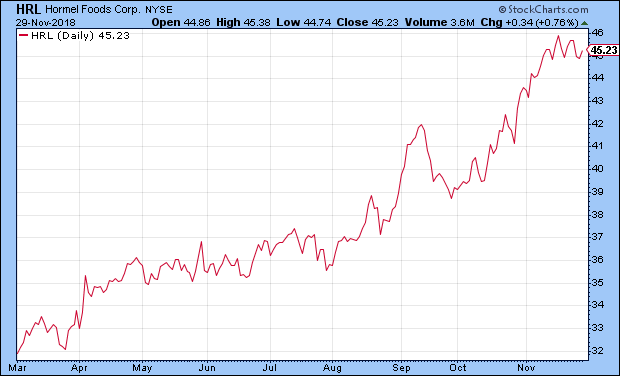

Also on November 20, Hormel Foods (HRL) reported fiscal Q4 earnings of 51 cents per share. That was two cents above estimates. Unfortunately, their revenues were pretty weak. Organic sales fell 1%, and operating margin slipped to 12.6%. For the year, the Spam folks made $1.57 per share.

For 2019, Hormel sees revenue ranging between $9.7 and $10.2 billion and EPS between $1.77 and $1.91. That’s not bad. The shares initially got dinged after the report but have since recovered. The stock is now about where it was prior to the earnings report.

Hormel also raised its dividend from 18.75 cents to 21 cents per share. (I had predicted 20 cents per share.) That’s their 53rd consecutive dividend increase. It’s also their tenth-straight year of double-digit increases. Not bad. I’m raising my Buy Below on Hormel Foods to $49 per share.

On Wednesday, JM Smucker (SJM) reported fiscal Q2 earnings of $2.17 per share. That missed Wall Street’s consensus by 17 cents per share. Net sales rose 5% to $2 billion which was $100 million below consensus. Traders were not pleased. The stock got slammed for a 7% loss on Wednesday.

Smucker is in a bit of a jam. One problem is the pet-foods business. Overall, growth has been good for pet foods, but it still hasn’t matched expectations. The business has also been hurt by higher transportation costs. Also, Smucker’s overall business has been plagued by a weak pricing environment. The company said it expects better performance next year.

Smucker also lowered its full-year guidance. The company now expects net sales of $7.9 billion and earnings between $8.00 and $8.20 per share. The previous forecast was for $8.0 billion and earnings between $8.40 and $8.65 per share. I’m keeping our Buy Below at $114 per share.

Buy List Updates

There are two Buy List stocks with quarters ending in November, RPM International (RPM) and FactSet (FDS). RPM probably won’t report until the first week of 2019. FDS said they’ll report their fiscal Q1 results on Tuesday, December 18. That will be our final Buy List earnings report for the calendar year.

On Tuesday, Alliance Data Systems (ADS) said it’s looking at selling its Epsilon marketing business. There’s no guarantee that ADS will sell, but the company is seriously exploring that option.

Last month, Acxiom sold its marketing business for $2.3 billion, which probably planted the idea in Alliance’s mind. Last year, Epsilon made up about 30% of Alliance’s total revenue. The company said it would use the proceeds to pay down debt, buy back shares and pay out dividends.

That’s all for now. Next week is December, and we’ll get some of the key monthly economic reports. On Monday, the ISM Manufacturing Index comes out. The last one was 57.7 which is little weaker than I had expected. On Wednesday is the ISM Non-Manufacturing Index. We’ll also get the ADP payrolls report, plus Fed Chairman Powell will be speaking. Thursday is jobless claims. Then Friday is the big November jobs report. Last month, the economy created 250,000 new jobs, and the unemployment rate stayed at 3.7%. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

P.S. On Monday, I’ll be on Bloomberg TV’s “The Close” between 3:50 pm and 4:10 pm.

Posted by Eddy Elfenbein on November 30th, 2018 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His