Archive for 2013

-

Trader Gets 30 Months for Moving Decimal Point

Eddy Elfenbein, November 20th, 2013 at 3:22 pmSmooth move, Einstein (via Fortune).

Last fall, David Miller thought he’d found a sure-fire way to dig himself out of debt.

The Rochdale Securities trader had watched Apple (AAPL) shares fall in the space of a month from above $700 to below $600. Earnings were due out Oct. 25, and Miller expected what analysts call a positive surprise.

He took a client’s order for 1,625 shares of Apple, moved the decimal point three places, and bought 1.6 million shares — a billion dollars worth — using his employer’s capital for collateral.

Unfortunately for Miller, and for Rochdale, Apple’s surprise was the other kind. Earnings missed for the second quarter in a row and gross margin guidance disappointed Wall Street. Apple went down, not up.

On paper, Miller had just lost $30 million of someone else’s money.

By the time the dust settled, Rochdale Securities had gone out of business, 40 people had lost their jobs and Miller was in federal court in Hartford, CT, pleading guilty to wire fraud charges that carried a possible sentence of 30 years in prison.

He got 30 months.

At Tuesday’s sentencing hearing, according to the Hartford Courant’s Edmund Mahoney, Miller gave a long and teary apology. “I don’t deserve to be forgiven.

-

The Fed and Communication

Eddy Elfenbein, November 20th, 2013 at 2:47 pmBen Bernanke gave an interesting speech yesterday about Federal Reserve policy and communication. You can see the complete text here. Bernanke said that one of his goals as Fed Chair was to make the Fed more transparent. I think he’s done a good job there, but the markets were surprised earlier this year when the Fed didn’t start tapering as many folks had expected. I think this episode was the impetus for Bernanke’s speech.

Let’s step back and remember that an interesting quality of monetary policy is that expectations matter. The public has to believe that you’re credible for your policy to work. If they think you’re going to stand behind your policy, then the policy will be much more effective. This is also why there’s been a growing emphasis on targeting specific economic indicators.

Bernanke that explained that in response to the crisis, the Fed had lowered interests to 0%. While they couldn’t go below 0%, the Fed could communicate their intentions to keep rates down there for a long time. At first the Fed used language to convey their intentions (“some time” or “extended period”), but the market wasn’t getting the clue. So two years ago, the Fed started using specific dates, and Wall Street finally got the idea.

The Fed kept pushing out the date, so now the market was concerned about what indicators the Fed was watching. So last December, the Fed said, “Fine, here are some numbers, but don’t freak out. These are thresholds, not triggers.”

Here’s where Bernanke explained the troubles following his June presser:

Having seen progress in the labor market since the beginning of the latest asset purchase program in September 2012, the Committee agreed in June of this year to provide more-comprehensive guidance about the criteria that would inform future decisions about the program. Consequently, in my press conference following the June FOMC meeting, I presented a framework linking the program more explicitly to the evolution of the FOMC’s economic outlook.

(…)

The framework I discussed in June implied that substantial additional asset purchases over the subsequent quarters were likely, with even more purchases possible if economic developments proved disappointing. However, following the June meeting and press conference, market yields moved sharply higher. For example, between the FOMC meetings of June and September, the 10-year Treasury yield rose about 3/4 percentage point and rates on MBS increased by a similar amount.

(…)

(M)arket participants may have taken the communication in June as indicating a general lessening of the Committee’s commitment to maintain a highly accommodative stance of policy in pursuit of its objectives. In particular, it appeared that the FOMC’s forward guidance for the federal funds rate had become less effective after June, with market participants pulling forward the time at which they expected the Committee to start raising rates, in a manner inconsistent with the guidance.

To the extent that this third factor–a perceived reduction in the Fed’s commitment to meeting its objectives–contributed to the increase in yields, it was neither welcome nor warranted, in the judgment of the FOMC. This change in expectations did not correspond to any actual lessening in the FOMC’s commitment or intention to provide the high degree of monetary accommodation needed to meet its objectives, as Committee participants emphasized in subsequent communications.

At its September 2013 meeting, the FOMC applied the framework communicated in June. The Committee’s decision at that meeting to maintain the pace of asset purchases was appropriate and fully consistent with the earlier guidance. The Committee was looking for evidence that job market gains would continue, supported by a pickup in growth. As it happened, the implications for the outlook of the evidence reviewed at the September meeting were mixed at best, while the ongoing fiscal debates posed additional risks. The Committee accordingly elected to await further evidence supporting its expectation of continued improvement in the labor market. Although the FOMC’s decision came as a surprise to some market participants, it appears to have strengthened the credibility of the Committee’s forward rate guidance; in particular, following the decision, longer-term rates fell and expectations of short-term rates derived from financial market prices showed, and continue to show, a pattern more consistent with the guidance.

