Archive for 2009

-

Thain Doing His Part

Eddy Elfenbein, January 27th, 2009 at 10:13 amAccording to the New York Post, while dining recently, John Thain, “loudly told the waiter, for all to hear, ‘under the circumstances with this tough economy, I think I’ll have tap water.'”

Going by his recent track record, I’m guessing he offered to pay $3.7 billion for the tap water. -

Dividends Being Cut at Fastest Pace in 50 Years

Eddy Elfenbein, January 27th, 2009 at 9:54 amBank of America (BAC) recently cut its annual dividend from $1.28 a share to four cents. (Why even keep it?) Of course, now that you’re on Uncle Sam’s bailout list, it’s hard to justify send profit checks to your owners. Dividends had made a big comeback in recent years, now it looks like the trend is in the other direction:

Already this year, seven companies in the Standard & Poor’s 500 index have decreased their dividends, removing some $12 billion from shareholders’ pockets in the coming months. On Monday, Pfizer became the latest blue-chip company to do so.

These cuts serve up another hit to shareholders who have already been battered by the steep declines in the stock market. That is especially true of retirees, who tend to be attracted to so-called “widows and orphans” stocks that provide them with a steady cash flow.

If the trend continues, this will be the worst year for dividend cuts since 1958, when annual payments fell by 8.4 percent, according to new research from S&P.

“It is easy to say this is going to be the worst in 50 years, but the bigger question is whether it is going to be much worse than that,” said Howard Silverblatt, senior index analyst at S&P. -

Geithner Is Confirmed

Eddy Elfenbein, January 26th, 2009 at 6:24 pmThe Senate votes to confirm Geithner 60-34.

-

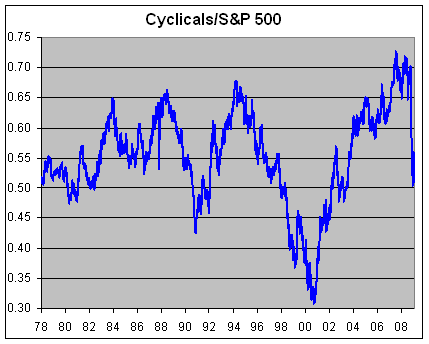

Cyclical Stocks Still Have a Long Way to Fall

Eddy Elfenbein, January 26th, 2009 at 3:59 pmHere’s a look at the Morgan Stanley Cyclical Index (^CYC) divided by the S&P 500 (^SPX). For such a simple metric, I think is an often-revealing look at the market’s mentality. What it tells us is how well economically sensitive stocks are performing compared with the overall market.

About two years ago, I started warnings investors that cyclical stocks were heading towards a top. On July 19, 2007, the CYC reached its peak ratio against the S&P 500 at 0.7273. Since then, all most all kinds of stocks have down poorly but cyclical stocks have down much worse. Through Friday, the S&P 500 is down 46.4% from July 19, 2007, but the CYC is down 62.3%.

The other reason why I like to follow this ratio is that it tends to move in multi-year waves, as one would expect from looking at economic cycles. Until the ratio starts to show some improvement, I’m not going to be terribly optimistic for the broader economy. The ratio is currently around 0.51 which is still well above typical cycle lows.

-

Blame China

Eddy Elfenbein, January 26th, 2009 at 12:56 pmSebastian Mallaby claims China’s currency policy was a major cause of the housing bubble:

Geithner is correct that China manipulates its currency. What’s more, this manipulation is arguably the most important cause of the financial crisis. Starting around the middle of this decade, China’s cheap currency led it to run a massive trade surplus. The earnings from that surplus poured into the United States. The result was the mortgage bubble.

China’s leaders protest that they are being unfairly scapegoated. Yet while there are rival accounts of the origins of the crisis, neither has the explanatory force of the blame-China narrative. -

A Capital-less Financial System

Eddy Elfenbein, January 26th, 2009 at 12:19 pmHere’s a sample of a fascinating article from Ricardo Caballero at the Financial Times Economists Forum:

Forcing institutions to raise capital, be it private or public, at panic-driven fire sale prices threatens enormous dilutions to already shell-shocked shareholders, further exacerbating uncertainty and fuelling the downward spiral. This is self-defeating.

The question then is whether it is feasible to run a (nearly) capital-less financial system until panic subsides. If it is, then a solution to the financial crisis is in sight since it would free up trillions of dollars of hard to raise funds, covering more than even the most extreme estimate of losses.

I believe it is feasible to run such a system for a while, because, essentially, distressed financial institutions need (regulatory) capital for two basic purposes: To act as a buffer for negative shocks, and to reduce their risk-shifting incentives by exposing them to their losses.

However these two functions can be replaced, respectively, by the provision of a comprehensive public insurance, and by strict (and intrusive) government supervision while this insurance is in place.

A few days ago the UK announced a policy package that almost got it right, by pledging to insure banks’ balance sheets and other private liabilities.

Unfortunately, it backfired and caused a worldwide run on financials because it did not dissipate, and even exacerbated, the fear of forced capital raising (or nationalisation).

The events following Lehman’s demise should have taught us that this fear needs to be put to rest until we can return to normality. Financial institutions are too intertwined to predict with any precision the impact of diluting any significant stakeholder, and the markets are too fearful to feed them more uncertainty. Strong guarantees with strict supervision, and the commitment of no further capital injections at fire sale prices (directly or through convertible bonds) should go a long way in building a foundation for a sustained recovery. -

Buy List Updates

Eddy Elfenbein, January 26th, 2009 at 10:48 amThere are a couple of items to pass along this morning. Danaher’s (DHR) earnings were down from last year, but the company still beat estimates. Excluding charges, DHR made $1.11 a share, seven cents more than what the Street was expecting. The stock has been up by as much as 11% this morning.

