CWS Market Review – July 14, 2026

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Inflation Has Its Biggest Drop in Six Years

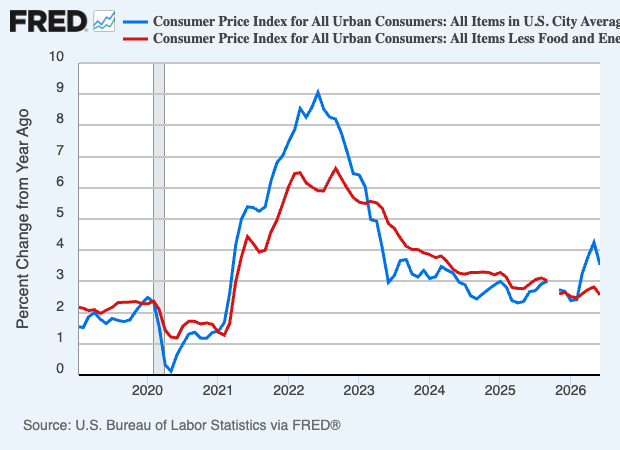

This morning, the Bureau of Labor Statistics reported that inflation fell by 0.4% last month. I knew it was going to be down, but I was surprised that it was down that much. That’s the biggest drop in over six years. Wall Street had been expecting a drop but only of 0.2%. Over the last year, inflation is running at 3.5%.

The long-term statistics say that stock prices love low and stable prices and hate inflation. In fact, the only thing stocks hate more than inflation is deflation.

Of course, the big drop was due to the decline in energy prices. This is precisely why we look at core inflation which excludes food and energy prices. Food and energy prices can easily get knocked by temporary shortages. For June, core inflation was unchanged while Wall Street had been expecting an increase of 0.2%. Over the last year, core inflation is running at 2.6%.

Here’s a look at the 12-month rolling inflation rate (blue) along with the core rate (red):

It wasn’t just energy that held down inflation last month, but housing costs also played a role. Here are some details from CNBC:

The energy index slumped 5.7% in June, its biggest monthly drop since April 2020, though it still surged 15.7% on an annual basis, pushed by a 26.7% gain for gasoline. However, gasoline and fuel oil both saw decreases of more than 9% in June.

In addition, services costs, which are closely watched by Federal Reserve policymakers for longer-run inflation trends, moderated significantly. Services excluding energy costs were flat, with shelter rising just 0.1% and transportation services posting a 0.3% decline.

Food prices rose 0.2%, while new vehicles were flat and used cars and trucks saw a 0.2% decline. Apparel prices, which are sensitive to both energy and tariff inputs, fell 0.6%.

Where does this leave the Fed? Probably not much of a change. Futures traders still expect a rate hike in September, but the odds dropped a little in today’s trading. Yesterday, the odds of a September hike were at 75%. Now it’s closer to 60%.

Thanks to some hopeful signs for peace in the Middle East, oil prices fell last month. In June, the price for West Texas Crude got as high as $97 per barrel. In July, it’s been as low as $67 per barrel.

This morning, Federal Reserve Chairman Kevin Warsh gave his regular semi-annual testimony before members of Congress. On Tuesday, he went before the House Financial Services Committee. On Wednesday, he’ll go before the Senate Banking Committee.

Warsh is new on the job. The problem is that financial markets love to over analyze any minor clue in the Fed Chairman’s remarks.

In today’s testimony, he sounded very hawkish on inflation. Warsh said that inflation “has been a tax on the American people and businesses. We plan on getting rid of that tax.” That’s nice to hear, but Fed Chairmen have long been known for tough talk and wimpy policies.

Warsh created five task forces to examine how the Fed conducts business. The panels will look at Communications Strategy, Balance Sheet, Economic Data & Alternative Data, Productivity & Jobs and Inflation Framework. Twelve-month inflation has exceeded the Fed’s target for the last 64 months in a row. There’s certainly room for improvement.

IBM Has Worst Day Ever

Today was the unofficial kickoff for the Q2 earnings season. Several of the big banks reported today.

