-

Morning News: April 9, 2026

Posted by Eddy Elfenbein on April 9th, 2026 at 7:05 amIran War Cease-Fire Can’t Undo the Middle East’s Energy Hangover

Oil Prices Edge Higher as Confidence in Cease-Fire Wavers

Chevron Says Iran War Reduced Production, Impacted Earnings

Iran and Ukraine Make Oil Shocks Look Too Easy

Irish Protesters Block Dublin With Trucks and Tractors Over Rising Energy Costs

How ‘Attritable’ Systems Are Changing the Economics of Warfare

From Merchants of Death to Merchants of Confusion

Trump Got Schooled by Iran. He’ll Never Learn

How Iran’s Information War Machine Operates Online

Extent of Damage to Middle East Energy Facilities Key to Economic Impact, OECD Says

Dollar Could Rise if Cease-Fire Fails to Hold and U.S. Inflation Jumps

Markets Have Faced a Year of Chaos and Still Done Awfully Well

No Matter Your Opinion on Iran, War Is Depression

Why Reviving the WTO Would Serve US Interests

Why Fed Rate-Cut Prospects Have Dimmed, With or Without a Cease-Fire

The Fed Can Only Watch Iran’s Energy Shock — and Wait

Fed’s Inflation Woes Preceded the War With Iran

Wall Street Is Whiffing on Its Economic Forecasts

Earnings Optimism Enhances Stocks’ Allure as Iran Worries Ease

US Bank Profits to Rise on Deals, but Iran War Fuels Outlook Uncertainty

How to Rebuild Cuba’s Crumbling Economy

Ares Management to Buy Whitestone REIT in $1.7 Billion Deal

This Is Why America Is Short Four Million Homes

As Legislators Attack Single Family, Multi-Family Residences Shine

Why the U.S. Fertility Rate Has Hit a Record Low

RFK Jr. Has Stopped Talking About Vaccines. A Memo Shows Why

CoreWeave, Meta Strike Another $21 Billion Deal for AI Computing

Gen Z Is Using A.I., but Doesn’t Feel Great About It

Samsung to Invest $4 Billion in Chip Packaging Site in Vietnam

Delta’s Ace in the Hole for Surging Jet Fuel Costs: Its Own Refinery

Disney Planning Layoffs Under New CEO Josh D’Amaro

The Dealmaking Gamble Threatening Estée Lauder’s Turnaround

Can Longtime Car Executive Luca De Meo Kick the House of Gucci Into Gear?

Be sure to follow me on X.

-

Morning News: April 8, 2026

Posted by Eddy Elfenbein on April 8th, 2026 at 7:09 amArgentines Plunge Into Debt for Bills, Cars and Birthday Parties

JD Vance’s Hungary Trip Deserves Bipartisan Rebukes

As Trump Bullies NATO, Europeans Question Its Deferential Chief

Oil Prices Plunge and Stocks Surge After Cease-Fire Deal

Trump’s Ceasefire Still Leaves the US and Iran Mired in Quandary

Trump’s Iran War Leaves the US Looking Weakened to Adversaries

Our Vacations. Our Food. Our Mortgages. The Iran War Will Change Our Lives.

Delta Expects Strong Profit Despite Higher Fuel Costs

Investors Still Have Questions About the Cease-Fire

Why You Can’t ‘Flick a Switch’ to Get Oil and Gas Flowing Out of the Persian Gulf

Russia Boosts Oil Income to Highest Since Early in Ukraine War

Exxon Sees 6% of Its Worldwide Output Shut on Mideast Conflict

How China Built Its Vast Natural Gas Stockpile

The Iran War Is Hitting California Harder Than Any Other State

The US Economy Is Replaying the 2000s, Not the 1970s

Wall Street Watchdogs Pull Back Amid Trump’s Deregulatory Push

As It Becomes Wholesale, Banking Is More Essential Than Ever

White House Economists Say Stablecoin Rewards Won’t Harm Banks

My Quest to Solve Bitcoin’s Great Mystery

‘Definitely a Sham’: As Tariffs Climb, Trade Fraud and Accounting Tricks Proliferate

