CWS Market Review – February 24, 2026

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

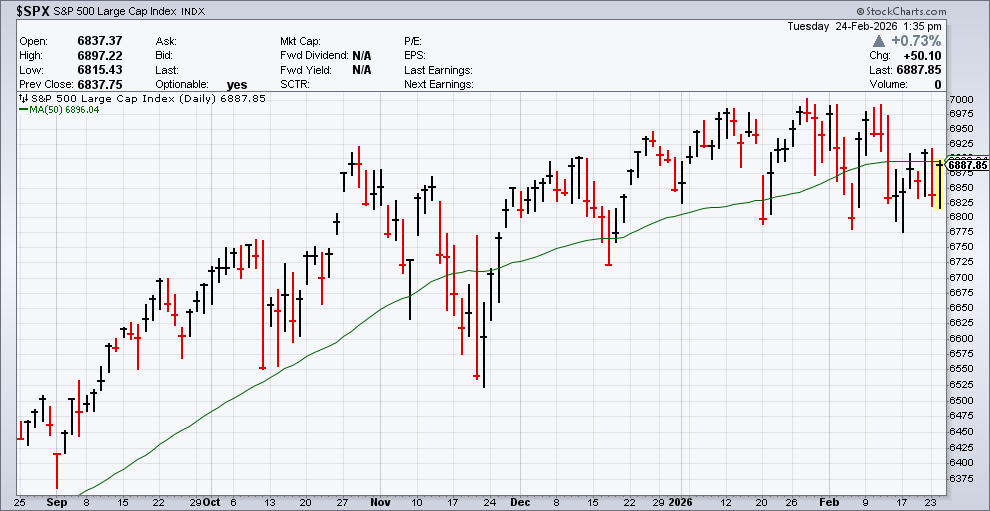

For the 44th trading day in a row, the S&P 500 closed within 1.5% of 6,900. It doesn’t seem to matter what the news is – the S&P 500 can’t get the strength to stray very far from 6,900. While on the surface, the market appears to be calm, that can be misleading. There are strong currents just below the surface.

The most important change is that since late October, defensive stocks have started to act much better, especially compared with the overall market. By defensive stocks, I mean companies whose businesses tend to prosper no matter what the rest of the economy is doing. Principally, I think of consumer staples and healthcare stocks as the best examples of defensive stocks.

When times get tough, defensive stocks hold up much better. Or, more accurately, defensive stocks tend to fall the least in bear markets. Before October, defensive stocks got absolutely clobbered by traders. Beginning in April 2025, the market soared, but our defensive friends barely budged. The gap between defensive stocks and everybody else grew enormously wide.

I knew something had to give, and it finally happened.

Since October 29, the S&P 500 Consumer Staples ETF (XLP) is up by 17.6% and the S&P 500 Healthcare ETF (XLV) is up by 10.4%. Meanwhile, the S&P 500 ETF (SPY) is up by a scant 0.3%.

As a general rule, defensive stocks will slowly lag the market for a long time; then all of a sudden, they massively outperform. Think of defensive stocks as the lifeboats of stock picking.

The time to buy defensive stocks is when the economy gets wobbly. The big question is, if defensive stocks are leading the market, does this mean that Wall Street is worried about the economy? Utilities are also defensive and they also do well when the economy is weak and rates are coming down.

The U.S. Economy Hit a Small Bump Last Quarter

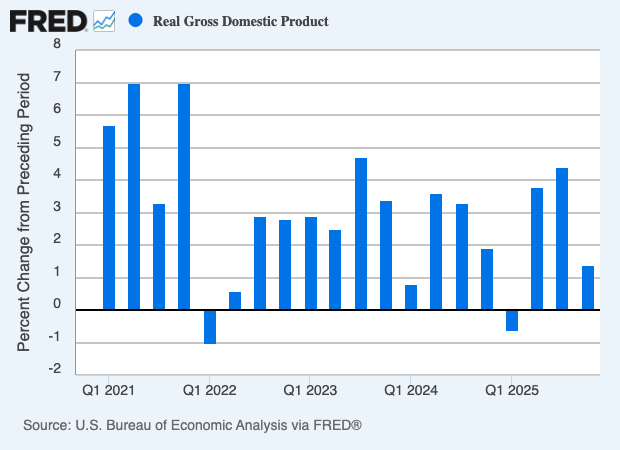

On Friday, the Commerce Department finally released its long-delayed Q4 GDP report. Bear in mind that this is dated info. Q4 began five months ago and ended two months ago.

Unfortunately, the news wasn’t very good. According to the government, the U.S. economy grew in realized annualized terms of 1.4% during Q4. That was well below economists’ estimate of 2.5%. Some folks were expecting 3% or more.

The Commerce Department said that the government shutdown shaved about 1% off growth for Q4.

Consumer spending increased at a slower pace for the period while government spending tumbled sharply in a quarter marked by the record-length shutdown. The department estimated that the shutdown subtracted about 1 percentage point from growth, though it added that the exact impacts “cannot be quantified.”

