CWS Market Review – June 17, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The stock market was shaken a bit on Friday after geo-political events dominated the news. On Monday, the market made back much of what it lost but today was another down day. The S&P 500 closed below 6,000 for the second time in three days.

During these kinds of events, Wall Street tends to be much calmer than the talking heads on TV. The Volatility Index is back over 20 which still isn’t very high. Compare that with April when it got as high as 60.

Over the past two months, overall volatility has decreased markedly. There simply aren’t a lot of intra-day movements. Earlier this year, we saw several big intra-day swings. I’m happy to say that Wall Street has really chilled out from the tariff panic this past spring.

The price for oil spiked, but even that has started to cool off.

This week, Wall Street seems less interested in Iran and more interested in the upcoming Federal Reserve meeting. The Fed will release its policy statement tomorrow at 2 pm ET and it’s very doubtful that we’ll see a rate cut. Traders currently place the odds of a 0.25% cut at 0.2% which, in my opinion, is about 0.199999% too high.

The Fed probably won’t resume cutting rates until after Labor Day, and that’s at the earliest. There’s even a good chance that rate cuts won’t happen until October. Goldman Sachs said the Fed won’t cut until December. Meanwhile, interest rates are having an important impact on retail sales, the housing market and which kinds of stocks are doing well. I’ll explain it all in a minute.

Also with this week’s Fed meeting, the Fed will release its Summer of Economic Projections. Frankly, the Fed has a pretty lousy track record of predicting the economy (remember that “transitory” inflation?), but it’s still interesting to see what the Fed expects. While inflation has been better behaved, it looks like we’re not returning to the pre-Covid world of sub-2% inflation. This is the new reality.

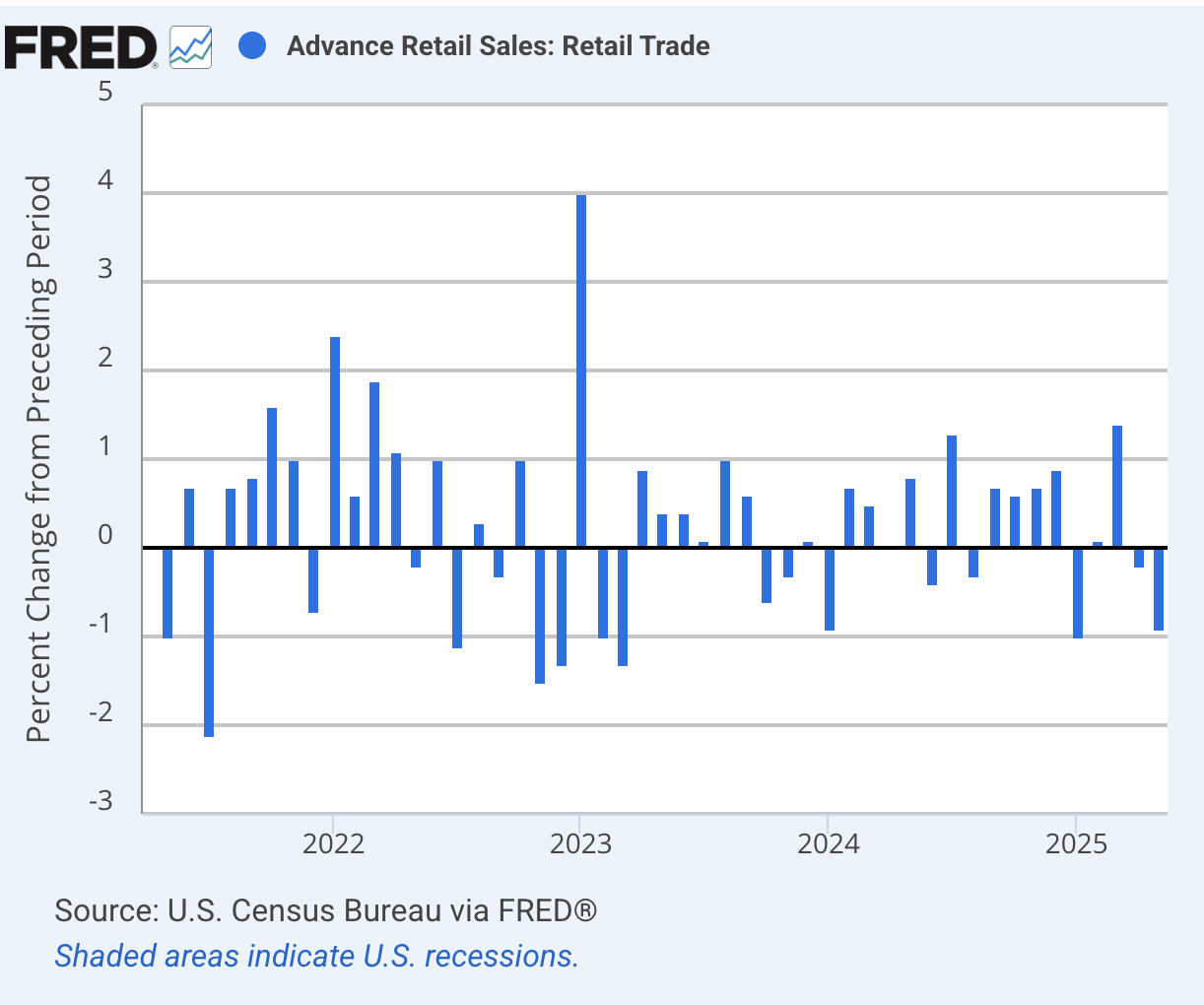

May Retail Sales Fall 0.9%

We’ve had a few disappointing economic reports this week. I’m not worried just yet, but it’s something to be aware of.

