CWS Market Review – August 26, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

At Jackson Hole, Powell Hints that Rate Cuts are Coming

Last Friday, Federal Reserve Chairman Jerome Powell gave his highly anticipated speech at the annual Jackson Hole conference in Wyoming. As I’ve explained in previous issues, the Jackson Hole conference is a big deal in the Fed world.

The central bank has used the occasion to announce important policy decisions. This year, Powell told the world to expect interest rate cuts from the Fed. This is hardly news, but it’s noteworthy that Powell used Jackson Hole to make his announcement.

The market celebrated the news and the stock market rallied strongly on Friday. That gain ended a six-day losing streak. The market’s gain on Friday nearly wiped out the entire loss of the preceding six days. The market continued to rally and came close to a new all-time high today.

I get the feeling that Powell is in the hawkish camp at the Fed. By that, I mean that he’s more reluctant than other members to lower rates right now.

The Fed has an unfortunate habit of fighting the last war. The Powell Fed is uniquely concerned with its credibility. Sadly, that took a big hit during the opening months of inflation. If you recall, the Fed said that inflation was merely transitory. Well, that wasn’t the case, and the Fed eventually reversed course and attacked inflation with its full force. Now it needs to relent.

Specifically, Powell said, “With policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.” As you know, your humble editor is conversant in the abstruse language of Fed-speak, which has a distant relationship with proper English. I’ll happily translate.

The Fed has been holding rates high for several months, and the bond market is getting antsy. The White House has also been placing pressure on the Fed to cut rates (more on that later).

The problem for the Fed is the president’s tariff policies. We’re not exactly sure what the effect will be, or even the finalized policy. This places the Fed in the position not knowing what it doesn’t know. There’s also the impact of more restrictive immigration policies.

The Fed’s mandate is to keep inflation low and the labor market happy. That’s not always an easy balance. Powell admitted that “the balance of risks appears to be shifting.”

Overall, while the labor market appears to be in balance, it is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers. This unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment.

At the same time, GDP growth has slowed notably in the first half of this year to a pace of 1.2 percent, roughly half the 2.5 percent pace in 2024. The decline in growth has largely reflected a slowdown in consumer spending. As with the labor market, some of the slowing in GDP likely reflects slower growth of supply or potential output.