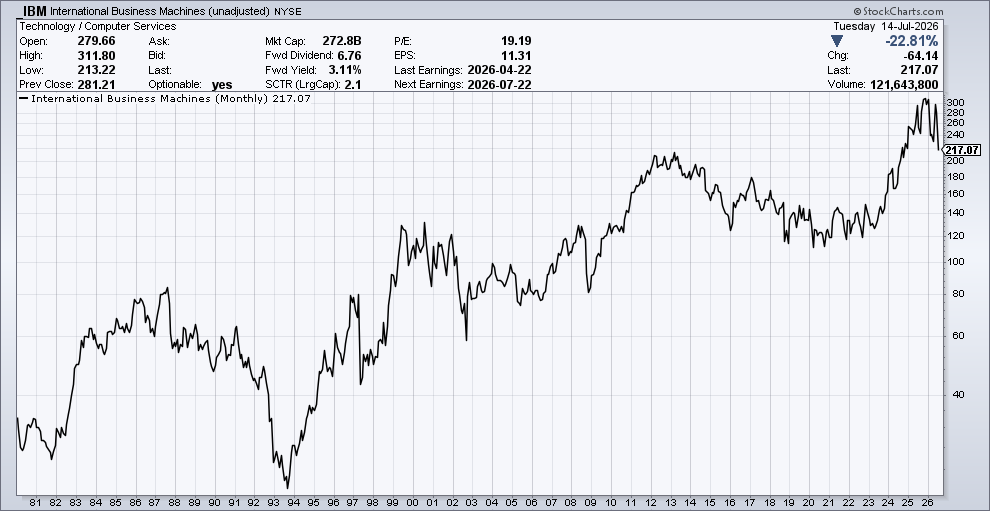

Before I get to the big banks, the big shocker today was IBM (IBM). The stock got pounded for a 25.2% loss. This looks to be IBM’s worst day in its 115-year history, even surpassing Black Monday in 1987.

Here’s a chart of IBM going back to January 1980 (without dividends):

Except for the late-90s, that’s not a very impressive chart.

Big Blue won’t report its earnings until next week, but it said its profits will be below expectations. This is exactly what I’ve talked about before. Profits are up for Corporate America, but expectations are even higher. Nowadays, if you miss, even by just a bit, the traders will be merciless.

According to the WSJ, “IBM said the performance of its software and infrastructure business fell short of expectations in the second quarter, and the company didn’t react quickly enough to the changing market conditions.” The drop erased $68 billion in market value. CEO Arvind Krishna said, “this quarter we faltered.”

The other fallout is that IBM is a Dow component. It’s been in the index continuously since 1979. This is where things get interesting because the Dow is a price-weighted index. This means the Dow is computed by adding up the prices of all 30 stocks and multiplying by six (or 5.9436, to be more precise). That means that all by itself, IBM cost the Dow more than 430 points today. Not including dividends, the stock is up 11% over the last 14 years.

Now let’s look at some of the bank earnings from today. Citigroup (C) appeared to have good numbers. For Q2, Citi earned $3.15 per share which beat estimates of $2.71 per share. In fact, Citi beat all 20 of the estimates Wall Street had for today.

Citigroup has received a lot of attention recently as CEO Jane Fraser has worked to turn around the bank. It seems that her plans are working.

The bank also announced a $30 billion share buyback, plus a 12% dividend increase. Still, the shares fell more than 4% today.

Goldman Sachs (GS) had a very strong quarter. The bank had equities revenue of $7.42 billion. That’s a blowout number. It’s up 72% over last year. Goldman had investment-banking fees of $3.4 billion, and $4.59 billion in rates trading.

The stock closed higher by 9% today. Like IBM, Goldman is also a member of the Dow. With a share price at $1,140, it has the greatest weight of any member of the index. Goldman is currently worth more than 6,800 points in the Dow.

JPMorgan (JPM), yet another Dow stock, reported its highest profit ever. Q2 equities rose 86% to $6.03 billion. Net income was $7.70 per share. Wall Steet had been expecting $5.64 per share. JPM gained 2.5% today.

Bank of America (BAC) saw its profits rise 27% last quarter to $9.1 billion. Earnings per share rose 34% to $1.21 per share. Revenue grew 15% year-over-year to $31.6 billion.

Tomorrow, we’ll get earnings from companies such as BlackRock (BLK), Morgan Stanley (MS) and Bank of New York Mellon (BNY).

On Thursday, Abbott Labs (ABT) will be our first Buy List stock to report for this season. The stock has fallen the last few days but I’m expecting good results. For Q2, Abbott sees earnings coming in between $1.25 and $1.31 per share. For the whole year, Abbott sees earnings between $5.38 and $5.58 per share. I hope to see higher guidance.

That’s all for now. Fed Chairman Kevin Warsh will testify on Wednesday before the Senate Banking Committee. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on July 14th, 2026 at 5:58 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His