CWS Market Review – December 9, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

How much is cash worth? We’ll soon learn the answer. Paramount has launched a hostile takeover bid for Warner Bros. Discovery. Netflix already announced a deal for WBD, but that was in cash and stock. Specifically, Netflix offered $27.75 per share for WBD. That’s $23.25 per share in cash and $4.50 in stock. Paramount is offering $30. All cash.

The details get a little tricky because WBD’s cable holdings aren’t in the Netflix deal. If those are spun off, that could be very lucrative while Paramount is trying to buy all of WBD. What I like is that Paramount is bringing its offer directly to WBD shareholders. Personally, I’d lean toward the Paramount offer.

The S&P 500 Nears a New High But Doesn’t Quite Make It

Through Friday, the S&P 500 rallied nine times in 10 sessions. The index got within 0.5% of a new all-time high. Then it lost its nerve and quickly backed off. The S&P 500 lost ground yesterday and today, albeit by a very modest amount.

Will the market rally through to a new high? I can’t say, but if it does then the Federal Reserve would be an ideal catalyst. The Fed began its two-day meeting today. Tomorrow afternoon, the central bank will release its policy statement, and it’s widely accepted that the Fed will cut interest rates again. This would be the third cut in as many meetings.

If the Fed cuts by 25 basis points, then it would bring the Fed’s target range for its Fed funds rate to 3.50% to 3.75%. This is the overnight lending rate that banks use between themselves. Over the last year, through September, core inflation is running at 3%. A Fed cut would lower the real interest rate, meaning adjusted for inflation, to a range of 0.50% to 0.75%. That’s low by historical standards, but there’s room to go lower.

There could be some drama at this meeting. I’m curious what the vote will be. For the first time in many years, there may be a rift among FOMC members. Jerome Powell appears to be fine with a rate cut this week, but I sense he’s not fully onboard with another rate cut next month, while some members are.

Even though the C in FOMC stands for committee, it’s rare to see divisions within the Fed. The Fed prefers to make its moves by consensus. Sometimes you’ll see minor dissents, but nothing too dramatic. By and large, the chair gets their way. A Fed chairman hasn’t been outvoted in over 40 years.

But Powell is a lame duck. That may change things. Powell will be out as Fed chair in May, and Kevin Hassett is the leading candidate to be President Trump’s pick. Powell was initially appointed by President Obama. He was then elevated to Fed chair by President Trump and reappointed by President Biden.

The FOMC meeting will conclude tomorrow, and the policy statement will be released at 2 pm ET. For the January meeting, the odds of a Fed rate cut are at just 23%. After cutting rates tomorrow, traders see the Fed taking a six-month break. With tomorrow’s decision, we’ll also get the Summary of Economic Projections, otherwise known as the dot plot. This will tell us more about the Fed’s plans for 2026 and beyond.

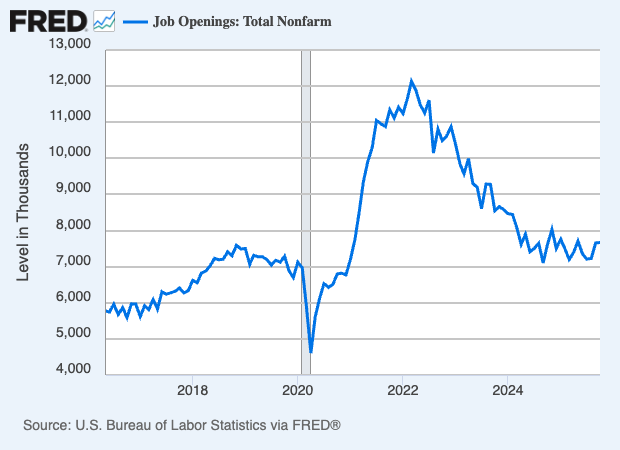

The key for investors is to watch for the health of the jobs market. Remember that more workers translates to more shoppers. The Labor Department released its jobs openings report today, (ie, the JOLTS report). The report said that the number of job openings for October rose to a five-month high.

That’s the good news. The bad news is that job openings increased a tiny bit, from 7.66 million to 7.67 million. Also, layoffs rose to 1.85 million which is the highest since early 2023. Hiring fell by 218,000.

Healthcare has been the big jobs driver all year. Outside that, the numbers haven’t been that impressive. This fits the overall pattern we’ve seen: a stagnant jobs market. The reality is that consumers and businesses are struggling to deal with higher costs.

Also, we may have to put a big asterisk on today’s numbers from the JOLTS report. The BLS said that because of the government shutdown, it had to stop using its regular methods. The next JOLTS report will be out on January 7.

The phrase that’s been making its way around economists these days is “no hire, no fire.” In other words, the unemployment rate is still quite low by historical terms, but companies aren’t willing to hire new employees.