-

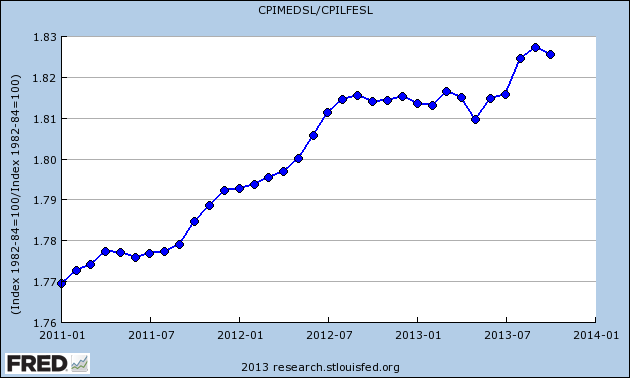

Healthcare Costs Update

Eddy Elfenbein, November 20th, 2013 at 12:02 pmThe government released the October CPI report this morning. Once again, inflation continues to be tame. Consumer prices fell 0.1% last month which was the first drop in six months. The “core rate,” which excludes food and energy, rose by 0.1%.

What I wanted to see was the trend of medical costs versus core inflation. Medical costs had been outpacing core inflation for decades, but that abruptly slowed down last year. There was, however, a recent uptick in medical costs in August, but that trend may have already faded.

Here’s the chart of medical costs divided by core inflation.

From August 2012 to July 2013, the rise in medical costs was almost the same as the rise in core prices. If this continues, that’s a game changer.

-

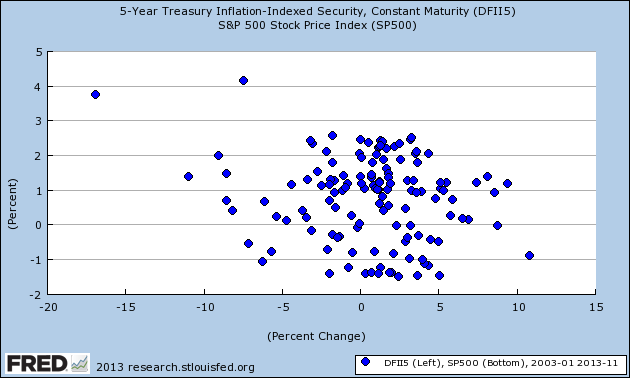

Equity Returns and TIP Yields

Eddy Elfenbein, November 20th, 2013 at 10:24 amHere’s a look at the relationship between equity returns and the yield on 5-year Treasury Inflation Protected securities. The 5-year TIPs yield is the y-axis and the monthly gain/loss of the S&P 500 is the x-axis.

I haven’t run a regression but by eye-balling the chart, there seems to be a weak negative correlation. In other words, the dots kinda form a downward sloping trend. This makes sense — the lower the real yield you get in fixed income, the greater the desire for alternatives.

Earlier this year, the 5-year TIPs yield shot up from around -1.4%, where it had been for a few months, to -0.2% in just a few weeks. Later, it broke into positive territory for a brief shining moment. Currently, the yield is hanging out around -0.47%.

-

Morning News: November 20, 2013

Eddy Elfenbein, November 20th, 2013 at 6:58 amBOE Sees Case for Keeping Record-Low Rate Beyond 7% Jobless

FX Dealers Said to Use Day Traders to Make Personal Bets

As Myanmar Modernizes, Old Trades Are Outpaced By New Competitors

Citing Fed’s Efforts, Bernanke Says U.S. Economy Is Growing Stronger

Yahoo Boosts Share Buyback by $5 Billion

GlaxoSmithKline to Divest $740 Million Stake in South Africa’s Aspen

Roark Capital Group to Acquire CKE Restaurants from Apollo Global Management

Nissan Unfazed by EV Delays, Dismisses Rivals’ Fuel Cell Targets

Nokia Investors Approve Phone Unit’s Sale to Microsoft

Lowe’s Raises Outlook As Housing Rebound Boosts Sales

Staples Quarterly Sales Fall 4%

In Extracting Deal From JPMorgan, U.S. Aimed for Bottom Line

JPMorgan’s Mortgage Confessions Don’t Include O.J. Simpson

Jeff Miller: Four Costly Ideas

Cullen Roche: Jeremy Grantham – The Market Bubble Isn’t Here Yet But It’s Coming

Be sure to follow me on Twitter.

