CWS Market Review – March 8, 2019

“If you don’t have a competitive advantage, don’t compete.” – Jack Welch

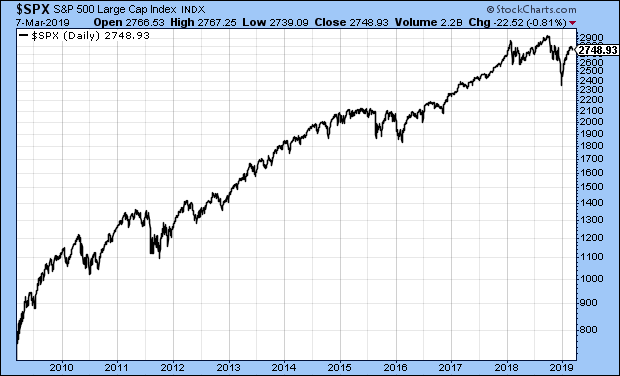

Tomorrow is the Bull Market’s 10th birthday. On March 9, 2009, the S&P 500 closed at 676.53. Since then, the market has more than quadrupled. Once we include dividends, it’s up fivefold. (Yep, those reinvested divies sure do add up!)

This has been one of the longest and strongest bull markets in history. Yet what I find interesting is how hated it’s been. Some folks just can’t stand this rally. All along the way, I’ve heard countless voices telling me that the upsurge was all phony and that we’re about to plunge into the abyss. Just you wait!

Some folks said it was a house of cards built by the Fed. Others said it was all a mirage because of share buybacks. In this week’s issue, I want to look back on the amazing bull run and see what important lessons are there. Later on, we’ll look at the growing gap between the stock and bond markets. On our Buy List, we had a nice earnings beat from Ross Stores. The deep-discounter gave us a 13% dividend boost as well. But first, let’s wish the mighty bull a happy 10th birthday.

Happy 10th Birthday to the Bull!

Let’s turn back the clock to March 6, 2009. That was a Friday, and like today, it was the day of the February jobs report. The report was a disaster. The U.S. economy lost a staggering 651,000 jobs in February 2009. The details were even worse. The number for January was revised to a loss of 655,000 jobs, and the loss for December was revised to 681,000. That was the single-worst month for jobs in 60 years.

There was bad news everywhere. The unemployment rate came in at 8.1%, which was a 25-year high. (Note that some of these numbers have since been revised over the last ten years, but these are the numbers that came out ten years ago.)

During the day on March 6, the S&P 500 fell to a devilish low of 666.79. The Dow got down to 6,469.95. Adjusted for inflation, that’s unchanged from the Dow’s peak 43 years before. Think about that. Forty-three years of no change.

I bring up these stats to point out a crucial lesson: this was the best time to invest in a generation. The news was terrible, and stocks were a great buy. Investors had to tune out the fear and focus on the long-term. But make no mistake – that’s not what the experts were saying.

I’ll give you an example. On March 6, the Wall Street Journal ran an editorial titled “Obama’s Radicalism is Killing the Dow.” Talk about lousy timing. The article wasn’t written by some nobody; it was by a former chairman of the President’s Council of Economic Advisors, Nouriel Roubini, who had earned the nickname “Dr. Doom.” Roubini said the market had even further to fall.

Let’s look at some indicators. The Volatility Index was at 50. Yikes! The TED Spread (remember that one) was at 1%. On Friday, the S&P 500 actually closed a tiny bit higher. The market sunk again on Monday, but crucially, it didn’t break below Friday’s low. On Monday, the S&P 500 closed at 676.53. That was a 12-year low. As of now, that stands as the lowest close this century.

Beneath the noise, there was a small news item that didn’t get too much attention at that time. Congress was considering backing off on the mark-to-market rules. I can’t say for certain, but that’s my strongest contender for what led the market to turn around. The lesson here is that many experts were flat wrong. For disciplined investors with a long-term focus, this was a great time.

Within a month, the S&P 500 soared 25%. The index gained 70% in less than a year. By the bull’s first birthday, Nobel Prize-winning economist Dr. Robert Shiller said the market was due for a pullback. Long-time readers will remember that 2009 was one of the best years for our Buy List. We beat the market by nearly 20%.

The Divergence Between Stocks and Bonds

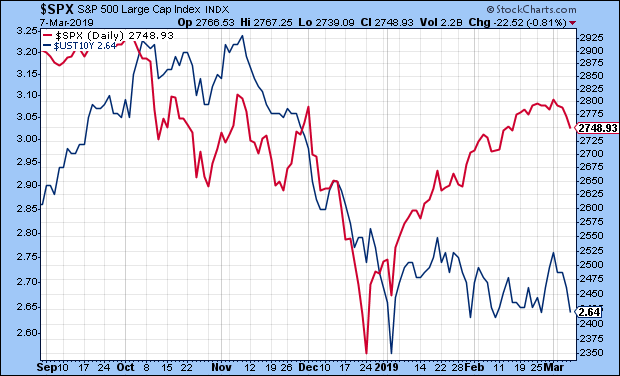

There’s been an interesting divergence lately between the stock and bond markets. Let me explain what I think is driving it. Late last year, the stock market tanked. The S&P 500 lost about 20% in three months.