Blue Owl Fund Outlook Cut to Negative by Moody’s on Outflows

Growth-Focused States Move To Rein In Property Taxes

Altman Is His Own Risk Factor in OpenAI’s Mega-IPO

The SpaceX IPO Is Elon Musk’s Most Audacious Product Launch Yet

Tesla’s $44 Billion Swing Is More Than Just a Miss

US Charging Networks Race to Keep Up as Gas Prices Boost EVs

Ex-Rio Tinto Boss to List Seabed Mining Firm in $1 Billion Deal

Hormone Drugs Make $6.3 Billion Comeback After FDA Nixes Safety Warnings

Social Media Companies Are Looking for a New Name

How European Winemakers, Importers Absorbed Trump’s Tariff Punch

Why McCormick’s $65 Billion Deal Might Actually Work Out

The Economic Divide Behind That McDonald’s CEO Viral Video

The Sports Broadcasting Act Is Still a Home Run for Consumers

Be sure to follow me on X.

-

CWS Market Review – April 7, 2026

Posted by Eddy Elfenbein on April 7th, 2026 at 7:39 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

On Tuesday, the stock market rose for its fifth day in a row. While that rally has been good to see, I tend to be skeptical of any stock market rally that comes in the midst of a larger selloff. Wall Street loves to throw head fakes and phony rallies our way.

A good sign of a true turnaround is when the S&P 500 crosses above its 50- and 200-day moving averages. We’re still a long way from that happening.

The stock market’s last all-time high was on January 27. Interestingly, the drawdown really didn’t start moving until February 25, but since then, the S&P 500 hasn’t been able to get much momentum against the bears.

Frankly, Tuesday was a rather blah day for the markets. At one point, shares of Apple were down by 5%. There was talk of engineering delays in its foldable iPhone. Shares of Home Depot, Trade Desk and Kimberly-Clark all made new 52-week lows today.

There are a few things coming soon that could alter Wall Street’s outlook. The first would be a quick resolution to military operations against Iran. I wouldn’t even try to guess what could happen, or when, but this is a major concern for investors. The price for oil has been rallying again. Oil has recently been as high as $115 per barrel, and it’s not far from its big jump at the start of this conflict.

Another big event coming our way will be Q1 earnings season. The unofficial kickoff of earnings season comes next Tuesday, April 14. That’s when JPMorgan, Citigroup, Wells Fargo, BlackRock and Johnson & Johnson are due to report. Not long after that, the earnings reports will come in a big flurry.

The big banks tend to report early in the earnings season. In fact, Goldman Sachs will report on Monday, but it may be the only major bank that will do that.

The other big event will come at the end of April when the Federal Reserve meets again. It’s very doubtful that the Fed will make any move on interest rates, but we may learn more what the Fed has planned for later this year.

At the moment, Wall Street seems unconvinced that the Fed will do much of anything over the next several months. In fact, traders don’t expect any move—up or down—from the Fed over the next 12 months.

Dissecting Nike’s Fall

In today’s issue. I want to take a closer look at Nike (NKE). The former all-star is stuck in the mud, and it can’t seem to do anything right.

As investors, we want to look at any lessons we can draw from Nike. It’s a good reminder that in a free enterprise system, no company is safe. Time and chance happeneth to us all.

Here’s a weekly chart of the last five years:

Last week, shares of Nike got taken to the woodshed. In one day, the sneaker company lost over 15% of its value, and it’s continued to slide from there. Nike had been falling going into last week’s big drop. In fact, Nike has been sliding for a few years.

As investors, it’s important for us to examine why and how good companies can go off the rails.

Since Nike’s all-time high in November 2021, the stock has fallen more than 75%. Remember that on Wall Street, one 75% drop is effectively two back-to-back 50% drops. This is a massive reversal of fortune. In the 37 years prior to Nike’s peak, the stock gained 18,000%, and that’s before dividends.

