CWS Market Review – May 3, 2019

“Successful investing is anticipating the anticipations of others.” – J.M. Keynes

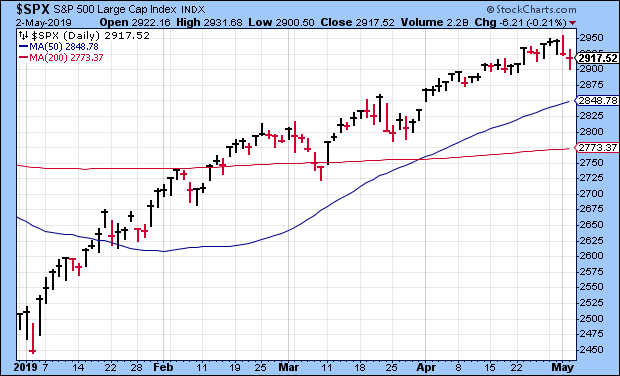

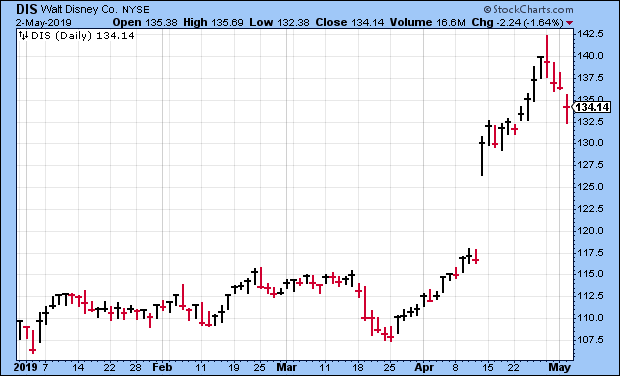

On Tuesday, the S&P 500 closed at yet another all-time high. The same day, our Buy List closed at a YTD high. We now have six stocks that are up more than 28% this year, including Disney, which just had its best month in nearly 20 years.

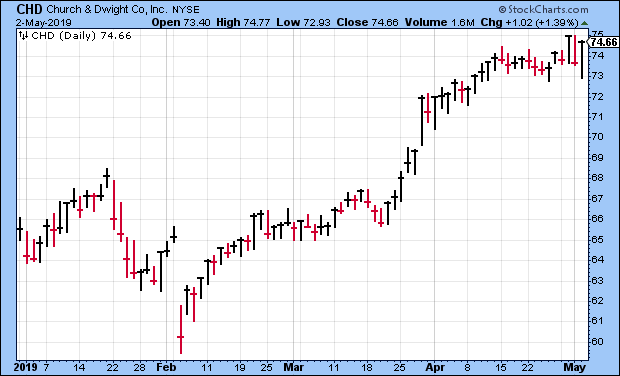

We had more Buy List earnings reports this week, and they were quite good. Fiserv beat by two cents. So did Intercontinental Exchange. Church & Dwight beat by four cents and rallied to a new high. Continental Building topped estimates by 24%.

Our one dud (and there’s always one each earnings season) was Cognizant Technology Solutions. The IT-outsourcer missed earnings and cut guidance, and the shares took a nasty fall. I’ll have all the details in a bit. But first, let’s survey some recent economic data.

We May Have Avoided an Earnings Recession

If all the earnings news wasn’t enough, the Federal Reserve got together this week and decided against changing interest rates. This wasn’t much of a surprise. In fact, the Fed may not be touching rates at all in the next few months. In the policy statement, the Fed kept the language saying the central bank will be “patient” regarding future rate increases.

In the post-meeting press conference, Chairman Jerome Powell was optimistic. He said, “Our outlook, and my outlook, is a positive one, is a healthy one, for the U.S. economy for the rest of this year.” I have to explain that in central-banker talk, that’s a jump for joy. Most central bankers are born dour, and it goes down from there.

I want to highlight some recent economic data because they back up Powell’s view. Last week, we got the initial report for Q1 GDP growth, and it came in at 3.2%. That’s pretty good. Over the last nine quarters, GDP has grown at its fastest pace in 12 years. We’ll get another CPI report next week, but the latest figures (through March) show that core inflation is running at 1.6%. That’s hardly a problem.

