CWS Market Review – August 19, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Wall Street Is Focused on Jackson Hole

This week, most of the world’s attention has been on the diplomatic meetings in Washington that are trying to end the Russia-Ukraine War. But on Wall Street, traders have been focused on the Federal Reserve’s annual late-summer conference in Jackson Hole, Wyoming.

In previous years, the Fed has used the Jackson Hole conference to announce major policy decisions. Fed Chairman Jerome Powell will be delivering his speech on Friday, and he’s expected to give greater clarity to the Fed’s plans for the economy and interest rates. This will likely be Powell’s last Jackson Hole conference as Fed chair.

The Jackson Hole shindig is sponsored by the Kansas City Fed. The KC Fed has been running the conference since 1978. It moved to Jackson Hole in 1982 because, it’s said, Paul Volcker wanted to get in some fly fishing.

Tomorrow, the Fed will release the minutes from its last meeting. In July, the Fed again decided to forgo any rate cuts. There were, however, two dissenting votes on the Fed, which is unusual. There could be more members thinking about breaking ranks, but we don’t know yet. The Fed isn’t known for its transparency, but it does like to show a united front.

The most likely scenario is to expect the Fed to cut rates next month. After that, things get a little murky. Still, I think it’s reasonable to expect at least one more rate cut between July and the end of the year. Let me be careful to say that there are still a lot of unknowns floating around out there. In recent days, for example, we’ve had conflicting news on the economy.

After reaching an all-time high last Thursday, the S&P 500 had minor drops on Friday, Monday and today. Today’s market was noteworthy because the High Beta sector again lagged the market. This is the third time this has happened in the last four days. Not long before that, there was a period when High Beta lagged for five days in a row. This is probably a reaction to lower interest rates.

Has the High Beta cycle ended? I’m not willing to say just yet. For over four months, High Beta stocks have done very well. Perhaps too well. I’m skeptical that High Beta will do well in the coming weeks and months. These recent sessions could be an omen for a longer-term rotation away from High Beta and towards Low Vol. At some point, those boring stocks will look attractive.

Now that earnings season is over, this is when we get many of the off-cycle earnings reports. In particular, many retailers are due to report this week. A lot of retailers prefer to have their quarters end in January, April, July and October. That way, the important holiday-shopping quarter isn’t cut off early. This week, we’re get earnings reports from big box retailers like Lowe’s (LOW), Walmart (WMT) and Target (TGT).

This morning, Home Depot (HD) reported earnings that were slightly below consensus. The stock rallied today as the company reiterated its full-year guidance. The company also said that it will have to raise some prices due to tariffs. I like to look at HD’s earnings because it tells us a lot about the housing sector and about many independent contractors. This is a vital segment of our economy.

