Archive for 2008

-

An Investing Lesson

Eddy Elfenbein, April 30th, 2008 at 11:56 amConsider these recent headlines.

So Warren Buffett not only thinks we’re in a recession, but he thinks it will be worse than feared. So what does he do? He buys.

To quote George Bailey:Can’t you understand what’s happening here? Don’t you see what’s happening? Potter isn’t selling. Potter’s buying! And why? Because we’re panicky and he’s not. That’s why. He’s picking up some bargains.

-

What If Bernanke Is Winning?

Eddy Elfenbein, April 30th, 2008 at 10:57 amHere’s a scary thought. What if Ben Bernanke has been doing the right thing? Not only did GDP come in positive for the month, but core inflation has been running between 2% and 2.5%. Most shocking of all has been the decline in gold. The June contract dropped below $870 an ounce today. That’s a major fall from six weeks ago.

-

The Economy Grew But Just Barely

Eddy Elfenbein, April 30th, 2008 at 8:41 amFirst-quarter GDP came in at +0.6%. That’s not a lot, but it is positive. Naturally, this number will be subject to several revisions and re-revisions of previous revisions.

Even though we haven’t reached an official recession yet, which is usually defined as back-to-back quarters of negative GDP, the economy has had below-trend growth for six of the last eight quarters. Below is a table showing economic growth for the trailing eight quarters (not annualized but adjusted for inflation). You can really see how much economic growth has down-shifted.

On a bizarre note, today’s GDP report showed that the economy grew by almost exactly the same rate in the first quarter of 2008 as in the first quarter in 2007. One year ago, the economy grew by 0.6009%. For this year’s first quarter, the number was 0.5966%. -

Even Buffett Isn’t Perfect

Eddy Elfenbein, April 30th, 2008 at 8:23 amAuthor Vahan Janjigian claims that even Warren Buffett isn’t perfect in his new book, Even Buffett Isn’t Perfect. David Kansas writes:

And there have been memorable stumbles over the years: A Berkshire Hathaway investment in the retailer Pier I, in 2004, unhappily preceded a big drop in Pier I’s stock; more famously, a stake in Salomon Bros. in the late 1980s and early 1990s, though it eventually made money, caused more headaches than it was worth. (Salomon eventually became part of what is now Citigroup.)

What’s remarkable about Mr. Buffett is that he has made so few mistakes while building Berkshire Hathaway into a stock-market titan. He strongly prefers that the investments of Berkshire Hathaway be referred to as such rather than credited to himself alone. Still, in the popular imagination it would be hard to slide a piece of paper between Mr. Buffett and his company.Buffett also owned US Air which was a major blunder. To his credit, Buffett has been very candid about his mistakes. This is from his 1996 Chairman’s Letter:

When Richard Branson, the wealthy owner of Virgin Atlantic Airways,

was asked how to become a millionaire, he had a quick answer: “There’s

really nothing to it. Start as a billionaire and then buy an airline.”

Unwilling to accept Branson’s proposition on faith, your Chairman decided

in 1989 to test it by investing $358 million in a 9.25% preferred stock of

USAir.

I liked and admired Ed Colodny, the company’s then-CEO, and I still do. But my analysis of USAir’s business was both superficial and wrong. I was so beguiled by the company’s long history of profitable operations, and by the protection that ownership of a senior security seemingly offered me, that I overlooked the crucial point: USAir’s revenues would increasingly feel the effects of an unregulated, fiercely-competitive market whereas its cost structure was a holdover from the days when regulation protected profits. These costs, if left unchecked, portended disaster, however reassuring the airline’s past record might be. (If history supplied all of the answers, the Forbes 400 would consist of librarians.) -

RIP: Albert Hofmann

Eddy Elfenbein, April 30th, 2008 at 7:07 amAlbert Hofmann, the inventor of LSD, has died at the age of 102. The story of the development of drugs, legal and illegal, is one of the more fascinating business stories of the 20th Century. It’s fashionable today to say that we live in the Digital Age. Sometimes I think we live in the Drug Age. (For example, check out the amazing story of Aspirin.)

