CWS Market Review – July 14, 2017

“You can get in way more trouble with a good idea than a bad idea,

because you forget that the good idea has limits.” – Ben Graham

After a long wait, Q2 earnings season is finally here. Next week, six of our Buy List stocks are due to report earnings. I expect most of them to top expectations, but I’m also curious to see if they’ll raise guidance for the rest of the year. Right about now, companies have a good idea of how the year is shaping up.

In this week’s CWS Market Review, I’ll preview all of the earnings reports. Also this week, Janet Yellen testified before Congress and struck a cautious note about interest rates. There’s a good chance we’ll only get one Fed rate hike over the next 12 months. Not that long ago, the Fed was looking for a few more hikes.

The market is also undergoing a pronounced rotation away from consumer staple stocks. This is having an impact on some of the stocks on our Buy List. I’ll explain what it all means. But first, let’s look at our upcoming earnings reports.

Six Buy List Earnings Reports Coming Next Week

Here’s a look at the Earnings Calendar for our Buy List stocks this earnings season. Over the next few weeks, 21 of our 25 stocks will report earnings. On the table below, I’ve listed each stock’s reporting date and Wall Street’s consensus estimate:

| Company | Ticker | Date | Estimate |

| Snap-On | SNA | 20-Jul | $2.55 |

| Microsoft | MSFT | 20-Jul | $0.71 |

| Alliance Data Systems | ADS | 20-Jul | $3.73 |

| Danaher | DHR | 20-Jul | $0.97 |

| Sherwin-Williams | SHW | 20-Jul | $4.56 |

| Moody’s | MCO | 21-Jul | $1.33 |

| RPM International | RPM | 24-Jul | $1.18 |

| Express Scripts | ESRX | 26-Jul | $1.71 |

| Stryker | SYK | 27-Jul | $1.51 |

| Cerner | CERN | 27-Jul | $0.61 |

| Aflac | AFL | 27-Jul | $1.64 |

| Fiserv | FISV | 1-Aug | $1.23 |

| Ingredion | INGR | 1-Aug | $1.84 |

| Intercontinental Exchange | ICE | 3-Aug | $0.75 |

| Cognizant Technology Sol | CTSH | 3-Aug | $0.91 |

| Signature Bank | SBNY | n/a | $2.22 |

| CR Bard | BCR | n/a | $2.64 |

| Wabtec | WAB | n/a | $0.93 |

| Axalta Coating Systems | AXTA | n/a | $0.39 |

| Cinemark | CNK | n/a | $0.48 |

| Continental Building Products | CBPX | n/a | $0.35 |

There are a few stocks where I don’t have the earnings date just yet. Some of these companies are less forthcoming than others. Be warned that the earnings calendar may not be exact, but I’ll track all of our earnings news at the blog.

Next Thursday, July 20, will be a particularly busy day for us. Five of our Buy List stocks are due to report.

Microsoft (MSFT) has had some outstanding earnings reports in recent quarters. Their “Intelligent Cloud” business has been especially strong. For the June quarter, which is the fourth quarter of Microsoft’s fiscal year, Wall Street expects earnings of 73 cents per share, which is only two cents above last year’s fiscal Q4.

The stock got caught up in the brief tech swoon from last month. Lately, however, MSFT has been on the rise. MSFT has rallied the last five days in a row and is near another all-time high.

Meanwhile, Snap-on (SNA) hasn’t been well lately, which is a bit of a surprise. The company had a good earnings report three months ago, and the stock gapped up. But that didn’t last long, and SNA gradually gave back all its gains and dropped to its lowest point since the election. Wall Street expected earnings from Snap-on of $2.55 per share.

Alliance Data Systems (ADS) has been a frustrating stock for us, but I’m glad that our patience is finally paying off. On Thursday, in fact, ADS got to a fresh 52-week high. If you recall, this stock absolutely cratered in early 2016, and it’s been gradually clawing its way back ever since.

ADS runs a great business. They’re the loyalty-rewards people. Three months ago, Oppenheimer initiated coverage on ADS with an “Underperform” rating. Nice timing. A few days later, they crushed earnings and the stock jumped $20 per share. They reiterated their full-year forecast for earnings of $18.50 per share. That means the stock is going for 14.3 times this year’s estimate. That’s a decent valuation. For Q2, Wall Street expects earnings of $3.53 per share.

Danaher (DHR) is about as steady as they come. They told us to expect Q2 earnings to range between 95 and 98 cents per share. Wall Street had been expecting 99 cents per share. However, Danaher stuck by its full-year forecast of $3.85 to $3.95 per share. This stock doesn’t get nearly the amount of attention it deserves.

Sherwin-Williams (SHW) has been a great stock for us this year; it’s up 32% so far in 2017. For Q2, Sherwin expects earnings to range between $4.40 and $4.60 per share (that doesn’t include an adjustment of 25 cents per share for acquisition costs). Wall Street had been expecting $4.43 per share. For the whole year, Sherwin expects $14.05 to $14.25 per share (40 cents for acquisition costs). Their previous range was $13.60 to $13.80 per share.