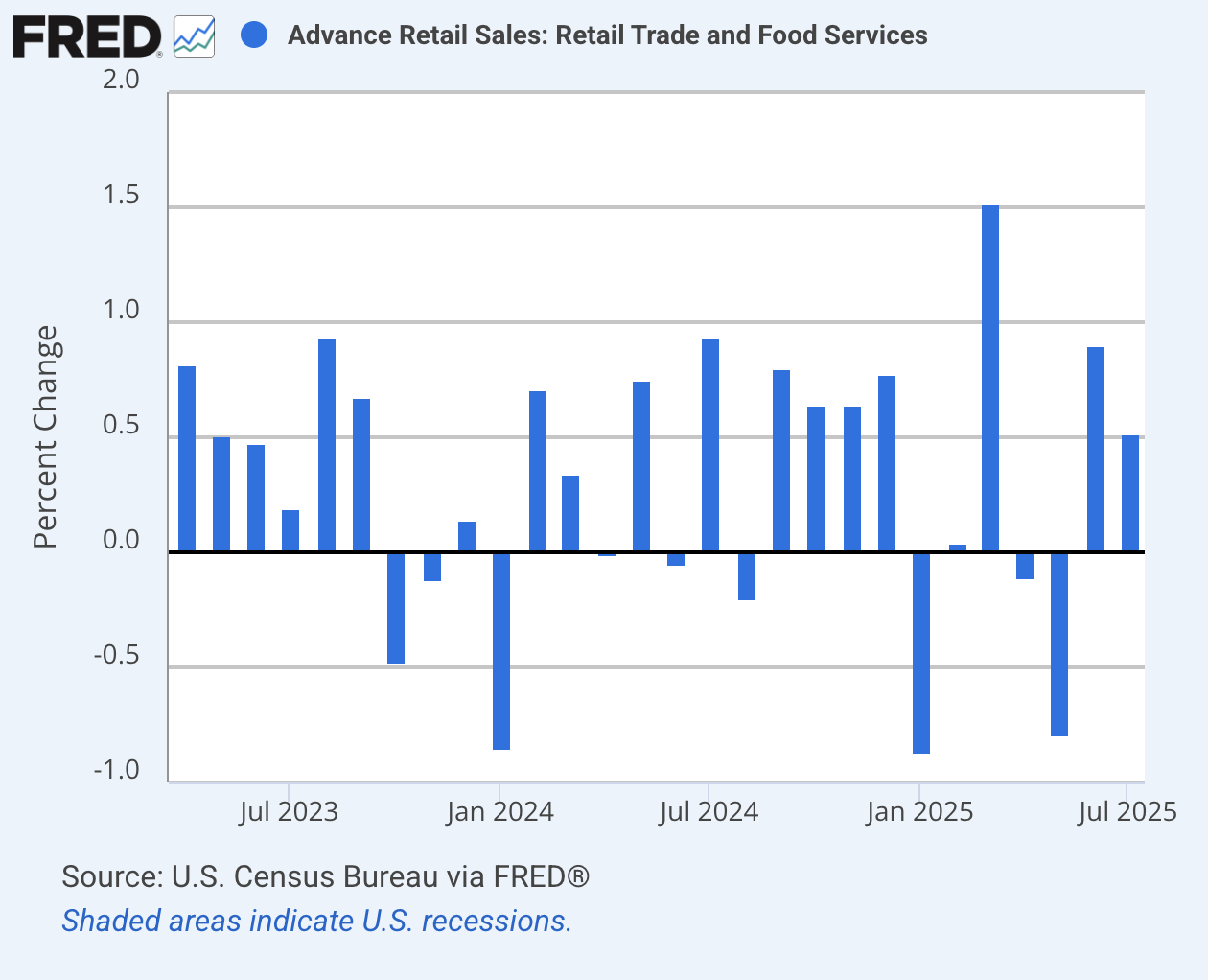

We got another snapshot of the economy last Friday when the retail sales report for July was released. Wall Street had been expecting a 0.6% increase. Instead, retail sales were up 0.5%. That’s not too bad. If we strip out auto sales, then retail sales were up by 0.4% which matched estimates. If we take out autos and gas, then retail sales were up 0.2%.

This was the second month in a row that retail sales increased. That came after two months of lower sales. In fact, the retail sales number for June was revised higher. The initial report showed an increase of 0.6%. Now it’s an increase of 0.9%.

The retail sales report showed so-called control-group sales — which feed into the government’s calculation of goods spending for gross domestic product — advanced 0.5% in July after an upward revision to the prior month. The measure excludes food services, auto dealers, building materials stores and gasoline stations.

Several categories that posted solid gains, such as furniture, sporting goods and cars, also saw some price increases during the month. Because the data aren’t inflation adjusted, an advance could reflect the impact of higher prices.

Spending at restaurants and bars, the only service-sector category in the retail report, fell by the most since February. That doesn’t bode well for discretionary services spending at the start of the third quarter, said Oscar Munoz, chief US macro strategist at TD Securities.

Also on Friday, the Federal Reserve reported that industrial production declined by 0.1% in July. Wall Street had been expecting no change. The sluggish number could be a result of shifting resources ahead of new tariff policies. The Fed also revised higher the industrial production number for June to a gain of 0.4%.

Manufacturing makes up for 75% of all industrial production. The Manufacturing number for June was revised upward to no change. At the start of this year, manufacturing was doing quite well but that’s slowed down in recent months. Lower interest rates could help ease the decline. Since April, the manufacturing sector has lost 37,000 jobs.

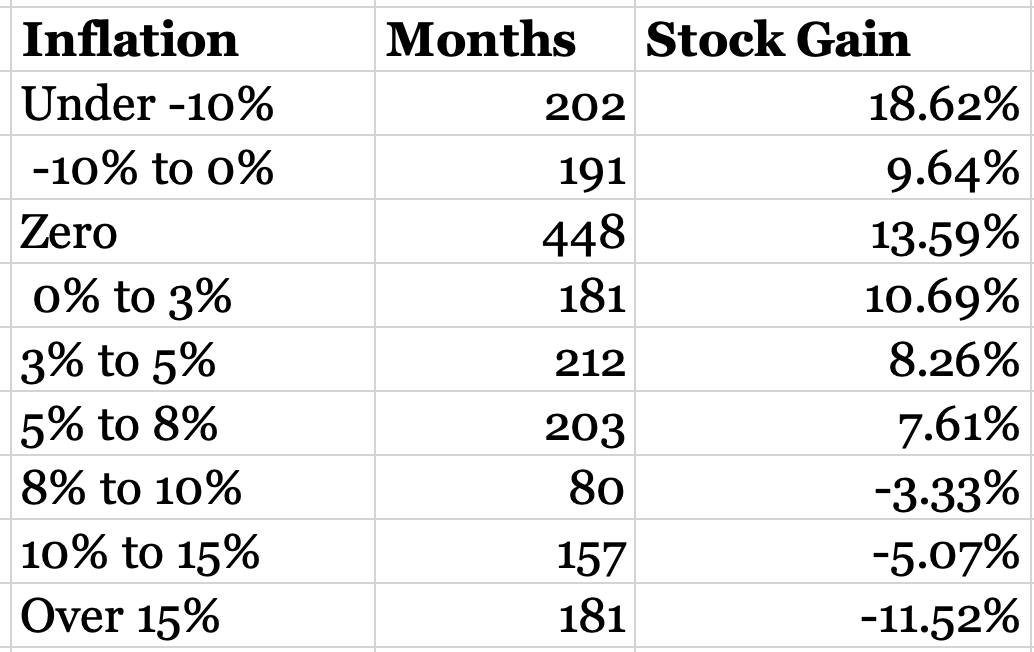

Inflation’s Impact on the Stock Market

I often talk about inflation and the Federal Reserve, but this week I wanted to show why it’s so important. I want to show you how poorly the stock market has performed under high inflation.

I went to Professor Robert Shiller’s data library. He has stock market data going back over 150 years. I took all the monthly market gains and monthly inflation rates. I then sorted all the months by level of inflation. I then calculated the average market return by different levels of inflation.

To make things easier to read, I annualized the data. Here’s what I got:

For example, the monthly inflation was 0% in 448 months. Over those 448 months, the stock market has had an average annualized gain of 13.59%. As you can see, the stock market really takes a nosedive when inflation gets too high. The turning point is about 7.3%. As long as inflation has remained below that, the stock market has done well. Above that is the problem area. The inflation rate is currently 2.7%. The important lesson is that few things kill the stock market quite like inflation.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on August 19th, 2025 at 6:48 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His