What went wrong? The short answer is—everything. The stock is back to where it was 12 years ago. Nike now has a market value of about $62 billion which makes it the smallest member of the Dow Jones Industrial Average. For some perspective, Nvidia is about 70 times more valuable than Nike.

It’s as if they looked at the competitive landscape and then decided to do everything wrong. There are a lot of lessons to be learned here.

Nike held an all-hands meeting this week. CEO Elliott Hill, who was called out of retirement to lead the sneaker outfit, said, “I’m so tired, and I know you are too, of talking about fixing this business.”

Nike beat earnings, but the details were not good. For the quarter, Nike made 35 cents per share on revenue of $11.28 billion. Wall Street had been expecting 28 cents per share, Still, there are many problems for Nike. For example, Nike’s margins continue to shrink, and sales in China fell by 7%.

Sales are basically flat in North America even though earnings are getting smaller. Nike said that sales will fall between 2% and 4% this quarter, and sales in China are expected to be down by 20% for the year.

Flat sales and lower margins mean they’re slashing prices just to tread water. That’s the thing about business: there’s no easy way out of a lousy product.

Here’s a chart that says a lot. This is NKE’s percentage gain over the last 40 years:

What’s particularly frustrating is that Nike has already been in turnaround mode, but it’s simply not showing results. The company said it needs more time, but at some point, they need to rethink their strategy. Shareholders have been very patient, and now they’re not. The benefit of telling shareholders that you’re in a turnaround strategy is that it grants you leeway to make major changes, but Nike hasn’t done that.

The company, especially previous management, made several missteps. For example, Nike placed too much emphasis on direct-to-consumer (DTC) sales. This came at the expense of their partners for wholesale business (think department stores).

This move completely backfired. This strategy alienated retailers, who then gave more shelf space to Nike’s competitors. The wholesale numbers have gotten a little better, but that took a lot of discounting, and that comes at the expense of margins.

Nike also tended to rest on its laurels. They assumed their old best-sellers would carry the load. With footwear, you have to be fresh. That means sports and athletes. Once your shoe becomes uncool, your competitors will eat you alive.

Nike’s other big problem is China. Nike had done well in China, but domestic competition and a bloated inventory of older shoes drove China’s business down. Sales in China are expected to be down by 20% this year.

Then there are tariffs. Oh boy, this a tough one. Nike’s shoes are made in the developing regions of Asia, particularly China and Vietnam. New U.S. tariffs are expected to add over $1 billion in costs. That will hit gross margins. Nike is working to diversify its supplies, but that will take time.

There are some reasons for (limited) optimism. Wholesale is looking a little better. Margins could stabilize soon. The brand is still strong, and it’s known all over the world. Of course, the stock price is low. Or it’s lower than where it was.

In FY 2024, Nike made close to $4 per share. This year, they’ll probably make $1.50 per share. Next year, maybe $1.85 per share. Is that worth $42 per share? Not to me. I won’t even consider Nike until the company has shown evidence that business has improved.

That’s all for now. The GDP report will be this Thursday, and the CPI report will be on Friday. Stay tuned! I’ll have more for you in the next issue of CWS Market Review.

– Eddy

-

Morning News: April 7, 2026

Posted by Eddy Elfenbein on April 7th, 2026 at 7:02 amUnderwater Mortgages Force China’s Banks to Get More Creative

Trumpworld’s Growing Sway in Arms Sales on Display in Rome

UK Signals It Won’t Let US Use Bases for Strikes on Iran Energy

Hungary to Agree to Buy Oil From US at Orban-Vance Meeting

Markets on Edge as Trump’s Iran Ultimatum Looms

Traders Brace for Trump’s Iran Deadline as Frustration Grows

High Gas Prices Will Haunt the GOP Even If the War End

US Inflation Shows Worrying Parallels With 2022 Price Surge

The American Gas Exporter That Pulls In Billions During Energy Shocks

The K-Shaped Economy’s Defining Statistic Has Some Problems

How Bill Phillips Used Flowing Water to Model the Economy

Economic Growth Is the Cause of the National Debt, Not Its Solution

This Is Starting to Look Like a Slow-Motion Bank Run

Is Donald Trump About To Do What Gold Bugs Never Could?