Then on Friday, July 21, Moody’s (MCO) is due to report. This is one of my favorite long-term stocks. Last quarter, they earned $1.47 per share, which was 23 cents more than estimates. Revenues were up nearly 20% from the year before. Moody’s adjusted operating margin is close to 50%.

Moody’s had said they expect full-year earnings between $5.15 and $5.30 per share. In May, they added that they expect it to be in the upper range of that forecast. Wall Street expects Q2 earnings of $1.33 per share. Moody’s is currently a 32% winner for us this year.

Please note that a few of these stocks are currently above my Buy Below prices. I’ll probably adjust them soon, but I want to see the earnings reports first just to be sure.

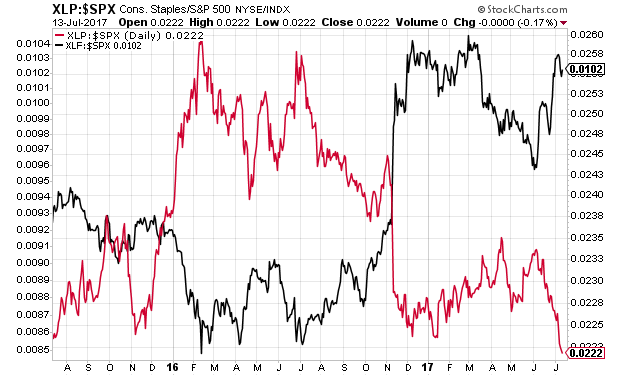

The Market Rotates Against Consumer Staples

Twice a year, the Chair of the Federal Reserve heads off to Capitol Hill to testify on monetary policy. This is usually done near the hottest and coldest days of the year in Washington. A few times, I’ve gone down to the hearing rooms to watch. In fact, once I got the seat directly behind Ben Bernanke.

On Wednesday, Janet Yellen gave what was interpreted as a more dovish stand on inflation and interest rates. Perhaps she was trying to underscore the point that the Fed aims for a gradual approach toward rate increases.

As a result, we saw a lot of financial stocks lag the market on Wednesday. That makes perfect sense, because banks want to see short-term rates go higher. Still, over the past five weeks, financial shares have performed quite well against the overall market. This period, of course, included the Fed’s last rate hike. I think that in general, Wall Street has been surprised by the firmness of the Fed’s stand on interest rates.

This is especially interesting because the rise in financials has been matched by a dive in consumer staple stocks. I should explain that consumer staples are classic defensive stocks. This means they’re the type of business that isn’t much hurt by a broad economic recess. Folks really don’t cut back on their toothpaste buying when the economy gets bad. Instead, they stop buying cars and houses.

The chart below shows Consumer Staples divided by the S&P 500 (in red) along with Financials divided by the S&P 500 (in black).

When staples lag, as they’re doing now, that’s usually a signal of economic expansion and the willingness of investors to shoulder more risk. The Consumer Staples ETF (XLP) has seemed to trail the market nearly every day since early June. Bear in mind that people like to buy these stocks because they are so conservative.

We’ve certainly seen this effect on our Buy List. Hormel Foods (HRL) and JM Smucker (SJM) have been lagging badly lately. As you might expect, I’m not concerned about either stock. In May, Hormel missed earnings by a penny. For some reason, that was an excuse to punish HRL. This week, the shares dropped to a 20-month low.

Smucker also dropped to a new low this week. Barron’s jumped to the stock’s defense earlier this week when they said, “it’s time to buy Smucker.” Here’s a sample:

Expect more uncertainty if Amazon.com’s (AMZN) $13.2 billion deal for Whole Foods goes through. All this helps explain why Smucker shares have fallen by more than 25% in the past year. But it doesn’t justify the severity of the selloff.

Is it time to nibble? We think so. In fact, we recommend a hearty bite.

Fetching a forward price-to-earnings multiple of less than 14.4 times earnings, Smucker trades at a 19% discount to its historical average. Moreover the stock, at $114.45, offers a market-beating 2.6% dividend yield.

Tuesday morning, Hilliard Lyons analyst Jeffrey Thomison upgraded Smucker from Neutral to Long-term Buy, arguing that the valuation had fallen to attractive levels. Over the next two years, he sees the stock rising almost 22% to $140 a share as earnings growth accelerates.

As investors it’s important to determine if a stock is falling because it’s not doing well or if it’s simply in an out-of-favor sector. With both Hormel and Smucker, the latter appears to be the case. With investing, there’s not much you can do when a good company gets brought down because it’s in an unpopular sector. Actually, that’s often a good time to look for bargains.

Another stock that’s been doing poorly for us is Ross Stores (ROST). The deep discounter has itself been deeply discounted. I think the retailer is going for a very good price here. This week, I’m lowering my Buy Below to $55 per share.

That’s all for now. Next week will be dominated by earnings reports. However, there will be some key economic reports. On Wednesday, the housing starts report comes out. Then on Thursday, we’ll get leading economic indicators plus the initial jobless claims report. Jobless claims peaked more than eight years ago, and we’re still close to multi-decade lows. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on July 14th, 2017 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His