Moog (MOG-A) also has a good earnings report, but it lowered its revenue estimate for this year. The company’s Q1 EPS came in at 70 cents which is up from 64 cents last year, plus it’s two cents more than Street expectations. Moog cut its revenue outlook for the year from $2 billion to $1.95 billion. The shares are up about 5% so far today.

Stryker (SYK) was downgraded from Buy to Hold by Needham. The company reports earnings tomorrow (Andrew Leckey has a good summary of SYK). Bed Bath & Beyond (BBBY) was downgrade by J.P. Morgan from neutral to underweight, although the downgrade doesn’t seem to be hurting the shares at all.

Overall, the Buy List is having a good morning. -

The Peter Schiff Backlash Begins

Eddy Elfenbein, January 26th, 2009 at 10:05 amI’ve been saying for some time that I’m not particularly impressed with Peter Schiff and his hyper-bearish calls. Fortune just had an article on how prescient Schiff has been: “As one of the few talking heads who loudly, relentlessly, and more or less accurately sounded the alarm about the mortgage bubble and its consequences – in the process becoming the latest bearish commentator to earn the moniker “Dr. Doom” – Schiff has suddenly emerged as a cult hero and something of a minor celebrity.”

Well, Dr. Doom has predicting disaster for several years now, and what we’re seeing now isn’t quite what Schiff predicted. Jonas Elmerraji of the Rhino Stock Report writes:While Schiff has proved himself as an economist, his ability to parlay those predictions into profits for his clients was questionable for 2008. For the last few years, he’s been betting big on overseas investments and precious metals – two areas that got hit as hard or harder than the S&P last year.

According to Morningstar, the average international equity fund performed 7% worse than the average U.S. stock fund in the last year.

Just look at the iShares MSCI Belgium (EWK), the worst performing ETF last year according to SmartMoney.com, or the iShares FTSE/Xinhua China 25 ETF (FXI), which lost 49% in 2008.

Another of Schiff’s investment strategies has been to exit the U.S. dollar in favor of more fundamentally sound currencies. This too has proved untimely since anxious treasury investors have driven up the dollar in the last year.

And some, like Seeking Alpha contributor Todd Sullivan, are quick to remind investors that Peter Schiff has been bearish on the market since at least 2002, when the S&P was poised to move up 48% over the next five years.Mish breaks it down in list form:

12 Ways Schiff Was Wrong in 2008

* Wrong about hyperinflation

* Wrong about the dollar

* Wrong about commodities except for gold

* Wrong about foreign currencies except for the Yen

* Wrong about foreign equities

* Wrong in timing

* Wrong in risk management

* Wrong in buy and hold thesis

* Wrong on decoupling

* Wrong on China

* Wrong on US treasuries

* Wrong on interest rates, both foreign and domestic

That’s a lot of things to be wrong about, especially given all the “Peter Schiff Was Right” videos floating around everywhere. The one thing he was right about was the collapse of US equities and no part of his investment strategy sought to make a gain from that prediction.

Peter Schiff concludes many of his articles, books, etc. with the claim he saw this coming and “positioned his clients accordingly”. -

The Obama Plan

Eddy Elfenbein, January 25th, 2009 at 11:46 amPresident Obama has laid out his plans to revive the economy, and the price tag will be “at least $820 billion.” Something tells me that the “at least” part means “at the very, very least.”

Obama’s goal is to create four million jobs. Dean Baker works out the math and says that the plan comes down to $65,000 per job.

In my mind, the empirical evidence in favor a stimulus package is, at beat, inconclusive. The major problem, however, is that the recovery plan is no longer theoretical—we can see what it is. A lot of this spending isn’t for short-term fiscal stimulus, it’s merely larger government. The Washington Post opines:Helping hire, equip and pay police, a $4 billion item under the bill, might be a good idea, but writing checks to individual households for the same amount would do more to stimulate the economy. Ditto for $16 billion in Pell Grants for college students, $2.1 billion for Head Start and $50 million for the National Endowment for the Arts. All of those ideas may have merit, but why do they belong in an emergency measure aimed to kick-start the economy?

The short answer is, they don’t belong. I expect the plan to sail through Congress. The only upside I see is that future economists will now have another bit of evidence to weight.

-

Contra Geithner

Eddy Elfenbein, January 23rd, 2009 at 12:38 pmJoe Weisenthal makes the case against Geithner:

We know that not everyone would’ve made the same decision here. We’ve worked with people in our professional life, who everytime they encountered something legally or ethically murky opted to make the conservative choice that wasn’t immediately beneficial to them. They do exist, believe it or not. We suspect a guy like Warren Buffett would’ve asked for a professional opinion on the tax issue, were he in that same position.

Again, it’s not that Geithner is so bad, it’s just that his mindset is apparently similar to the people who got us here. Substitute “Moody’s” for “TurboTax” and it should be be obvious.

It’s moot at this point. The speed of the banking crisis means the full Senate will sign off on today’s finance committee vote. But we will soon have a Treasury Secretary who was basically of the same mindset as everyone else, rather than a real clean break from the failed, convenient thinking of the past.Geithner said he simply made a mistake on his taxes and apologized. Well, the apology is good but it misses the point, the mistake is the issue. Calling it one doesn’t diminish the significance. The Secretary of the Treasury should know how to do his taxes without making obvious, boneheaded mistakes.

Larry Ribstein has more.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His