BNY and Robinhood Will Help Run ‘Trump Accounts’ for Children

Retirement Security Requires Modern Investment Access

Depressed Tech Valuations Could Offer Entry Point for Investors, Goldman Sachs Says

Goldman Says It’s Ready to Pounce as Retail Flees Private Credit

Blackstone Hits $10 Billion Cap for Opportunistic Credit Fund

Anthropic in Talks to Invest $200 Million in New Private-Equity Venture

BlackRock, State Street Target Invesco’s $379 Billion Tech Grip

Why Taxpayers Shouldn’t Rely Exclusively On AI

Silicon Valley’s Hottest AI Metric Is Also Its Least Trusted

AI-Displaced Workers Could Face Long Setbacks, Report Finds

The Workers Opting to Retire Instead of Taking on AI

Microsoft Plays Catch-Up in Data Center Build-Out

Battery Giant CATL Taps Zijin Founder as Advisor for Mining Arm

Blockbuster SpaceX Listing Could Suck the Oxygen Out of Fragile IPO Market

Why Is the NYT Laundering the Reputation of a Sleazy AI Startup?

Ackman Pitches $65 Billion UMG Deal for US Listing, Stock Boost

Kanye West Is Seeking Redemption. There’s a Long Road Ahead.

The FCC May Rescue Frustrated NFL Fans

Doritos at $7 a Bag Ended Up Costing PepsiCo Billions

The Viral Japanese Planner That Has TikTok Getting Organized

Be sure to follow me on X.

-

Morning News: April 6, 2026

Posted by Eddy Elfenbein on April 6th, 2026 at 7:08 amIraq Tells Buyers to Collect Crude as Oil Can Cross Hormuz

Hormuz Traffic Rises to Highest in Weeks

Oil Swings as Traders Gauge Report of Push for Iran Ceasefire

One Gas Station, 12 Customers, and a Test of America’s Patience

It’s a Jackson Browne Economy: Running On Empty

OPEC Plus Warns of Slow Recovery After War in Iran

Trump’s Answer to Iran’s Hormuz Crisis: Sell Oil We Don’t Have

Trump’s Iran Deadline Looms With Mediators Pushing for Truce

America’s Diplomat Shortage Is a Self-Inflicted Wound

King Charles Can Handle a Boorish White House

Canadian Confidence Hits 11-Month Low as Iran War Drags On

This Is Not China’s War, but Beijing Started Preparing for It Years Ago

Who Knew ‘Slick’ Gavin Newsom Was Such an Economic Maestro?

Dimon Urges US to ‘Get Stronger,’ Keep Economic, Military Power

Goldman Sachs Private Credit Fund Defies Redemption Surge Across Industry

Government Shouldn’t Dictate How Online Markets Operate

The Wall Street Dealmaker Charged With Solving Paul Weiss’s Identity Crisis

Debanking Is a Confusing Nightmare. It’s at Risk of Getting Worse

State Climate Laws Targeted Around US as Iran War Spikes Gas Prices

Peter Thiel’s Big Bet on Solar-Powered Cow Collars

Industrial Firm Madison Air Seeks to Raise $2.23 Billion in IPO

SpaceX Heralds New Era of Mega IPOs. Buyers Beware

OpenAI Advocates Electric Grid, Safety Net Spending for New AI Era

Chinese Battery-Storage Supplier Sees Shipments Doubling in 2026

Neurocrine to Buy Soleno for $2.9 Billion

Pesticide Giant Syngenta Readies New Weapon Against Superweeds

Gulf Funds Agree to Back Paramount’s $81 Billion Takeover of Warner

‘Super Mario’ Sequel Scores Year’s Biggest Movie Opening

Baseball’s Robo-Umps Aren’t Ready to Replace The Real Umpires Yet

Fight Over Feta Strains America’s Ties With Europe

Be sure to follow me on X.

