CWS Market Review – June 16, 2026

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

On Sunday evening, President Trump announced that Iran and the United States had reached a deal to end hostilities in the Middle East. I’m certainly no geopolitical expert so I won’t judge the deal. I am, however, a realist, and I understand there’s a long way between an announcement and real peace, especially in Middle East.

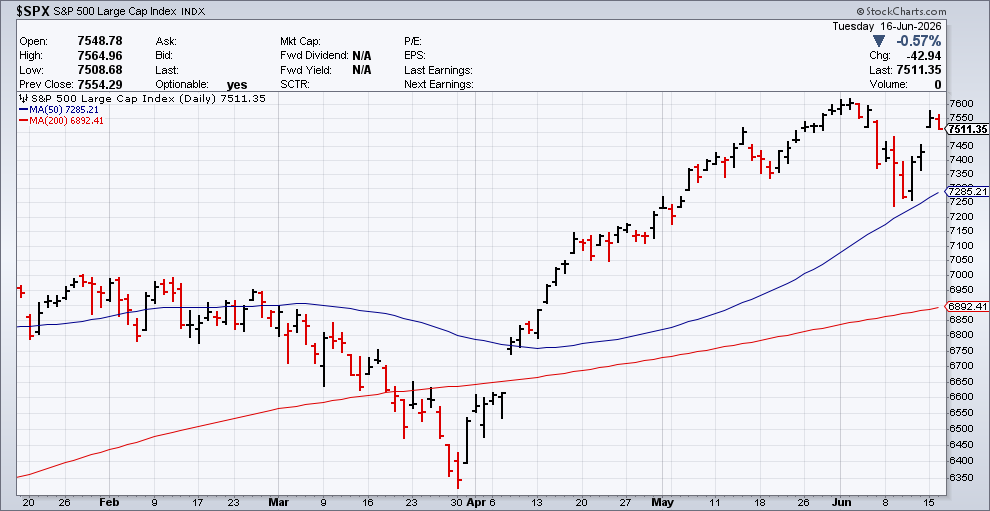

At least for now, there’s no more fighting. On Monday, the stock market celebrated the news and stocks soared. The Dow closed at an all-time high of 51,671.03.

The S&P 500 gained more than 1.6% and it’s not far from a new all-time high. The Nasdaq was up over 3% and semiconductor stocks were particularly strong. The SMH ETF was up 4.4%. At the other end, defense/aerospace and energy stocks lagged the most. Bitcoin rallied and, most importantly, oil prices dropped. The S&P 500 High Beta ETF was up more than 3.5% while the Low Vol ETF was down by 0.4%.

The stock market was a lot calmer on Tuesday. Some of the big tech names pulled back some, but nothing too alarming (outside of semiconductors). After Monday’s rally, a little bit of profit-taking is to be expected. The Dow closed at another high on Tuesday. It performed more than 120 basis points better than the S&P 500.

SpaceX (SPCX) had another good day on Tuesday. At one point, the shares broke above $225. That’s a 67% jump from last week’s IPO price of $135 per share. The valuation reached $2.85 trillion. That made it more valuable than Amazon and Microsoft.

Here’s a thought exercise. Imagine a company that had sales last year of $50,000. The company posted an annual loss of $13,200. You’re looking to buy the company, so you ask the owner, how much? He tells you it’s all yours for just $7.5 million.

You might think the owner had lost his marbles, but those numbers are pretty much in line with what SpaceX is really doing, just at a much lower scale.

My little thought exercise is to show you how the market is looking at SpaceX. Using ROE or the P/E Ratio won’t help you much with SpaceX. With an unconventional company, you’ll need an unconventional analysis. Doubting Elon Musk has not been a terribly successful strategy.

It is humbling to consider that if we harness just 1 millionth of the Sun’s power for AI, that will be much more than a million times the intelligence of all of humanity

— Elon Musk (@elonmusk) June 16, 2026

The retail sales report is out tomorrow. The report for May showed the eighth consecutive monthly increase in a row, but the big news tomorrow will be the Federal Reserve meeting.

It’s highly doubtful that the Fed will make any changes to interest rates. However, what could be newsworthy would be any more dissenting votes at the FOMC. This will also be the Fed’s first meeting under the leadership of Kevin Warsh.

At the Fed’s last meeting in April, there were four dissenting votes. That was the most in 34 years. One vote wanted to lower rates immediately while three other votes did “not support inclusion of an easing bias in the statement at this time.” I’ll be curious to see how Jerome Powell votes.

What to Expect from the Q2 Earnings Season

We’re less than a month away from the start of the second-quarter earnings season. Of course, we don’t have the numbers just yet, but it’s looking like it will be a very good season. Wall Street currently expects year over year earnings to hit 21.9%. If that’s correct, then it will mark the second quarter in a row in which earnings growth topped 20%.

