CWS Market Review – June 30, 2026

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

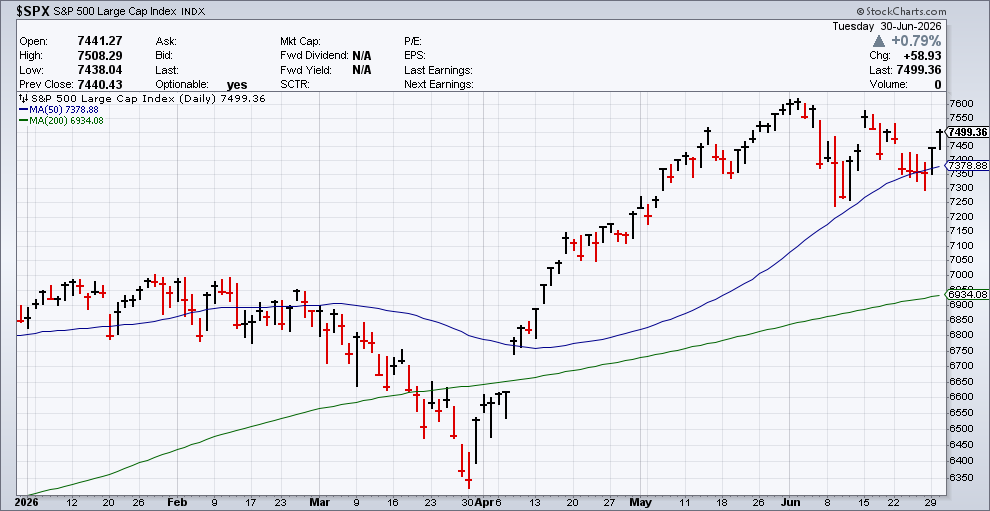

The first half of 2026 is officially on the books! So far, this has been a good year for Wall Street and the S&P 500. Even after a few dips recently, the index is up more than 9% on the year. The Dow just had its best first half in five years.

Here’s a breakdown of some YTD performance figures:

S&P 500 +9.55%

Dow Jones +8.85%

Russell 2000 +21.86

Nasdaq +12.79%

Nasdaq 100 +19.91%

Gold -7.03

Silver -16.18%

Oil 22.01%

Bitcoin -32.95%

The stock market could have more room to run. FactSet sees the S&P 500 rallying by 18.9% over the coming 12 months. Their target for the S&P 500 is 8,918.27. Personally, I admire that level of precision. They see all 11 sectors rising by double digits.

Frankly, the stock market had a little rougher time in June. At one point, the S&P 500 fell for five days in a row, and seven out of eight, but the losing streak was snapped on Monday, and the Nasdaq powered up again for a gain on Tuesday. The S&P 500 is back above its 50-day moving average.

What’s truly striking is that the Mag 7 has had a rough year so far. The group has lost a combined $2.3 trillion. All seven members are down for the year. In fact, all are down more than 10%. Tesla and Microsoft are both off more than 30% this year. Outside of the big boys, tech mostly did well during Q2. Micron is close to a double for 2026.

The story here is that Wall Street has gradually changed its outlook. It used to be focused on the level of cash flow from the Mag 7, especially free cash flow. Lately, it’s been more focused on the balance sheets as more of these companies are going to the bond market to raise cash.

What concerns me is that these companies are using these new funds to buy up companies at a frenetic pace. But are they buying companies because they complement their businesses? Or do they believe that if they don’t buy it now, someone else will soon?

How about small-cap stocks? The little guys are off to their best start in 35 years. The Russell 2000 is up more than 21% this year. Even there, AI is still part of the story. CNBC noted that chip-related companies make up 16 of the Russell 50 best performing stocks this year.

At the start of this year, Wall Street had been expecting earnings growth from the Russell 2000 of 23%. Now the forecast is up to 38%. Bank of America says that for every 0.25% hike from the Fed, that will knock 2% off this year’s earnings growth for the Russell.

If all 2,000 stocks in the Russell were merged and constituted in one stock, its market value would be in the low $3 trillions. That’s roughly in line with some of the Mag 7 names. (Of course, if all 2,000 stocks were bought out, the prices would radically change, but I meant this as a thought exercise.)

The hostilities in the Middle East continue to dominate the headline. There has been a softening in the oil market. For June, the price of oil is down about 20%. That’s good news on the inflation front, and it’s also a boost for consumer spending. Less money spent at the pump means more money spent elsewhere.