-

Morning News: April 3, 2026

Posted by Eddy Elfenbein on April 3rd, 2026 at 7:02 amTake Hormuz by Force? France and Britain Have Better Ideas

Macron Criticizes Trump and Calls on Allies to Unite Against US

Rival Nations Seize On Choke Points to Counter Trump

Tanker Carrying Iranian Crude Shifts Course from India to China

Iran Strikes Gulf Energy Sites as Trump Warns of Further Attacks

Bombing Iran’s Great Mosque Could Cost the World

Israel Resumes Biggest Gas Field After War Shut It for a Month

Fed’s Logan Says US Oil Producers Unlikely to Provide Near-Term Relief for Consumers

Jefferies Says UAE Injected $8 Billion Liquidity to Help Lenders

How Insulated Is the U.S. Economy From the Iran War?

Trump Budget Pits Spending Cuts Against Massive Defense Push

Blue Owl Reels as Investors Who Fueled Its Growth Now Want Out

401(k) Investment Menus Need a Reboot

Tariffs Strained U.S. Aluminum Supplies. Now the Iran War Is Making It Worse

U.S. Steel Tariffs Hurt America, Help China

A Bottle of Wine Shows the Slow-Motion Impact of Trump’s Tariffs

Trump Administration Unveils Up to 100% Tariff on Branded Drugs

JetBlue Raises Checked Bag Fees as Fuel Costs Soar

Amazon to Apply 3.5% Fuel Surcharge to Third-Party Sellers

Economists Once Dismissed the A.I. Job Threat, but Not Anymore

Jobs and Workers Are in Balance. Nobody Is Happy About It.

Skilled Foreign Workers Think About Leaving the U.S.

Bondi’s Firing Is Actually Good News

Trump’s Media-Bashing Is Coming Back to Bite Him in Court

SpaceX Targets More Than $2 Trillion Valuation in IPO

It’s Not Easy Being a Trillionaire

Under the Skin of America’s Humanoid Robots: Chinese Technology

Google/Meta Verdict: A Whole Lot of Nothing to Feed the Perpetually Alarmed

Google Workers Find It’s a Different Era for Activism

A Nintendo Cinematic Universe Can Learn From Marvel

Will Nike CEO’s Candor With Staff Have Any Effect on Performance?

Be sure to follow me on X.

-

Morning News: April 2, 2026

Posted by Eddy Elfenbein on April 2nd, 2026 at 7:05 amIran War Showcases Strength of South Korean Defense Sector

Macron Says Trump Weakens NATO by Casting Doubt on US Commitment

Trump Stirs Market, Political Angst With Vague Timeline for Iran

Defeat Has Never Sounded as Victorious as in Trump’s Address

U.S. Lifts Sanctions on Venezuela’s Leader, Opening Door to Deals

Tracking Trump’s Tariffs Across the Global Economy

Tariff-Struck Companies Exploring Loans Backed by Refund Claims

How Swap Markets Are Struggling to Gauge Rates as Iran War Fuels Volatility

Hedge Funds Walloped by a Month of Turmoil Sparked by Iran War

Mark Meador and the FTC Scarily Revive Teddy Roosevelt Economics

There’s a Competition Crisis, Not An Affordability Crisis

Institutional Investors Are Asking To Do Your Worrying For You

KKR Secures $23 Billion for Americas PE in Its Largest-Ever Haul

Antisemitic Violence Sparks $765 Million in Security Spending

Nursing Is the Surefire New Path to American Prosperity

140 Million Americans Are Locked Out of Low-Cost Access to Healthcare

How A.I. Helped One Man (and His Brother) Build a $1.8 Billion Company

SpaceX Files to Go Public, Setting Stage for Huge I.P.O.

A $45,000 Porsche Taycan Is a Decent Oil Price Hedge

G.M. Reports Sharp Decline in Car Sales Amid War and High Prices

Foreign CEOs Face More Scrutiny. Air Canada’s Earned It

US Job-Cut Announcements in Tech Keep Rising With AI Adoption

Microsoft CFO’s AI Spending Runs Up Against Tech Bubble Fears

Europe Pushes for a Gentler Internet for Children

Goodbye ‘Geeky Hunk’? Gmail Users Can Now Change Their Usernames

Louis Vuitton, Gucci, Prada … Meta?