For Q2, the estimated (year-over-year) earnings growth rate for the S&P 500 is 21.9%. That’s a big revision. At the start of Q2, Wall Street had been expecting growth of 18.7%. If 21.9% is the actual growth rate for the quarter, it will mark the second-straight quarter of earnings growth above 20% for the index.

For Q2, 47 S&P 500 companies have issued negative EPS guidance, and 62 S&P 500 companies have issued positive guidance. The forward P/E ratio for the S&P 500 currently is 20.1. This P/E ratio is above both the 5-year and 10-year averages.

Since the start of Q2, analysts have increased their estimates for Q2 earnings from $78.85 to $81.01 per share. This is unusual. Typically, analysts pare back their estimates as earnings season gets close. It’s no secret that companies try to dampen expectations so that when earnings day finally comes, they can announce “better than expected” news. At bottom, Wall Street is a game of expecting expectations.

Researchers at FactSet found that the term “inflation” was used on 220 earnings calls. That’s up 11% over Q4. Overall, the term “inflation” was cited on 220 earnings calls conducted by S&P 500 companies during this period. It’s also the third quarter in a row in which inflation mentions have increased.

FactSet also noticed something interesting. On earnings calls, companies have been mentioning AI at the fastest pace ever. From March 15 through June 11, the term “AI” was cited on 337 earnings calls. That’s far above the five-year average of 164. The previous was 334, which occurred in Q4.

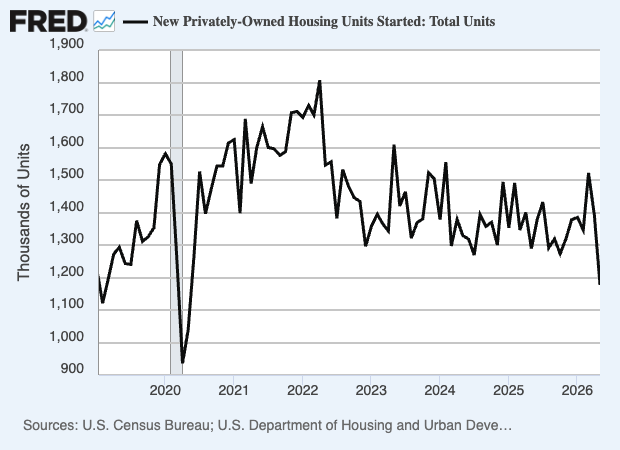

Earlier today, we got the report on housing starts, and it was ugly. The report said that housing starts last month fell by 15.4% to an annualized rate of 1.18 million. That’s the lowest since April 2020. This means we’re back to Covid levels. The report said that single family homes fell by 1.9% and multifamily starts dropped by 40.2%.

What appears to be happening is that homebuilders are trying to work off supply before they ramp up new production. A lot of young people have been priced out of the market, especially with higher interest rates. If potential buyers are waiting for mortgage rates to go lower, I don’t think they’re going to get it anytime soon.

Last month, building permits dropped by 0.7% to an annualized rate of 1.41 million. Last year, President Trump criticized home builders for sitting on empty lots in an attempt to boost home prices.

Stock Focus: Gorman-Rupp (GRC)

Shares of Gorman Rupp (GRC) hit another new high today. The stock is another example of a little-known company that’s done very well over the years.

First, though, what do they do? The company describes itself as “a leading designer, manufacturer and international marketer of pumps and pump systems for use in diverse water, wastewater, construction, dewatering, industrial, petroleum, original equipment, agriculture, fire suppression, heating, ventilating and air conditioning (HVAC), military and other liquid-handling applications.”

Since 1992, GRC is up over 4,000% including dividends. It’s nearly doubled over the last year. Despite this success, the stock is barely followed on Wall Street. GRC has a market value of more than $2.2 billion yet it’s only followed by three Wall Street analysts.

In April, GRC reported Q1 earnings of 68 cents per share. That beat estimates (if you consider so few analysts to be a consensus) of 53 cents per share. Net sales rose by 7.7% to $176.6 million.

Scott King, the president and CEO, noted that last quarter, GRC had strong operating cash flow and reduced its debt.

Four years ago, GRC bought Fill-Rite from Tuthill Corporation for $525 million. I’m always a little skeptical of big acquisitions. For a company of GRC’s size, this was a very big deal. I’m pleased to see that it’s been well integrated well. Also, the financing debt has been paid down. Interest expense dropped substantially from 2024 to 2025.

Wall Street expects GRC to earn $2.63 per share this year, and $2.99 per share in 2027. If that’s right, it would mean that GRC has tripled its earnings in five years.

The company has increased its dividend for 53 years in a row. That’s one of the longest for any publicly traded company.

If you’re looking for a conservative addition to your portfolio, Gorman-Rupp is a good choice. GRC isn’t a bargain, but it’s poised for long-term growth.

That’s all for now. Remember that the stock market will be closed on Friday in honor of Juneteenth. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on June 16th, 2026 at 7:10 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- August 2026

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His