Archive for 2013

-

Morning News: November 14, 2013

Eddy Elfenbein, November 14th, 2013 at 6:52 amEuro Zone Economy Stagnates as Growth Slows in Germany

Top Japan Banks’ Second-quarter Earnings Leap Thanks to ‘Abenomics’ Bull Market

JPMorgan’s Fruitful Ties to a Member of China’s Elite

Spy Scandal Weighs on U.S. Tech Firms in China, Cisco Takes Hit

New Catfish Inspections Are Posing a Problem for a Pacific Trade Pact

Yellen Says Economy Performing Far Short of Potential

Rejecting Billions, Snapchat Expects a Better Offer

Swiss Chocolate Maker Barry Callebaut Opens Factory in Japan in Rare Foreign Investment Coup

Macy’s Reverses Lackluster Quarter, Helped by Ad Campaign

EADS Third-Quarter Profit Rises on Higher Airbus Jet Deliveries

Apple Sticks to Winning Script in Samsung Damages Retrial

Italy Investigates Apple for Alleged Tax Fraud

Investment Manager Explains Why 99.5% of Americans Can Never Win

Edward Harrison: The Deflationary Forward Guidance Threshold

John Hempton: The FDA, Statistics and Fundamentalism

Be sure to follow me on Twitter.

-

The Surge In Consumer Services

Eddy Elfenbein, November 13th, 2013 at 11:38 amHere’s something I didn’t anticipate (which is a large category of things). The Consumer Services Sector has soared over the past few years, and it’s gotten stronger every day.

What’s interesting is that this sector had basically kept up with the broader market for years. Starting in mid-2008, it started to break away. The index has barely taken a break in the last two years.

Note that this is the Dow Jones U.S. Consumer Services Index which is similar (I believe) to the what the S&P calls its S&P 500 500 Consumer Discretionary Index.

-

Morning News: November 13, 2013

Eddy Elfenbein, November 13th, 2013 at 6:12 amU.K. Unemployment Falls to 7.6% in Move Toward BOE Threshold

Central Banks Risk Asset Bubbles in Battle With Deflation Danger

House Stalls Trade Pact Momentum

Dollar Rises to 2-Month High Versus Yen on Fed Bets

Gary Gensler’s Successor Has His Work Cut Out for Him

It’s Getting Closer to Panic Time for Healthcare.Gov

Starbucks Concludes Packaged Coffee Dispute With Kraft

Baidu Faces Lawsuit Over Video Piracy

CNPC, PetroChina to Buy Peru Oil, Gas Assets From Petrobras for US$2.6 Billion

WTI Trades Near Five-Month Low as U.S. Supplies Seen Rising

Jos. A. Bank Tries to Look Like a Catch for Men’s Wearhouse

Rosneft Beats Rivals to Grab Enel’s $1.8 Billion SeverEnergia Stake

Samsung Says It Will Supply Half Of The Smartphones In Africa This Year

Joshua Brown: Everything You Need to Know About Stock Market Crashes

Epicurean Dealmaker: The Invention of Leisure

Be sure to follow me on Twitter.

-

The Effect of Inflation on Real Stock Returns

Eddy Elfenbein, November 12th, 2013 at 11:54 amI’ve been doing more splicing of the Ibbotson data. Today, let’s look at the effect inflation has had on real stock returns. This may seem counter-intuitive but the more consumer prices rise, the worse stock prices have done. This makes sense since stocks are in competition with bonds, not consumer prices, and bonds do worse as inflation rises. At the other end, real stock markets have done very poorly under deflation. Historically, what the market appears to like best is low, stable inflation.

Now let’s look at some numbers. I took all of the monthly returns from 1925 to 2012 and broke them into three groups; there were 75 months of severe deflation (greater than -5% annualized deflation), 335 months of severe inflation (greater than 5% annualized), and 634 months of stable prices (between -5% and +5%).

The 75 months of deflation produced a combined real return of -46.77%, or -9.60% annualized. The 335 months of high inflation produced a total return of –70.84%, or -4.32% annualized. The 634 months of stable prices produced a stunning return of more than 177,000%. Annualized, that works out to 15.21%, which is more than double the long-term average.

Here’s an interesting stat: The entire stock market’s real return has come during months when annualized inflation has been between 0% and 5.1%. The rest of the time, the stock market has been a net loser.

-

One Full Year Above the 200-DMA

Eddy Elfenbein, November 12th, 2013 at 10:50 amThis Saturday will mark the one-year anniversary of the S&P 500’s last close below its 200-day moving average. This run represents both the market’s climb and its low volatility. The end result is a steady march upward.