TotalEnergies, Masdar Form $2.2 Billion Asia Renewables Joint Venture

State Farm Is in Trump’s Crosshairs Over L.A. Fires

How a Sapling and a Viral Candy Made California the World’s Pistachio King

The IRS Chief, His Old Pal and the Case of Muhammad Ali’s Missing Pair of Shorts

The Women Who Love the Manosphere

Six Flags Was a Summer Destination. Can It Win Families Back?

Be sure to follow me on X.

-

Morning News: April 1, 2026

Posted by Eddy Elfenbein on April 1st, 2026 at 7:01 amGlobal Ban on Digital Duties Expires After Stalled Talks at W.T.O. Meeting

Iran War Hobbles Myanmar Economy as Gasoline Supplies Disappear

Some French Gas Stations Run Dry as Price Caps Spur Rush to Fill

Ukraine Is Having a Surprisingly Good Iran War

The Dubai War Narrative Is Looking a Little Stretched

Four Passover Questions as the Iran War Nears Endgame

Stocks in Asia Rally and Oil Prices Rise

Bank of England Says Iran War Has Boosted Threats to Financial Stability

Dimon Says Vital US Ensures Iran War Is ‘Successfully Completed’

Indian Rupee Set for More Chaos as Banks Unwind $30 Billion in Arbitrage Trades

The Economy Is on the Edge. What Could Tip It Over, or Help It Pull Through.

Prediction Markets Are An Essential Driver of Better Decisions

Bearish Positioning Is Driving Stocks More Than Peace Prospects

Wells Fargo Unleashes Pent-Up Power in Crucial Repo Market

Is U.S. Housing Starting to Crash?

Institutional Investors Are the Housing Solution, Not the Problem

Trump’s Executive Order on NPR and PBS Is Unconstitutional, Judge Rules

The Year Is Off to the Strongest Start for Big Deals Ever

Global First-Quarter M&A Exceeds $1.2 Trillion, Led By AI

The 322-Foot Tall Rocket for NASA’s Moon Flyby

America Now Has an EV Rust Belt. High Gas Prices Won’t Rescue It.

Anthropic Accidentally Posts Source Code of Claude AI Agent

Oracle Lays Off Workers Amid Heavy AI Investment

Google Faces Demands to Prohibit AI Videos for Kids on YouTube

Big Drug Companies Hunting for Deals Are Lowering Their Sights

Nike Guides for Sales Declines Ahead as Turnaround Plan Hits Snags

Allbirds, Once Silicon Valley’s Favorite Shoe, Sells for $39 Million

Ken Paxton Should Know That Government Can’t Lower Ticket Prices

Las Vegas Is Still a March Madness Mecca

Be sure to follow me on X.

-

CWS Market Review – March 31, 2026

Posted by Eddy Elfenbein on March 31st, 2026 at 7:05 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