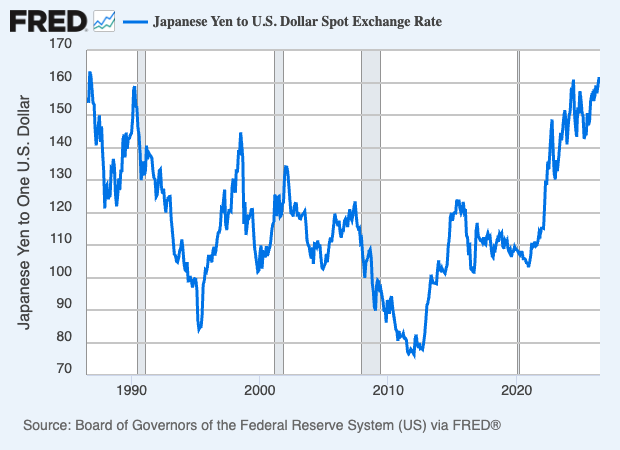

In the currency market, the Japanese yen traded at 162 to the dollar. That’s the weakest against the dollar in 40 years. That’s great for tourists, but it’s troubling to the government. In fact, the government will probably step in and start buying yen to help the currency.

Japan is starting to feel the effect of inflation. That’s something the country hasn’t had to deal with in decades. In fact, Japan has mostly dealt with falling prices.

There’s a long, sad history of finance ministers from every corner of the globe who have wasted tons of money to try prop up currencies that dearly want to go down. Reality has an odd habit of prevailing in these battles.

The yen has also been hurt by a surging dollar. That, in turn, has been aided by an increasingly hawkish tone from the Fed. There’s a decent chance we’ll get two Fed rate hikes during the second half of this year.

Frankly, there’s not a lot going on right now on Wall Street. Most of the fat cats are relaxing at their vacation homes in the Hamptons or on Martha’s Vineyard.

Earnings season isn’t far away. The unofficial kickoff for Q2 earnings season will be on Tuesday, July 14. (That’s Bastille Day. If you miss earnings, off with your head!) That’s when several of the big banks like JPMorgan Chase (JPM) and Goldman Sachs (GS) are due to report earnings. This will probably be another good earnings season, but I want to hear more guidance for the rest of this year.

This week is jobs week, but it’s a holiday-shortened week as well. We’ll get the ADP report on private payrolls tomorrow. Then on Thursday, we’ll get the June jobs report. Along with nonfarm payrolls, we’ll get the numbers for the unemployment rates and average hourly earnings.

Earnings Preview for FactSet

FactSet (FDS) is our lone Buy List earnings report between now and the start of Q2 earnings season. The fiscal Q3 results are due out tomorrow morning.

The shares have had an impressive recovery from February to early June. At one point, FDS gained 44% in a little over three months.

FactSet is a member of that group of stocks that’s assumed to be done in by AI, yet it continues to be very profitable. Three months ago, it happened again. Fact Set reported very good earnings, raised guidance and the stock rallied 6% the next day.

Let’s dig into the details. For its fiscal Q2, FactSet made $4.46 per share. That was eight cents better than Wall Street’s consensus, and it was up 4.2% over last year’s Q2. FactSet’s quarterly revenue rose 7.1% to $611 million.

The big stat for FactSet is Annual Subscription Value, or ASV. This is an important measure of forward-looking annualized revenue. For Q2, the company’s organic ASV was up 6.7% to $2.449 billion.

FactSet’s net cash from operations rose 21.7% to $211.7 million, and its free-cash flow was up 23.6% to $185.7 million. One weak spot is that its operating margin fell by 230 basis points to 35.0%.

For 2026, FactSet expects organic ASV growth of 5.4% to 6.7%. The company sees annual revenues ranging between $2.45 and $2.47 billion. For earnings, FactSet expects to be between $17.25 and $17.75 per share. That’s up from its previous guidance of $16.90 to $17.60 per share.

At the end of Q2, FactSet’s client count stood at 9,101, and its user count reached 241,352. Annual ASV retention was greater than 95%. When expressed as a percentage of clients, annual retention was 91%. Employee headcount was 1.9% to 12,840.

In May, the company increased its quarterly dividend from $1.10 to $1.16 per share. This is the 27th year in a row that FactSet has increased its dividend.

Three months ago, FactSet increased its growth forecast for organic ASV and annual revenue. The company expects operating margin of 34% to 35%. As I mentioned before, FactSet increased its earnings range for this fiscal year from $16.90 to $17.60, to $17.25 to $17.75 per share. For tomorrow, Wall Street expects FactSet to report Q3 earnings of $4.45 per share. Look for an earnings beat.

That’s all for now. The stock market will be closed on Friday. The jobs report will be on Thursday morning. Have a happy and safe Fourth of July weekend. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on June 30th, 2026 at 6:11 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His