Hofmann developed LSD in 1938 when he was working for Sandoz (now Novartis, but I doubt you’ll find that fact in their annual reports) and took the first hit in 1943. For a while, the drug was seen an aid for the psychiatry profession, hence Timothy Leary and the Army tests. In fact, LSD was perfectly legal up until 1966.

Of all the major stock sectors, the major pharmaceutical stocks have probably had the best long-term performance of any sector. In recent years, stocks like Merck and Pfizer and others have stumbled, but for decade after decade, these types of stocks were world beaters. New leaders will emerge, but this sector has been a great triumph of free enterprise, and I think it will continue to be so.

-

Crossing Wall Street: It’s Like Reading Tomorrow’s Newspaper Today

Eddy Elfenbein, April 29th, 2008 at 7:27 pmAfter the bell, SPSS (SPSS) reported earnings of 51 cents a share. This caught everyone off-guard since Wall Street’s consensus was for 44 cents a share. The stock is up nicely after-hours.

Actually, there was one outlet that wasn’t surprised. This guy’s analysis is brilliant. Almost godlike.

I could go on, but Mensa may call. -

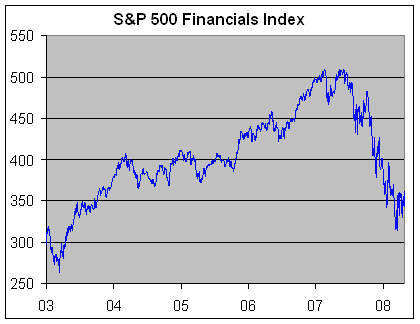

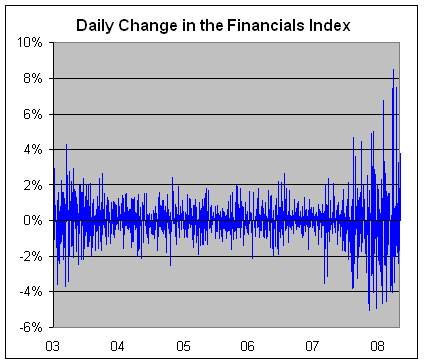

The Decline and Fall of Financials

Eddy Elfenbein, April 29th, 2008 at 2:55 pmLook at the stunning decline in the S&P 500 Financial Index (^SPSY).

Notice how the line went from being somewhat smooth to being extremely jagged. Barry Ritholtz notes that there have been an amazing 12 rallies of 5% or more in the Financials Index since it topped out.

Here’s a look at the daily changes. Sometimes a chart says it all:

-

One and Done

Eddy Elfenbein, April 29th, 2008 at 1:43 pmThe Fed meets again today and tomorrow. According to the futures market, there’s about a 70% chance that the Fed will cut by 25 basis points tomorrow. That would bring rates down to 2%. There’s close to a 30% chance that the Fed won’t make any cut.

Assuming the Fed cuts by 25 points, the futures market believes there’s about a 55% chance of no further action at their June meeting. There’s about a 10% chance of another 25-point cut, and there’s close to a 30% chance of no cut at either meeting.

Interestingly, if the Fed stops at 2%, this will mark the third straight easing cycle where the Fed stopped at a round number. In the early-90s, they went down to 3%, and a few years ago, they went down to 1%. -

Volcker at the Fed

Eddy Elfenbein, April 29th, 2008 at 12:47 pmMegan McArdle has a smart post on her choice for the most underrated and overrated presidents of the 20th century. She says that Jimmy Carter’s economic policies are underrated and she cites his appointment of Paul Volcker to head the Federal Reserve as an example.