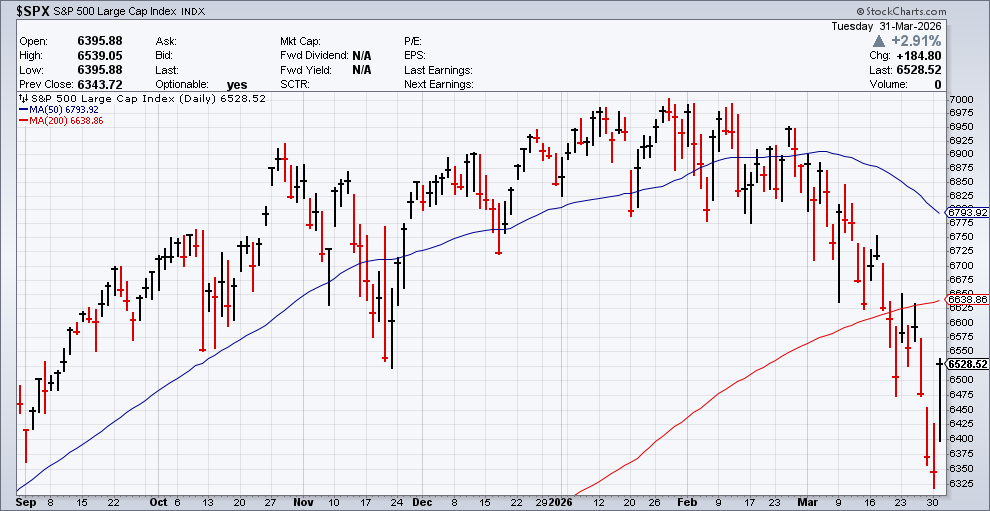

The first quarter came to an end today, and it was a difficult one for Wall Street. We started off the quarter, and the new year, just fine. By January 27, the S&P 500 reached an all-time closing high. Then on February 6, the Dow Jones Industrial Average closed above 50,000 for the first time ever.

Then in the middle of the quarter, things started to change as the market had to deal with the ramifications of military operations in the Middle East. The Strait of Hormuz was shut down and the price of oil shot to more than $100 per barrel. It’s still up there as I write this.

Now the damage is being felt on Wall Street and on Main Street. The price for a gallon of gas is now above $4. In recent days, the Dow closed more than 10% off its high which is the traditional definition of a market correction.

Here’s how the three major indices performed during Q1:

S&P 500: -4.63%

Dow Jones Industrial Average: -3.58%

Nasdaq Composite: -7.11%

The S&P 500 closed Monday at 6,343.72 which marked its lowest close since August 7, 2025. The index is currently below its 50- and 200-day moving averages. It’s not in correction territory yet, but it’s getting close.

March turned out to be the worst month for stocks in more than a year, and Q1 was the worst quarter for the S&P 500 in nearly four years. If we measure from the market’s high in February 2025, then the stock market has barely advanced — and adjusted for inflation, the market is basically flat for 13 months.

The Mag 7 stocks, in particular, have not fared well. All seven lost ground during Q1:

Google is missing from the chart because I’m only allowed six lines at once. For the quarter, Google lost 8.06%.

The stock market had a big relief rally on Tuesday (+2.91%). I tend to be skeptical of outsized “contra-trend” rallies. This is when the stock market does exactly the opposite of what it had been doing, and it does it by a lot. Don’t get me wrong. I’ll welcome any rally, but days like today seem more like temper tantrums rather than optimistic rallies.

The stock market rallied after the president of Iran said that his government might be open to ending the war. The Dow rallied over 1,100 points today and the Nasdaq was up 3.83%.

Earlier today, the Labor Department’s JOLTS report said that hiring in February fell to its lowest level in six years. This week, we’re going to learn a lot more about how well the economy is performing. Tomorrow, ADP will release its monthly report on private payrolls. Wall Street expects to see a gain of 39,000 jobs.

We’ll also get the retail sales report for February. If you recall, the report for January was not terribly good. For tomorrow, Wall Street expects to see a gain of 0.5%, and a gain of 0.3% excluding autos. At 10 a.m. ET tomorrow, we’ll get the ISM Manufacturing Index.

That leads us to Friday and the big March jobs report. This report will be a little unusual in that the stock market will be closed on Friday for Good Friday. This means that we’ll have to wait until Monday to see the market’s reaction.

For Friday’s report, Wall Street expects to see a gain of 59,000 jobs. For February, the economy lost 92,000 jobs. Analysts also see the jobless rate staying at 4.4%. Hourly average earnings are expected to rise by 0.3%. That’s not bad, but I hope to see better numbers.

This leaves the Federal Reserve in a difficult position. The jobs market is weak, and commodity prices are rising. The economy would certainly benefit from lower prices, but the inflation may be too precarious to ignore.