-

Newsletter Feedback

Eddy Elfenbein, November 19th, 2013 at 7:43 pmCWS Market Review just celebrated its third birthday and I’d like to ask you for feedback. Tell me what you like about it, and what you don’t like. Is it too short? Too long? Too in-depth or not deep enough? Should it come more often or on different days of the week? Let me know! I want to hear from you.

Just send me an email with “Feedback” in the subject line. Also, don’t be shy in saying that it’s fine as is. That’s important feedback as well.

-

Lower Oil Helps Retail

Eddy Elfenbein, November 19th, 2013 at 12:33 pmOne of my goals with this blog is to help people think properly about investing. For example, I often caution against folks looking to predict the next big bubble.

The following is a good example of how people ought to approach investment analysis. Over the last two years, oil stocks (black line) have not done very well relative to the broader market. At the same time, the retail sector (blue line) has done quite well.

These two events are related. Lower prices at the pump act like an immediate tax cut for consumers. What do they do with that money? They spend it. Of course, there would be times when consumers simply sit on that cash. Please note that we’re talking about relative performance. Where retail leads the market is exactly where oil falls short.

Check out this chart:

-

Medtronic Earns 91 Cents per Share

Eddy Elfenbein, November 19th, 2013 at 9:16 amMedtronic’s ($MDT) second-quarter earnings are out and the company earned 91 cents per share. That’s one penny better than estimates. This was a solid quarter for MDT; quarterly revenue was up 2.4% to $4.19 billion. Medtronic’s CEO Omar Ishrak said, “Our second quarter revenue growth was in-line with our outlook for the year, and we are performing at or better than the market in almost every one of our business lines.” That’s something nice to hear from your CEO.

The WSJ:

Sales in the cardiac rhythm disease management segment, which includes defibrillators, pacemakers and tools for treating a common rhythm disorder rose to $1.27 billion, up 5% excluding currency fluctuations. Overall defibrillators revenue increased 4% while pacemaker sales grew 2%, excluding currency impacts.

Medtronic’s spinal-products business posted a sales decline of 3% excluding currency impacts.

Most importantly, Medtronic reaffirmed their full-year guidance of $3.80 to $3.85 per share. They see revenue rising by 3% to 4%. Note that MDT’s fiscal year ends in April. The shares are close to the 52-week high from last week, which was the highest price in nearly eight years. The all-time high was $62 per share from December 2000.

-

Morning News: November 19, 2013

Eddy Elfenbein, November 19th, 2013 at 6:44 amO.E.C.D. Forecasts Lower Growth for Euro Zone

Wall Street Pushes Back on CFTC’s Advisory for Overseas Swaps

Alan Greenspan: Never Saw It Coming

Fed Ponders How to Temper Tapering Without Rate Increase

Regulators See Value in Bitcoin, and Investors Hasten to Agree

Was Carl Icahn Right to Put a Damper on Markets?

U.S. Poised to Announce $13 Billion JPMorgan Settlement

BNY Mellon Says $8.5 Billion BofA Deal ‘Easy Decision’

Dutch Firm to Spin Off Drug Making Business in $2.6 Billion Deal

U.S. Regulator Opens Probe of Fire in Tesla Electric Cars

Labor Panel Finds Illegal Punishments at Walmart

Hollywood Studios Facing Upheaval at Highest Levels

Joshua Brown: Dow Breaks 16,000, S&P Breaks 1,800, Whatever.

Roger Nusbaum: Markets Have More Moving Parts Than That

Be sure to follow me on Twitter.

-

Buffett Buys ExxonMobil

Eddy Elfenbein, November 18th, 2013 at 3:57 pmLast week Warren Buffett revealed that he bought a cool $3.7 billion worth of ExxonMobil ($XOM). That’s about 1% of the total company. Non-professional Investors should take note that Buffett is buying a blue-chip stock which hasn’t done very well. So many investors think you should only buy stocks near their highs.

I’ve been puzzled by XOM’s poor performance. Just a few weeks ago, I did a blog post asking “What Happened to ExxonMobil?” Since the beginning of the bull market in 2009, XOM has not only lagged the S&P 500, but it’s lagged the Energy Sector as well. I noted that if XOM had merely kept pace with the S&P 500, their market cap would be over $700 billion today.

So is it a buy now? I’m on the fence. I think the stock is cheap but I can’t say how strong the long-term potential is. But if Buffett is doing it, then it’s probably a very smart move.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His