For the full year in 2025, the U.S. economy grew at a 2.2% pace, down from the 2.8% increase in 2024.

The shutdown ran for most of the first half of Q4. Except for Covid, last year the U.S. economy had the worst year for economic growth of the last nine years. I think it’s interesting that nominal GDP grew by 44% over the last five years. Of course, inflation had a lot to do with that, as did the sharp rebound from Covid.

There were some positive details within the report:

Another key Fed metric, called final sales to private domestic purchasers, posted a 2.4% increase for the quarter, half a percentage point lower than the prior quarter but still indicative of solid underlying demand in the $31.5 trillion U.S. economy.

Also, gross private domestic investment rose 3.8% after being flat in Q3. On the downside, government spending and investment slid 5.1%, slammed by a 16.6% tumble at the federal level that was only partially offset by a 2.4% increase from state and local entities.

We also got the PCE data which is the Fed’s preferred measure for inflation. During December, the PCE rose by 0.4%, and it’s up by 2.9% over the last year. That was a little higher than expected. In December, the core PCE rose by 0.2%, and it’s up by 3% over the last 12 months.

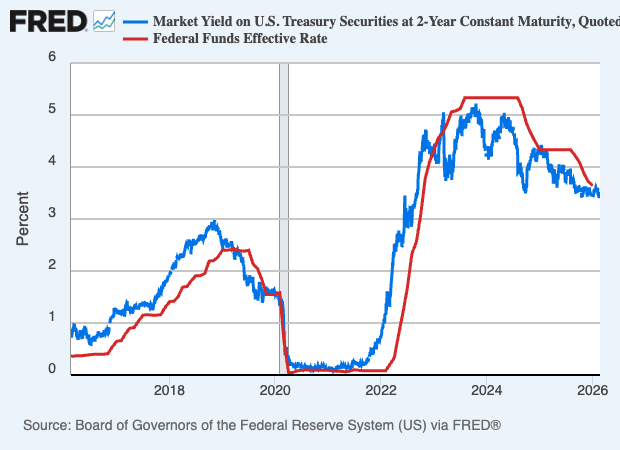

Where does this leave the Federal Reserve? Probably no change. The Fed doesn’t meet again for another three weeks and it’s very doubtful the Fed will make any changes to interest rates at its March or April meetings. There is a decent chance, although far from absolute, that the Fed will make a move in June. Of course, this would be after May when Jerome Powell’s tenure comes to an end.

If you want to see a sneak preview of what the Fed is up to, checking out the two-year Treasury is often a good predictor. If you look at the chart below, the blue line (the two-year yield) often runs just ahead of the Fed’s policy (the red line).

The Fed currently has interest rates pegged between 3.5% and 3.75%. The two-year Treasury is currently at 3.47%. This tells me that the Fed probably won’t make any big moves soon.

Stock Focus: Graco

If you’ve followed me for a long time, then you know I’m big fan of little-known stocks that have great long-term track records. I’m always amazed that investors waste so much energy trying to find the “next Nvidia” instead of the current Church & Dwight (CHD).

This week, I want to bring Graco (GGG) of Minneapolis to your attention. I can’t say that Graco is completely unknown, but it isn’t well known. Graco turns 100 years old this year.

The company describes itself:

Graco Inc. supplies technology and expertise for the management of fluids and coatings in both industrial and commercial applications. It designs, manufactures and markets systems and equipment to move, measure, control, dispense and spray fluid and powder materials. A recognized leader in its specialties, Minneapolis-based Graco serves customers around the world in the manufacturing, processing, construction, and maintenance industries.

Sexy, right? Management of fluids! Sure, I know it’s a little boring, but look at the stock. According to this chart, shares of GGG are up 70-fold over the last 40 years.

That doesn’t include dividends. If we add in dividends, then GGG is up more than 440-fold over the last 40 years. Not bad for managing fluids.

But there’s another reason why I like Graco. I love to follow the Dividend Aristocrats. These are companies that have increased their dividends every year for at least 25 years. There’s an ETF focused on the the Aristocrats (ticker symbol: NOBL).

One pet peeve I have is that too many Dividend Aristocrats give their dividends a token increase just so they can keep their dividend streaks going.

That’s where Graco comes. First, GGG can’t officially be a Dividend Aristocrat because it’s not in the S&P 500. It’s in the Mid-Cap S&P 400. What I like about Graco is that the company consistently raises its dividend by sizable amounts. It’s rare that you’ll see Graco hike its dividend by less than 7%.

From Graco’s Investor Relations page, you can see a long history of Graco’s dividends. Not many companies provide that level of detail. The current quarterly dividend is 29.5 cents per share. Over the last 20 years, Graco has increased its dividend at an average rate of 9.5% per year, and that comes on top of a healthy increase to its stock.

As much as I like Graco, the company has missed its earnings forecast several times recently. I can’t say I’m a buyer yet – I’d prefer to wait on Graco until its business improves. That’s the great thing about investing. We can wait and wait and wait until we get the patch we want.

That’s all for now. The next jobs report will be due out on March 6. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on February 24th, 2026 at 6:36 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His