I agree that Volcker was a good choice and Carter deserves credit for it, however I’m not willing to give him much credit. According to William Grieder’s wonderful book, Secrets of the Temple, Jimmy Carter was almost comically illiterate on monetary policy. Plus, the Volcker selection hardly signaled any policy shift from the Carter administration, and if Carter had realized what he was doing, he probably would have had second thoughts.

Carter’s selection of Bill Miller for Fed Chairman was disastrous, and it made Volcker’s job that much harder. When it came to replace Miller, Volcker was actually Carter’s second choice. His first choice was Tom Clausen, who was the president of Bank of America (he later became head of the World Bank). Also, Volcker was already an important voice on the Fed. He was president of the Federal Reserve Bank of New York, which in the Federal Reserve system, is first among equals. The president of the New York Fed also has a permanent seat on the interest-rate-setting Federal Open Market Committee. The other bank presidents have to rotate. In fact, at the time of his appointment, Volcker was serving as vice-chair of the FOMC.

So Carter’s choice was a natural elevation more than taking a major gamble, or boldly separating himself from a previous path. Still, he did make the right choice and that’s worthy of praise. The point that I find interesting is how often we give credit to people for doing something that really had no intention of doing. Instead, circumstances came to them, and they made the best of it. Perhaps, that’s a good definition of leadership. -

Investors Are Basically Crazy

Eddy Elfenbein, April 29th, 2008 at 11:06 amI’m a bit skeptical of this, but I’ll pass this along from the Genetic Engineering & Biotechnology News website (I know, like you don’t have it under your favs):

‘Emotional inflation’ leads to stock market meltdown

Investors get carried away with excitement and wishful phantasies as the stock market soars, suppressing negative emotions which would otherwise warn them of the high risk of what they are doing, according to a new study led by UCL (University College London). Economic models fail to factor in the emotions and unconscious mental life that drive human behaviour in conditions where the future is uncertain says the study, which argues that banks and financial institutions should be as wary of emotional inflation as they are fiscal inflation.

The paper, published in this months issue of the International Journal of Psychoanalysis, explores how unconscious mental life should be integrated into economic decision-making models, where emotions and phantasies unconscious desires, drives and motives are among the driving forces behind market bubbles and bursts.

Visiting Professor David Tuckett, UCL Psychoanalysis Unit, says: Feelings and unconscious phantasies are important; it is not simply a question of being rational when trading. The market is dominated by rational and intelligent professionals, but the most attractive investments involve guesses about an uncertain future and uncertainty creates feelings. When there are exciting new investments whose outcome is unsure, the most professional investors can get caught up in the everybody else is doing it, so should I wave which leads first to underestimating, and then after panic and the burst of a bubble, to overestimating the risks of an investment.

Market investors relationships to their assets and shares are akin to love-hate relationships with our partners. Just as in a relationship where the future is unexpected, as the market fluctuates you have to be prepared to suffer uncertainty and anxiety and go through good times and bad times with your shares. You can adopt one of two frames of mind. In one, the depressive, individuals can be aware of their love and hate and gradually learn to trust and bear anxiety. In the other, the paranoid schizoid, the anxiety is not tolerated and has to be detached, so the object of love is idealised while its potential for disappointment is split off and made unconscious.

What happens in a bubble is that investors detach themselves from anxiety and lose touch with being cautious. More or less rationalised wishful thinking then allows them to take on much more risk than they actually realise, something about which they feel ashamed and persecuted, but rarely genuinely guilty, when a bubble bursts. Again, like falling in idealised love, at first you notice only the best qualities of your beloved, but when everything becomes real you become deflated and it is the flaws and problems that persecute you and which you blame.

Lack of understanding of the vital role of emotion in decision-making, and the typical practices of financial institutions, make it difficult to contain emotional inflation and excessive risk-taking, particularly if it is innovative. Those who join a new and growing venture are rewarded and those who stay out are punished. Institutions and individuals dont want to miss out and regulators are wary of stifling innovation. If other investors are doing it, clients might say why arent you doing it too, because theyre making more money than we are.You can find the full paper here.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His