For example, this morning, we got the retail sales report for May, and it wasn’t good. Last month, retail sales fell by 0.9%. That was 0.3% worse than expected. Apparently, shoppers weren’t in a spending mood last month. Bear in mind that consumer spending makes up about two-thirds of the economy.

During April, retail sales fell by 0.1%. Over the last year, retail sales are up by 3.3%. That’s pretty weak.

If we don’t include cars, then sales fell by 0.3%, which was also worse than expected. Economists had been looking for an increase of 0.1%.

Building materials and garden stores saw sales fall 2.7%, while sliding energy prices pushed gasoline station receipts down 2%. Motor vehicles and parts retailers were off 3.5%, while bars and restaurants saw sales decline 0.9%.

On the plus side, miscellaneous retailers gained 2.9%, while online sales rose 0.9% and furniture stores increased sales by 1.2%.

The data from the prior months was probably impacted by consumers rushing to get deals before the tariffs went into effect. We recently got the report from the University of Michigan on consumer confidence, and it showed an impressive rebound, but this comes after a few disappointing months.

Another troubling report said that homebuilders are in a terrible mood. This is important because the housing industry drives so much of the economy.

For June, the Homebuilder Sentiment Index fell two points to reach 32. Any number below 50 is bad, and this is very bad. This is the third lowest print in the last 13 years. Wall Street had been expecting an improvement.

The survey showed that 37% of homebuilders said that they had to cut prices. That’s a three-year high. The average price reduction has been 5%. If the housing market isn’t happy, then it’s very hard for the overall economy to be happy.

There’s even a famous academic paper titled “Housing IS the Business Cycle.” I think that’s exactly right. The Federal Reserve also said that industrial production fell 0.2% last month.

I’m looking ahead to the Q3 GDP which is due out late next month. The GDP report for Q1 was a dud. It showed a decline of 0.2%, but Wall Street is expecting a rebound for Q2. The Atlanta Fed’s GDPNow model now sees Q2 growth of 3.5%. (That’s annualized and adjusted for inflation.)

I know the Fed doesn’t want to be the one to rescue the economy. I’m not sure it can, but I think it will give it a shot. I do expect interest rates to be lower by the end of the year.

The Market’s Tilt Away from Defense

One concern I have is that over the last two-and-a-half months, the market’s gains have been heavily concentrated in growth stocks. That’s to be expected at the start of a rally, but I’m skeptical that growth will continue to leave value in the dust.

Here’s a chart that I think shows a lot. This is the relative strength of consumer staples and healthcare stocks. I ran the chart on healthcare recently, but this week I want to show how it stacks up against consumer staples.

As you can see, the two lines are like waltzing partners.

Let me take a step back and explain this for a moment because it’s a subtle point that investors should understand. I call it “The Elfenbein Theory to Explain the Entire Stock Market.”

Broadly speaking, stocks tend to fall into one of four groups. The groups are value, growth, defensive and cyclical. The relative strength of value and growth sectors tend to move in opposite directions (but not always!). Likewise, the relative strength of defensive and cyclical sectors also tend to move in opposite directions. The cyclicals move in cycles. The defensives don’t (but not always!).

The value-growth dimension tends to align with short-term interest rates. Rates go down, value leads. Rates go up, growth leads (but not always!).

The cyclical-defensive dimension tends to align with long-term interest rates. Long-term rates go down, defensive stocks lead. Long rates go up, and cyclicals lead. (But not always!).

I’m sure the super-smart kids out there picked up on something: “Hey Eddy, can’t you make a quadrant of those groups?” Yes, you can! There are also periods when short-term and long-term interest rates move in opposite directions. In simple terms, this is when the yield curve gets wider or narrower, and it impacts financial stocks.

This brings me back to the graph. The key defensive sectors are consumer staples and healthcare. Investors tend to like these stocks because their business tends to be more stable. You may not think a consumer staple like Hershey (HSY) or Colgate-Palmolive (CL) is similar to a healthcare name like Abbott Labs (ABT) or Stryker (SYK), but the stock charts certainly think they’re similar.

Lately, however, these stocks have been in Wall Street’s doghouse. The defensive sectors have lagged the market for two-and-a-half years. I don’t think this can last much longer. If the economy gets weaker, investors will lean towards these areas of the market, and there will be a lot of bargains. The rotation probably is not far away.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on June 17th, 2025 at 7:16 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His