The Fed meets again in four weeks, and it will be Jerome Powell’s final meeting as Fed Chair. Now it looks like the Fed may not touch interest rates before the end of this year. In fact, they may not make any changes to rates for another 16 months. That’s according to the latest futures prices.

Stryker Hits New 52-Week Low

I wanted to highlight Stryker (SYK) this week. The stock has been on our Buy List for the last 19 years in a row. It’s a wonderful company, and I’m glad we’ve owned it.

Lately, however, the shares haven’t performed very well. The company was also the victim of a nasty cyber-attack. Fortunately, most of its systems are back up and running. Today, shares of Stryker got down to a new 52-week low. The stock is back to where it was nearly two years ago.

Here’s a look at 40 years of SYK:

It’s hard to find a point when it wasn’t a good time to buy Stryker. This is also a good example of Elfenbein’s Law: “When a stock has done so well that the legend for the vertical axis is unreadable, that’s probably a good sign.”

In January, Stryker reported very good numbers for Q4. Earnings rose 11.5% to $4.47 per share. That was eight cents better than expectations. Stryker’s own guidance had been for $4.34 to $4.44 per share.

Net sales were up 11.4% to $7.2 billion, and organic sales were up 11.0%. Stryker’s operating margin increased 100 basis points to 30.2%. For the year, Stryker made $13.63 per share. That’s up 11.8% over last year.

Here’s a look at Stryker’s annual earnings:

For 2026, Stryker expects earnings between $14.90 and $15.10 per share, and organic-net-sales growth of 8.0% to 9.5%. If that’s correct, then it would be another good year for SYK.

That’s all for now. The stock market will be closed on Friday in honor of Good Friday. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

-

Morning News: March 31, 2026

Posted by Eddy Elfenbein on March 31st, 2026 at 7:08 amWar’s First Inflation Hit Arrives in the Euro Area

China’s Pivot to Vietnam Blows Hole in Trump’s Made-in-USA Plan

Why Is the Japanese Yen So Weak — and Will Authorities Intervene?

A $50 Trillion National Debt In 2030 Will Signal Opposite of Debt Problem

US Bonds Are Caught in a Tug-of-War Between Inflation and Growth

Powell Says Fed Can Look Past Oil Shock, but Warns Patience Has Limits

Oil and Gas Prices Continue to Rise in Choppy Trade

Energy Stocks Set to Beat Broader Market by Biggest Margin Ever

Fresh Food Distributors Add Surcharges as Fuel Costs Rise

Trump Tax Law’s Expansion of Affordable Housing Credit Hits Snag

Government Attacks on Credit Cards Won’t Bring Down Prices

Private Lenders Delay Reckoning with Payment Concessions on Stressed Debt

U.S. Banks Raising Borrowing Costs for Private Credit Funds as AI Fears Pummel Valuations

JPMorgan Takes On American Dream in Latest Firmwide Initiative

Private Equity’s Growing Appetite for Fast Food in Japan

Japan Is Placing a Multibillion-Dollar Bet on the US Housing Market

Lilly to Buy Sleep Drug Maker Centessa in $7.8 Billion Deal

Biogen to Buy Apellis for $5.6 Billion to Boost Kidney Franchise

Unilever Food Arm to Join With McCormick in $44.8 Billion Deal

Unilever’s $40 Billion Food Sale Augurs a More Beautiful Future

Whoop Raises $575 Million at a $10 Billion Valuation on Its Way to an IPO

Google Partner Tenex Raises $250 Million for AI Security Services

The Sudden Fall of OpenAI’s Most Hyped Product Since ChatGPT

Exxon Scientists Had Doubts About Algae Biofuels. The Oil Giant Touted Them Anyway.

Delta to Tap Amazon Satellite-Internet Service for In-Flight Wi-Fi

Hegseth’s Culture Wars Are Inviting a Military Disaster

A Crackdown on Dreamers Is a Crackdown on the American Dream

The DC Streetcar Was Desired. It Just Wasn’t Worth It

How a Massive KitKat Heist Turned Into Crisis PR Gold

Be sure to follow me on X.

-

Archives

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His