CWS Market Review – January 17, 2020

“The dangers of life are infinite, and among them is safety.” — Goethe

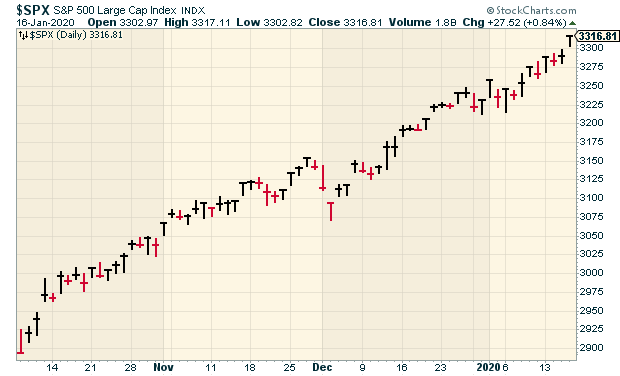

On Thursday, the S&P 500 closed above 3,300 for the first time ever. If you’re into numerology, the index first broke 330 in 1987, meaning 33 years ago, and it first broke 33 in 1954 which was 33 years before that. I don’t know what it means, but that’s a lot of threes.

In any event, not only is the market moving higher, but it’s been a fairly broad rally. That’s always a good sign. I tend to be suspicious when a market rally leans heavily on just a few stocks. This time, the minnows are joining in. Right now, the number of stocks in the S&P 500 that are above their 200-day moving average is at a five-year high.

The S&P 500 is divided into eleven sectors. Eight are currently at or near new 52-week highs. Two more aren’t that far away. Only Energy is lagging behind, and even that sector has perked up this year.

Here’s another cool stat: The stock market hasn’t had a down election year when an incumbent was running in 80 years.

This week, we got our first earnings report of this season. Eagle Bancorp missed by a penny per share. (Or more accurately, analysts missed reality.) Despite the miss, the bank’s doing just fine. I’ll have more in a bit. I also have a complete Buy List earnings calendar for you. But first, let’s look at some recent economic news.

The Lowest Jobless Rate in Half a Century

Last Friday, the government released the jobs report for December. The U.S. economy created 145,000 net new jobs which was below expectations of 160,000. The unemployment rate fell to its lowest level since June 1969.

The labor market is doing well. The government also tracks a broader measure of employment called the U-6 rate. For December, that rate fell to 6.7% which is the lowest rate since the data series was first tracked in 1994.

The weak spot, however, is wages. To be fair, we’re seeing some improvement here, but we need to see more. Over the past year, average hourly earnings are up by 2.9%. That’s more than inflation, but not by much. Bear in mind that higher wages will eventually translate into higher sales and profits for our companies.

We may be seeing evidence that workers are in demand. There was a recent story that Taco Bell is willing to pay general managers $100,000 per year. The company will also start paying employees 24 hours of sick time each year.

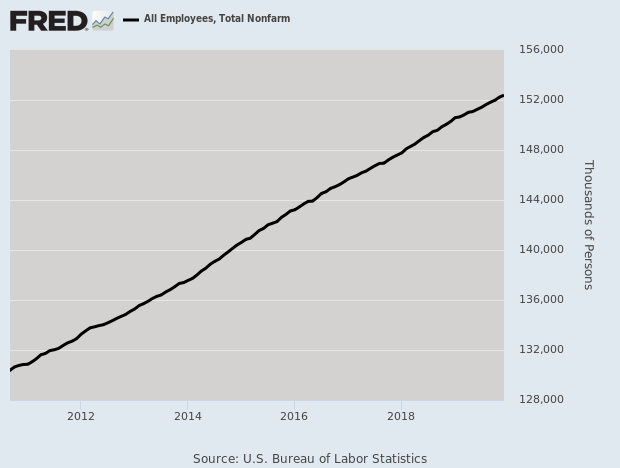

Here’s a look at nonfarm payrolls over the last decade. People who aren’t in finance would be astounded if they knew how much time and energy goes into forecasting this line.

Here’s a remarkable look at how the U.S. economy has changed. If we were to have the same jobs-to-population ratio that we had 20 years ago, we’d need 8.8 million more jobs. We could also achieve it if we had 13 million fewer people. What’s changed is that there are many more retirees.

Despite the lackluster wage gains, consumers were still out at the malls spending money. On Thursday, the Commerce Department said that December retail sales rose by 0.3%. Also, retail-sales growth for November was revised higher to +0.3%. This suggests that the U.S. economy ended 2019 at a moderate pace. In the last year, retail sales grew by 6.1%. That’s close to the fastest pace since 2012.

Remember that consumer spending accounts for two-thirds of the economy. Economists like to watch “core” retail sales, which excludes cars, gas, building materials and food. For December, the core rate was up +0.5%. That’s quite good, and it’s an improvement over the 0.1% increase we had for November.

In fact, the strong jobs market may continue. The recent jobless-claims report fell to 204,000. That’s very good.

Fortunately, there’s been no evidence yet of an uptick in inflation. On Tuesday, the government said that the Consumer Price Index rose by 0.2% last month. That comes after a 0.3% increase in November. For all of 2019, the CPI increased by 2.3%. That’s the highest annual rate in eight years, but it’s still not that high. Importantly, inflation is still close to the Federal Reserve’s target of 2%.