The April jobs report is due out later today. It may be out by the time you’re reading this. The other jobs numbers are encouraging. Jobless claims are up a bit, but that’s after hitting 50-year lows. Wednesday’s ADP payroll report showed a gain of 275,000 private payrolls last month. (I don’t place a high degree of faith in ADP’s figures, but it’s interesting to note.)

Earlier this week, we learned that the ISM Manufacturing report for April fell to 52.8. While that’s down, it still indicates that the factory sector is growing. Most importantly for us, this earnings season isn’t as bad as some folks had expected. About 75% of companies are beating expectations. We don’t have the full numbers in yet, but Credit Suisse had been expecting a Q1 earnings decline of 2.5%. Now they expect to see an earnings gain of 2.5% to 3%.

The takeaway is clear. All the doomsayers of a few months ago were overstating the case. The economy is still expanding, and markets are responding. Now let’s look at this week’s Buy List earnings.

Fiserv Earned 84 Cents per Share

After the bell on Tuesday, Fiserv (FISV) released a pretty good earnings report. This was a relief because the Q4 report wasn’t so hot. For Q1, the company made 84 cents per share. That’s an increase of 12% over last year. It also beat expectations by two cents per share. Quarterly revenues rose 5% to $1.43 billion. Free cash flow was $302 million, and adjusted operating margin came in at 31.9%. Those are nice numbers.

“We are off to a strong start to the year, with first-quarter internal revenue growth and sales ahead of our initial expectations,” said Jeffery Yabuki, President and Chief Executive Officer of Fiserv. “In addition to strong financial performance, we are well into integration planning and looking forward to completing the First Data acquisition in the second half of the year.”

In January, Fiserv said it’s going to merge with First Data in a major deal. The plans are moving ahead. The company sees the deal being completed in the second half of this year. On the earnings call, this is what Yabuki had to say about Q2.

Although we don’t provide quarterly guidance, it’s important to remind you that we had very high periodic revenue in last year’s Q2, which will create a difficult compare this year. As such, we anticipate the second quarter will be the low watermark for both internal revenue and adjusted EPS growth with strong acceleration into the back half of the year.

Due to the pending merger, Fiserv has suspended all stock buybacks. Fiserv reiterated its full-year earnings range of $3.39 to $3.52 per share. Fiserv is a buy up to $92 per share.

Four Buy List Earnings Reports on Thursday

We had four more Buy List earnings reports on Thursday, May 2. Let’s start with Church & Dwight (CHD), which reported before the opening bell. For Q1, CHD earned 70 cents per share, which was four cents better than Wall Street’s estimates, as well as CHD’s own guidance.

Q1 net sales rose 3.8% to $1.0447 billion. Organic sales rose by 4.5%. Global consumer products were up 5.2%. Of that, 2.7% was from volume while pricing added 2.5%.

First-quarter net sales grew 3.8% to $1,044.7 million. Organic sales grew 4.5% driven by global consumer-products growth of 5.2%, which was driven by volume growth of 2.7% and positive product mix and pricing of 2.5%. This was CHD’s fourth quarter in a row of organic sales growth topping 4%.

I was pleased to see gross margins increase by 20 basis points to 45.1%. Operating margins rose 120 basis points to 23.1%. The company reiterated its full-year EPS guidance of $2.43 to $2.47. That’s an increase of 7% to 9% over last year. For Q2, CHD expects earnings of 52 cents per share, which matches the Street. Church & Dwight remains a buy up to $75 per share.

Also on Thursday, Intercontinental Exchange (ICE) had a very good earnings report. (We love those pseudo monopolies!) For Q1, the NYSE owner made 92 cents per share. That was two cents more than Wall Street had been expecting. Their adjusted operating margin was 58%.

Q1 revenues were up 4% to $1.3 billion. The breakdown is that revenue for data and listings was $657 million. Revenue for trading and clearing was $613 million. Operating cash flow was $654 million. That’s up 14% from last year’s Q1. The company also noted that the blowup in bitcoin and other cryptos helped ICE acquire discounted assets in order to build its Bakkt platform.