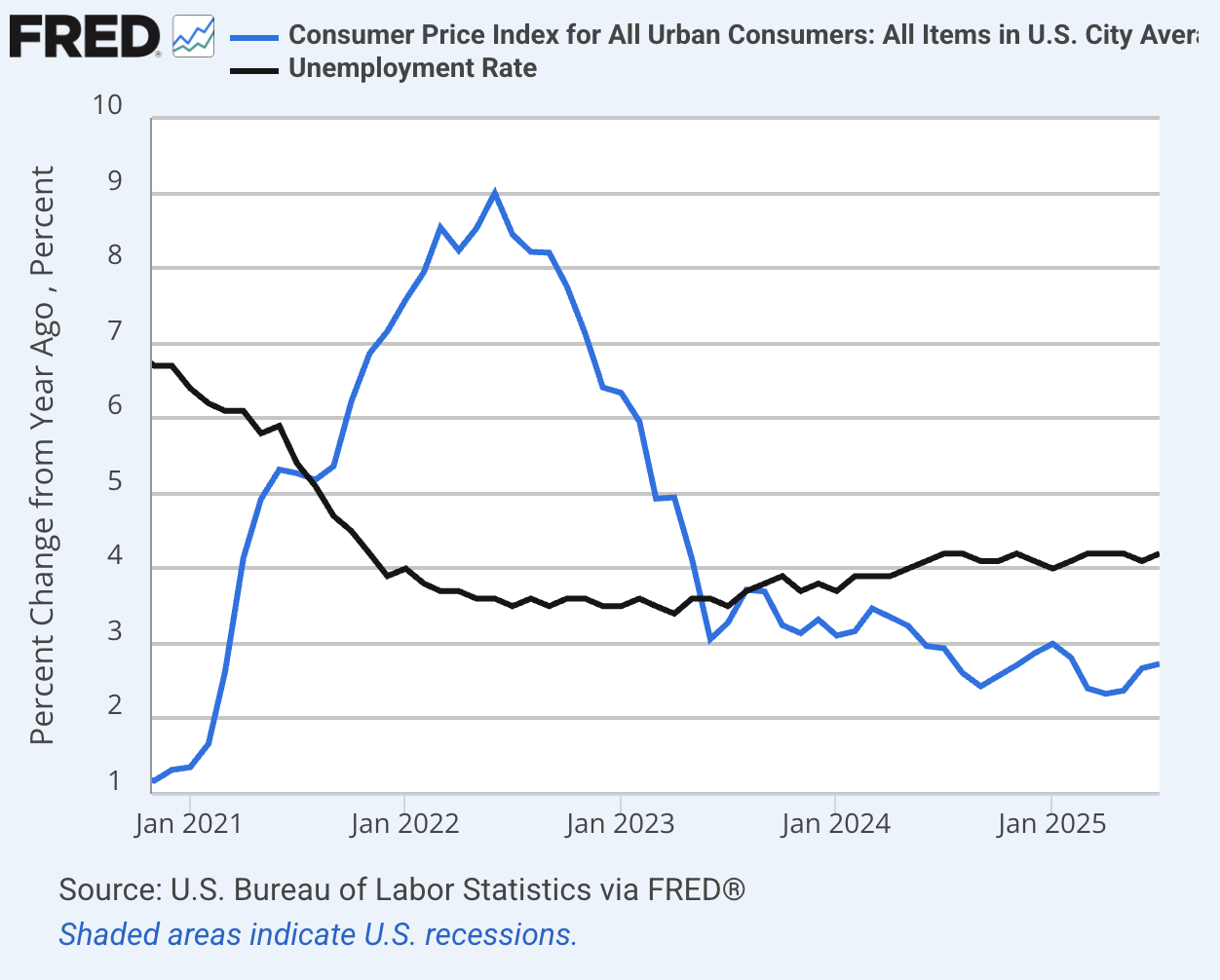

Check out this chart. Inflation is the blue line and unemployment is in black. It looks like the black line is inching up while the blue line is still moving lower:

This is also an unusual time for the Fed because the stock market has been doing well. The unemployment rate is still relatively low. While inflation is down, it’s above the Fed’s target of 2%. The economy isn’t as strong as it could be, but we don’t appear to be near a recession. Wall Street is expecting good numbers for Q3 GDP.

Given these facts, why is there such pressure to cut rates? Part of the reason is simply that the Fed went too far in raising rates, so it may be appropriate to walk that back.

Also, despite some good economic numbers, we’re seeing problems in areas of the economy that are heavily dependent on interest rates, the most important being housing. Over the last two years, the cost of housing – not just home prices but also mortgage costs – have soared. Yesterday, in fact, the Commerce Department released a report showing that sales of new homes dropped by 0.6% last month.

I like to keep an eye on how homebuilder stocks are doing. The homebuilders stand at the intersection of the stock market and interest rates. A good ETF to watch is the SPDR S&P Homebuilders ETF (XHB). Starting last summer, the homebuilders badly lagged the overall market. But in recent weeks, the homebuilders have perked up. I think it’s in anticipation of lower rates.

For now, we can expect the Fed to cut rates in September. After that, things are less clear. I would say the odds are that the Fed will cut again in October or December, but not both. Rate cuts will help alleviate some pressure points within the economy.

Now let’s look at the latest political battle at the Fed.

President Trump Fires Lisa Cook. Or Maybe Not

Sixty years ago, President Lyndon Johnson famously clashed with Fed Chairman William McChesney Martin. LBJ was used to getting his way and he didn’t take kindly to the Fed trying to fight inflation by raising interest rates.

The fight started when the Fed ignored the president’s demand to leave rates alone. Instead, the Fed hiked rates. LBJ was furious. And he summoned Martin to the LBJ ranch where the president was recovering from gallbladder surgery. Depending on whom you ask, LBJ berated Martin and even shoved him around the president’s office.

I bring these events up because on Monday, President Trump fired Lisa Cook, one of the Fed’s governors. Or I should say, he tried to fire her. The courts will most likely sort this all out before we’re done. If Trump prevails, his appointees will have a majority at the Fed.

Let me take a step back to describe what happened. The Federal Reserve is run by its seven-member board. The board is designed in such a way as to reduce political influence. The term of each board member is for 14 years. That way, a president will nominate new board members once every two years.

Board members usually serve around three to five years. Most board members fill in for part of a 14-year term. Note that the Fed board is not the same thing as the interest-rate setting Federal Open Market Committee which is comprised of Fed board members and rotating Federal Reserve bank presidents.

While the president appoints members to the Fed, and the Senate votes on the nominees, the president doesn’t have the power to fire Fed members except—and this is important— if it’s “for cause.” That means gross misconduct.

President Trump is claiming that Cook committed mortgage fraud and is therefore eligible to be fired. Cook is accused of claiming two primary residences over a two-week period. This happened before she worked at the Fed.

Cook ignoring the president. She has returned to work and said she intends to sue. Her lawyer said the president’s action is unlawful. Importantly, Cook hasn’t been charged with anything, and the actions involve her personal business dealings, and nothing about the Fed. Her term at the Fed doesn’t end until 2038.

This could get messy if the president nominates a replacement and the Senate confirms him or her. What then? I have no idea.

President Trump has already appointed two current Fed governors, both from his first term. He also got an opening recently when Adriana Kugler resigned, although that seat was due to be open soon. Then in May 2026 comes the big one when Jerome Powell’s term is up and the president can appoint a new Fed chairman. That would give Trump appointees a majority at the Fed.

The issue is that the Fed is designed to operate independent of political pressure, but it isn’t truly independent and never has been. I suspect that this battle will eventually be decided by the Supreme Court. The Fed is best left outside politics.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. Our Buy List had a nice 8.75% winner today with Heico. It’s up 40% for the year. If you want to learn more details of our Buy List, you can sign up for our premium letter here.

Posted by Eddy Elfenbein on August 26th, 2025 at 6:13 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His