Digging into the numbers a bit, we see that the “core” rate of inflation increased by 0.1% last month. This is the regular inflation rate, except for food and energy prices, which can be very volatile. The core rate was up by 0.2% in November. For the year, the core rate increased by 2.3%.

Overall, these are good numbers, and it looks like the Federal Reserve won’t need to make a move, in either direction, in the immediate future. It’s especially impressive that inflation is so low considering that the unemployment rate is low as well.

The Fed meets again in two weeks. Don’t expect much. In my opinion, the best market proxy for what the Fed will do is the two-year Treasury yield. On Thursday, the two-year yield closed at 1.58%, and that’s right in line with the Fed’s current target of 1.50% to 1.75%.

With the Fed now in reserve, let’s look at our upcoming earnings reports.

Fourth-Quarter Earnings Calendar

Here’s a table of the 21 Buy List stocks that are reporting this earnings season (the other four don’t follow the March/June/September/December cycle). I’ve included each stock’s earnings date, Wall Street’s consensus and the actual results. Please note that not all the dates are out, and the earnings consensus may change.

| Company | Symbol | Date | Estimate | Result |

| Eagle Bancorp | EGBN | 15-Jan | $1.07 | $1.06 |

| Silgan Holdings | SLGN | 28-Jan | $0.38 | |

| Stryker | SYK | 28-Jan | $2.46 | |

| Danaher | DHR | 30-Jan | $1.24 | |

| Hershey | HSY | 30-Jan | $1.24 | |

| Sherwin-Williams | SHW | 30-Jan | $4.39 | |

| Church & Dwight | CHD | 31-Jan | $0.55 | |

| Check Point Software | CHKP | 3-Feb | $1.99 | |

| AFLAC | AFL | 4-Feb | $1.02 | |

| Disney | DIS | 4-Feb | $1.48 | |

| Fiserv | FISV | 4-Feb | $1.14 | |

| Cerner | CERN | 4-Feb | $0.74 | |

| Globe Life | GL | 5-Feb | $1.72 | |

| Intercontinental Exchange | ICE | 6-Feb | $0.96 | |

| Becton, Dickinson | BDX | 6-Feb | $2.64 | |

| Moody’s | MCO | 12-Feb | $1.94 | |

| ANSYS | ANSS | tba | $1.98 | |

| Broadridge Fin Solutions | BR | tba | $0.72 | |

| Middleby | MIDD | tba | $1.72 | |

| Stepan | SCL | tba | $0.88 | |

| Trex | TREX | tba | $0.51 | |

Eagle Bancorp Earned $1.06 per Share

Now let’s look at our first earnings report. After the close on Wednesday, Eagle Bancorp (EGBN) reported Q4 earnings of $1.06 per share. That’s one penny below estimates, and it’s down from $1.17 per share from one year ago.

For all of 2019, Eagle made $4.18 per share. That’s down from $4.44 per year in 2018. The big issue I’ve been watching is Eagle’s legal fees. For Q4, the bank’s legal, accounting and professional fees and expenses rose 68% to $4.1 million. That’s about 12 cents per share.

Here’s what Eagle had to say:

The Company expects to continue to incur elevated levels of legal and professional fees and expenses in 2020 as it continues to cooperate with these investigations. Other than these increased costs, we do not believe at this time that the resolution of these investigations will be materially adverse to the Company. As a result of these ongoing investigations, there have been no regulatory restrictions placed on the Company’s ability to fully engage in its banking business as presently conducted. We are, however, unable to predict the duration, scope or outcome of these investigations.

Looking past these expenses, the bank is doing fine. For Q4, Eagle had a return-on-equity of 11.78%. The bank’s efficiency ratio was 39.7% for the quarter and 40% for the entire year. The legal expenses aren’t pleasant, but it’s a manageable problem. The market clearly over-reacted. Over the summer, the shares plunged $14 per share on the news.

Eagle opened Thursday’s trading down more than 3%, but it quickly righted itself and closed lower by just 0.3%. This is a good bank that’s sailing through some rough seas. Eagle remains a buy up to $53 per share.

Buy List Updates

Danaher (DHR) won’t report earnings until January 30. However, the CEO made some relevant comments at a healthcare conference this week. CEO Thomas P. Joyce, Jr. said that for Q4, Danaher’s sales will come in above the company’s previously-announced expectations. He also said that earnings will be “at or above” the high end of their range.

Allow me to translate. When a CEO says, “at or above,” they mean “above.”

Speaking of Danaher, it, along with a few other of our stocks like Moody’s (MCO) and Fiserv (FISV), has crept above our Buy Below prices. So has Trex (TREX), one of our newbies. It’s already up 11% in 11 trading days. I’m going to hold off adjusting our Buy Below prices until I get a chance to see their earnings reports. As always, there’s never a need to chase after good stocks. You always want to be a disciplined investor.

That’s all for now. The stock market will be closed on Monday in honor of Dr. Martin Luther King, Jr.’s birthday. Dr. King would have been 91. Next week will be dominated by earnings news. There’s not much in the way of economic reports next week. On Wednesday, the new-homes sales report is out. Then on Thursday, the jobless-claims report comes out. The last report was for 204,000, which is a very low number. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on January 17th, 2020 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His