Hiring has slowed down, especially for new college graduates. It’s as if the economy has hit a perfect equilibrium where businesses aren’t willing to shed staff, but they’re weighed down by costs and uncertainty so they’re not hiring either. I don’t expect this balance much longer. Soon, firings will be hard to ignore.

Home Deport Offers Cautious Guidance

Shares of Home Depot (HD) were weak today after the company gave disappointing guidance. I like to pay attention to what Home Depot has to say. They probably have a better understanding of consumer spending than many official government reports.

Home Depot has struggled lately. Over the last three months, the S&P 500 is up around 5% while HD is down by 15%.

For fiscal 2026, the home improvement store expects sales growth of 2.5% to 4.5%. That unnerved some traders. Wall Street had been expecting 4.5%.

Home Depot also said it expects EPS growth to be flat to +4%. For comparable sales, HD sees growth of flat to +2%. Of course, a lot of this will depend on the housing market. For the current fiscal year, HD sees EPS falling by about 6%. Home Depot isn’t alone. Toll Brothers and Hovnanian both said that demand is being held back by high mortgage rates and worries about the tariffs. So much of the broader economy is closely tied to the housing market.

On the plus side, the Russell 2000 Index of small-cap stocks hit a new high today. The Russell 2000 has lagged the market consistently for the last five years. Every prediction of a rotation to the little guys has flopped. Well, it’s happening again. The Russell 2000 has outpaced the S&P 500 for the last month. I hope this trend continues, but I won’t make any promises.

One of the more difficult aspects of investing that’s hard to convey to a new investor is just how big the big companies are. The giant blue-chip behemoths dominate the investing world, and everyone else is running behind.

Consider that if all 2,000 stocks in the Russell 2000 merged to form one super company, it still would be far from the largest company on Wall Street. The combined value is currently around $2.7 trillion. The Russell 2000 makes up for just 7% of the Russell 3000. The five largest companies in the S&P 500 make up slightly more than 25% of the index.

Financial stocks have also improved in recent weeks. Goldman Sachs (GS) and Bank of New York Mellon (BK) both hit new highs today. A wider yield spread is good for the banks. Tech has also been acting better in recent days, but it’s still lagging several sectors over the last month.

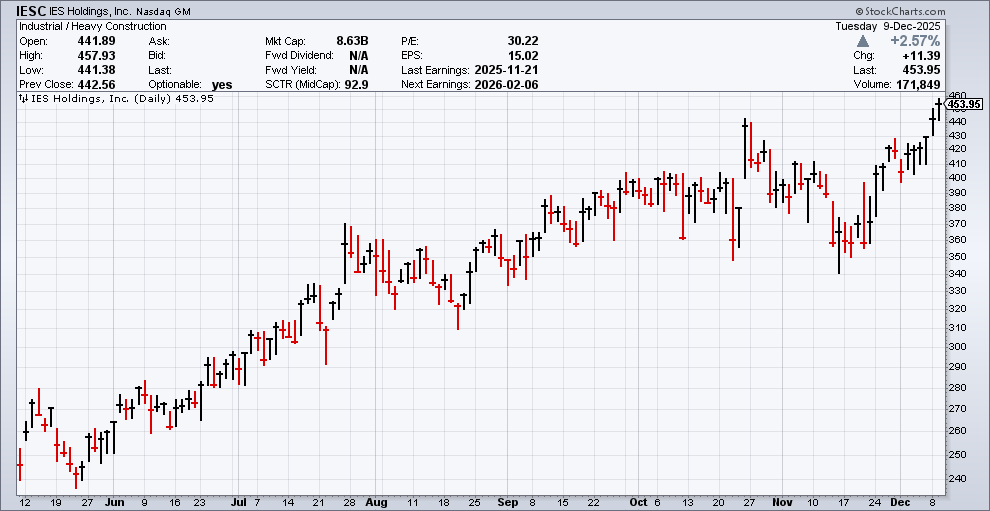

I hope you don’t mind if I brag a little about IES Holdings (IESC). I mentioned this stock to you three weeks ago, just before its earnings report. The company currently operates through four business segments: Electrical, Communications, Infrastructure and Residential. It’s been a huge winner for us this year.

On November 21, the company reported outstanding results for its fiscal Q4, and the shares rallied 8.5%. Revenue rose 16% to $898 million. Operating income was up 39% to $104.3 million, and diluted adjusted EPS was $3.77 compared with $2.61 one year ago.

I had already told you some of this story a few weeks ago, but the latest news is that the stock has rallied even more. The stock has closed higher for the last six days in a row. The stock reached another all-time high. IESC is up 27% since I first told you about it, and 125% since I first added it to our Buy List a year ago.

That’s all for now. The Federal Reserve meeting wraps up tomorrow. The policy statement will be out on Wednesday at 2 pm ET. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on December 9th, 2025 at 5:27 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His