While stock prices plunged, bond prices soared and bond yields fell. That’s perfectly natural as investors seek out safety. The yield on the 10-year bond fell from 3.24% on November 8 to a low of 2.56% on January 3. That’s a huge drop for less than two months.

Since then, the stock market has recovered a lot of lost ground (the red line below), but bond yields haven’t moved much at all (the blue line). On Thursday, the 10-year yield stood at 2.69%. That’s just five basis points higher than where it was at the end of 2018, yet the stock market is up more than 9.6% on the year.

So stocks go down, and bonds go up. Then stocks go up and bonds stay the same. What’s going on?

I think this phenomenon threads together a few important trends. One is obvious. The bond market is reflecting the Federal Reserve’s newly-found “patience.” If the Fed is going to chill out on interest rates, then it makes sense for long-term yields to be stable. The yield on the two-year Treasury, which can serve as a quick proxy for Fed policy, hasn’t moved much in several weeks.

The low long-term yields also suggest that the market is rallying on higher valuations. That’s always a fragile enterprise. I’ll take any rally we can get, but we’re getting one where the P/E Ratio is getting bigger. The “P” is rising while the “E” is pretty flat. There’s nothing wrong with a higher earnings multiple, but we should bear in mind that it can be fleeting.

This year may be a tough one for earnings growth. In fact, there’s a chance that earnings may contract a bit this year. We’ve already seen earnings estimates get slashed for Q1. Earnings valuations are decently (though not perfectly) correlated with long-term interest rates.

This also suggests that the market is more cautious about the economy. I would say that it’s unlikely that a recession will start this year, but it could be a year of more subdued growth. For example, the yield on the 10-year TIPs, the inflation-protected bond, recently got down to 0.72%. That’s an eight-month low.

Within the stock market, growth stocks have been outpacing value stocks. That may not last much longer. As a whole, our Buy List is holding up well this year. We’re ahead of the market, and we have 11 stocks that are more than double-digits. That includes our favorite retailer, which just reported earnings.

Ross Stores Earned $1.20 per Share

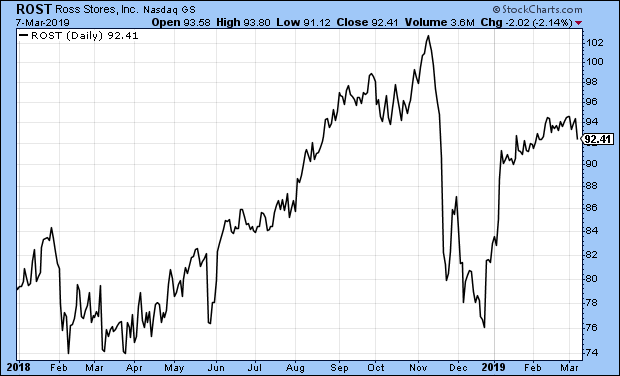

On Tuesday, Ross Stores (ROST) reported its fiscal Q4 earnings. The deep-discounter earned $1.20 per share. That’s for the big holiday shopping season. Previously, the company had given guidance of $1.09 to $1.14 per share. Sales for Q4 were $4.11 billion, which topped estimates of $4.05 billion. Comparable-stores sales were 4% whereas the Street was expecting 2.3%.

As usual, the company gave weak guidance. Ross sees Q1 earnings of $1.05 to $1.11 per share. The Street was expecting $1.18.

Looking ahead, Ms. Rentler said, “While we hope to do better, we continue to take a prudent approach to forecasting our business for 2019. Although we remain favorably positioned as an off-price retailer, we face our own difficult sales and earnings comparisons, a very competitive retail landscape, and an uncertain macro-economic and political environment.”

Well, they always say that. Ross sees full-years of $4.30 to $4.50 per share. Wall Street had been expecting $4.51 per share.

Ross is authorizing a $2.55 billion share buyback. If that’s not enough, Ross is raising its dividend. The quarterly payout will rise 13.3% from 22.5 cents to 25.5 cents per share. The new dividend is payable on March 29 to stockholders of record as of March 18.

The stock reacted in a few different ways following the earnings report. In the after-hours market, the shares were down, but the stock opened higher in the morning. It’s in times like that that I’m glad we’re not traders. In any event, Ross is doing very well. This week, I’m raising our Buy Below on Ross Stores to $95 per share.

Buy List Updates

With the earnings report from Ross Stores behind us, we’re now entering the lull period for Buy List earnings reports. FactSet (FDS) is due to report on March 26. RPM International (RPM) will probably report in early April. Outside those two, we don’t have anything until Q1 earnings season starts in mid-April.

One stock that made the news this week was Cognizant Technology Solutions (CTSH). On Thursday, the IT outsourcer announced a $600 million accelerated buyback. This is part of the already-announced plan to use 50% of their free cash flow to reward investors either by buybacks or dividends. Cognizant remains a good buy up to $74 per share.

That’s all for now. The big jobs report is later today. On Monday, we’ll get another retail-sales report. I expect a revision to the terrible numbers for December. On Tuesday, we’ll get the latest CPI report. I expect more subdued inflation. On Wednesday, we get durable goods and construction spending. New-home sales are on Thursday, and industrial production is on Friday. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on March 8th, 2019 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His