Shares of ICE got off to a relatively slow start this year, but the stock has picked up over the past few weeks. The stock isn’t far from its all-time high, reached in December. Thanks to this week’s earnings report, I think there’s a good chance ICE can break out to a new high. I’m raising my Buy Below on ICE to $86 per share.

“Cognizant’s growth and performance in the quarter leaves room for improvement,” said Brian Humphries, Cognizant Technology’s CEO. Well, I’ll give him points for understated brevity. There’s no easy way to put it. Cognizant Technology Solutions (CTSH) had a terrible Q1.

Let’s look at the damage. For the first three months of this year, Cognizant made 91 cents per share. That was well below Wall Street’s forecast of $1.04 per share. The earnings report came out shortly before the closing bell, and the stock lost 7.7% in Thursday’s session.

Cognizant also cut its full-year forecast. Previously, the company expected EPS this year to be at least $4.40. Now they see it ranging between $3.87 and $3.95.

Where was the weakness? Apparently, the banking sector hasn’t been spending as much. The company’s Financial Services division, which makes up about one-third of its revenue, posted a sales decline of 1.7%. Karen McLoughlin, the company’s CFO, said, “Our revised full-year outlook reflects the first-quarter underperformance and expectations of slower growth in Financial Services and Healthcare for the remainder of 2019.”

I feel confident that Cognizant can manage its way through a difficult environment, but it will take some cost-cutting. For now, I’m dropping my Buy Below on Cognizant Technology Solutions to $70 per share.

After the bell on Thursday, Continental Building Products (CBPX) reported Q1 earnings of 42 cents per share. Expectations were for 34 cents per share. Net sales rose 4.5% to $122 million, and wallboard volume increased by 5.5% to 649 million square feet. We want to see that the company isn’t merely profiting from higher product prices but that they’re selling more units as well.

Continental’s profits were up 16.7% from a year ago. Operating income was up 11.3%. Earlier this year, the company had a malfunction at its Buchanan plant, which went offline for several weeks. That’s now been resolved.

These results are good news for a stock that hasn’t done well over the past few weeks. In fact, the last two earnings reports have been pretty good, but it hasn’t had much impact on the stock price. That may change soon. Buy up to $26 per share.

Three Buy List Earnings Reports Next Week

We have our final three Buy List earnings reports next week. You can see the complete Earnings Calendar. Three months ago, Broadridge Financial Services (BR) bombed its earnings report. For Q2, BR made 56 cents per share, which was 15 cents below estimates. Total revenues fell 6% to $953 million.

For its part, Broadridge didn’t alter its fiscal 2019 guidance. BR sees revenue growth of 3% to 5%, operating margins at 16.5% and EPS growth of 9% to 13%.

For Q3, the company sees revenue between $1.195 billion and $1.245 billion and earnings of $1.40 to $1.56 per share. Wall Street expects $1.50 per share.

At this point, Disney’s (DIS) earnings report seems anti-climatic. The stock just finished up its best month in nearly two decades. The Avengers movie blew up at the box office. For the opening weekend, the movie did $1.2 billion. On top of that, the Disney+ announcement was very well received. For Q1, Wall Street expects earnings of $1.59 per share.

Shares of Becton, Dickinson (BDX) have been uncharacteristically weak lately. The stock lost more than 10% over a four-day period in mid-April. The next earnings report is due out on Thursday, May 9. For 2019, Becton expects revenues to grow by 5% to 6%, and they see EPS ranging between $12.05 and $12.15. For Q1, Wall Street expects earnings of $2.58 per share.

Before I go, I wanted to make two Buy Below adjustments. I’m raising my Buy Below on FactSet (FDS) to $287 per share. The stock has been doing very well for us lately. We’re now +37.2% in FDS this year. Earnings are due out in June. I’m also raising Cerner’s (CERN) Buy Below to $71 per share. The stock just touched a new 52-week high.

That’s all for now. Heads up: I’ll be hitting the road, so next week’s issue will be out on Sunday, May 12. There’s not much in the way of economic reports. Earnings reports will start to taper off. On Thursday, I’ll be on the lookout for the jobless-claims report. Then on Friday, the April CPI report is due out. I expect to see more signs of subdued inflation. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on May 3rd, 2019 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His