CWS Market Review – March 3, 2026

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

This weekend, the U.S. military commenced Operation Epic Fury with its mission of toppling the theocratic regime in Iran.

I’m far from an expert on defense issues or geopolitics (although I am a retired PFC), so I have no valuable insights on the efficacy of the mission or its potential outcome.

Around here, our concern is with finance and how the markets are reacting. For now, markets are clearly nervous. On Monday, the U.S. stock market opened lower. At one point, the S&P 500 was down 1.2% on the day. As you’d expect, many defense and aerospace stocks held up well along with energy stocks. Several travel-related stocks were among the losers.

Let me caution you that I see absolutely no reason for investors to sell. If anything, a downturn could present us with a good buying opportunity.

Bear in mind that a lot of successful investing boils down to doing nothing when everybody else is panicking. As the great Jesse Livermore said, “It never was my thinking that made the big money for me. It always was my sitting. Got that?”

Got it.

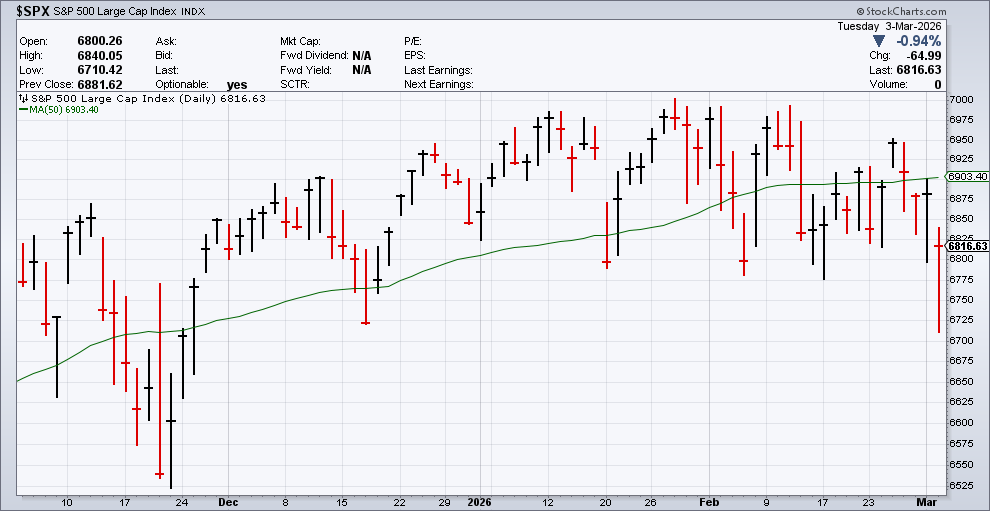

Despite the market’s weak morning on Monday, the index finished slightly positive by the closing bell. I’m sure a lot of people didn’t see that coming, and it’s a good reminder that the market loves to do what’s not expected.

Today we saw similar action but with even greater swings. At one point this morning, the S&P 500 was down over 2.1% and it briefly reached a three-month low. Like on Monday, the market reversed course and eventually closed lower by 0.9%.

Also today, there was a clear “run for safety.” By that, I mean that much of the losses were concentrated among High Beta stocks while the Low Volatility sector held up far better (still down, mind you, but not as much).

In plain English, the conservative stocks remained calm while the volatile stocks were more…well, volatile.

Check out this chart which shows the S&P 500 Low Volatility Index (in blue) compared with the S&P 500 High Beta index (in red). Since early January, Low Vol has been doing much better. This comes after last year when High Beta thrashed Low Vol.

We can also see this flock-to-safety among size categories. The big guys in the S&P 100 were down just 0.6% today, but the small-cap Russell 2000 was down close to 1.8% today.

Not surprisingly, the price of oil gapped up this week, but it wasn’t a panic move. One-fifth of the world’s oil consumption goes through the Strait of Hormuz. There could be a dramatic price spike, and that would certainly hurt consumer spending.

We saw that happen after Saddam Hussein invaded Kuwait, and that helped tip the economy into a recession. It can take a while before a disruption in the oil market appears as prices at the pump, and the odds of higher prices increase the longer the military operation lasts.

On Monday, we got the ISM manufacturing index report. This is a good report to watch because it usually comes out on the first business day of each month. Monday’s report said that the ISM Manufacturing Index for February was 52.4. That’s down a small bit from January’s number of 52.6. Wall Street had been expecting 51.8.

Any ISM number above 50 means that the factory sector of the economy is growing. This was the second month in a row of expansion, and it comes after 10 months in a row of contraction.

The Federal Reserve doesn’t meet again for another two weeks. It’s very doubtful that the Fed will make any move on interest rates at its upcoming meeting. In fact, it probably won’t make a move in the meeting again after that. The June meeting, however, could see some activity, but those odds have fallen some since the military operation started.

Remember that it’s very likely that Kevin Warsh will take over as the head of the Fed in May. Traders now see a 45% chance that the Fed will cut rates in June. That’s down from 56% a few weeks ago. The consensus on Wall Street is that we’ll have two 0.25% rate cuts before the end of the year.

On Friday, the government will release the jobs report for February. The January report said the economy created 130,000 new jobs that month. This time, economists expect to see a gain of just 50,000 jobs. A weak jobs number could spur the Fed to act, but at this point, it would have to be a dramatic miss. Now let’s look at one of my favorite little-known stocks.

Stock Focus: Allison Transmission

In our premium newsletter, we’ve recently finished all the earnings reports for Q4. (By the way, you can sign up for it here!) There’s one of our stocks in particular that I wanted to share with you, which is Allison Transmission (ALSN). In three-and-a-half months, shares of Allison are up close to 60% for us.

Allison has a market value of about $10 billion. While that may sound like a lot, it’s small potatoes on Wall Street. Only a few analysts cover the stock, which suits me just fine.

On February 23, Allison said it made $1.18 per share. That missed Wall Street’s forecast of $1.46 per share. The good news is that Allison gave reassuring guidance, and the shares rallied 4.4% the day after the report. After that, it closed higher for four straight days until finally closing lower today.

Allison specializes in making vehicle propulsion solutions, primarily fully automatic transmissions and electrified propulsion systems (including hybrid and fully electric options) for medium- and heavy-duty vehicles.

You can find their products in almost any vehicle including buses, motor homes and even the Abrams tank.

I added Allison to our 2025 Buy List, and it was a flop, but we held on and I’m glad we did. Once again, it was our sitting that did the trick.

The big news recently is that Allison completed the acquisition of Dana Incorporated’s Off-Highway Drive & Motion Systems business. This deal helps expands their footprint.

For all of 2025, Allison had sales of $3.01 billion, which matched its forecast. For the year, Allison made $7.33 per share. That’s down from $8.31 per share in 2024.

Let’s look at guidance, which is a little complicated due to the Dana deal. For all of 2026, Allison expects sales between $5.575 billion and $5.925 billion, but sales for the Allison Transmission segment are expected to range between $3.025 billion and $3.175 billion. That’s better than I had expected.

For 2026, Allison expects net income between $600 million and $750 million. That’s compared with $623 million last year. That’s not bad. It works out to net income of roughly $7.25 to $9 per share. If that’s right, then the stock is still going for a decent value. The current Enterprise Value/EBITDA is 11.67.

I also like that Allison increased its quarterly dividend by 7% to 29 cents per share. The new dividend is payable on March 20, to stockholders of record at the close of business on March 9.

In our premium issue, I rate Allison a buy up to $130 per share.

That’s all for now. The next jobs report will be due out this Friday, March 6. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on March 3rd, 2026 at 6:32 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- August 2026

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His