-

Morning News: November 12, 2013

Eddy Elfenbein, November 12th, 2013 at 6:32 amU.K. Inflation Slows More Than Forecast to Least in a Year

Compared to CFTC, Heading TARP May Have Been Easy Job

U.S. Nears Energy Independence by 2035 on Shale Boom, IEA Says

Gold Extends Drop to Three-Week Low on Outlook for U.S. Stimulus

Alibaba Breaks Sales Record Amid China Singles-Day Rebate

Here Are Six Reasons Twitter’s Stock Will Be Volatile

Shire of Ireland to Pay $4.2 Billion for U.S. Drug Maker

Vodafone Adds to Network Spending as Sales Miss Estimates

News Corp Misses Revenue Target As Australian Income Slumps

Transocean Yields to Icahn, Pursuing a Trendy Strategy

World Trade Center Tower Debuts in Manhattan Leasing Test

More Anxious Retailers Will Open Earlier on Thanksgiving

Cullen Roche: Hatzius: Baseline for Taper is March 2014

Credit Writedowns: Low Inflation is Creating a QE Trap

Be sure to follow me on Twitter.

-

Transocean Soars

Eddy Elfenbein, November 11th, 2013 at 5:22 pmI had been looking at Transocean ($RIG) as a possible candidate for next year’s Buy List. Unfortunately, a lot of RIG’s big discount evaporated over the past few days.

The company said Monday that it has agreed to support a dividend of $3 per share and reduce the size of its board. It is also looking to boost margins by $800 million through cost-cutting efforts and other measures. Transocean’s stock jumped 3.8% to $55.47 in early Monday trading.

Icahn, a minority shareholder in Transocean, had previously pushed for a $4 per share dividend but Transocean’s shareholders rejected it. Icahn, known for shaking up companies in which he invests, had also wanted several board changes.

Transocean isn’t out of the running for the Buy List, but its candidacy obviously isn’t as strong.

-

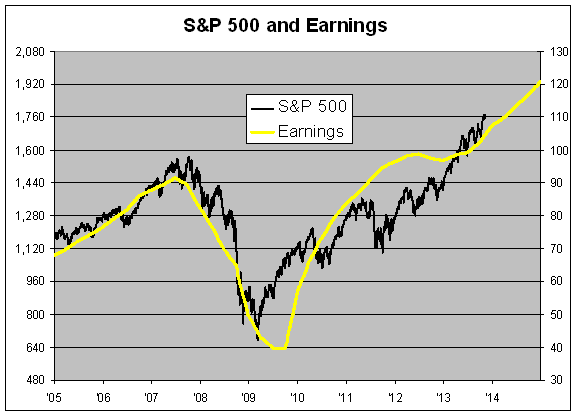

Are We in a Bubble?

Eddy Elfenbein, November 11th, 2013 at 10:44 amThe latest rage on Wall Street is to pronounce that stocks are in a bubble. This is rather unusual in that true bubbles are very rare. This is, of course, different from stocks dropping in a routine lousy market. That happens every few years.

Do I think that stocks are in a bubble? Honestly, I don’t know. And more importantly, I don’t much care. Let me explain.

For one, it’s odd to make a judgment about the aggregation of 6,000 publicly traded stocks. Our Buy List is pretty well diversified and that’s just 20 stocks. Where the entire S&P 500 is headed isn’t that important for a disciplined stock picker.

Also, even if the market is about to plunge, it’s very difficult to get the timing just right. Lots of people saw the housing bubble but they were very early. The bubble kept on going. Recently I noted that if an investor bought an S&P 500 index fund just prior to the Financial Crisis, say in March 2008, and held on to today, they would have made a decent return by historical standards. Time may not heal investing wounds, but it sure can help a lot.

When looking at valuation metrics, I urge investors to look at as many as they can, but never be a slave to just one. I’m particularly leery of metrics like the Cyclically Adjusted P/E ratio, also known as CAPE. The CAPE looks at the stock market’s current value weighted against the last ten years of earnings. The idea is to smooth out the economic cycles. I think this is a bad idea because stocks and earnings are themselves cyclical.

Also, the inclusion of so much prior data is, in my opinion, an unfair anchor to carry. The historic plunge in corporate earnings in 2008-09 will still be a part of CAPE for another five years. If we look at operating earnings or dividends, we can see what an outlier that profit data is. Interestingly, the market’s dividend yield has remained fairly consistent for the last decade, except for the worse parts of the Financial Crisis.

After two of the biggest bear markets in history is precisely when so many people are scared of another bubble. I’m reminded of people saying that shortly after 9/11 was actually the safest time to fly. Bubbles are now, apparently, everywhere.

I think the best way to look at the issue is to divide bear markets into two categories. One is where price shoots far above value. That’s your classic bubble ala 1987 or 2000. The second is when value crumbles beneath price. That happened in 1990 and 2008.

You might be surprised to hear me say that 2008 wasn’t a bubble. That’s right; stock valuations really weren’t that excessive. It was the fundamentals that turned out to be terrible. Believe it or not, stock valuations were above average in 1929, but not out of sight. The frothiest part of the bull market occurred in the last six months. The 1920s was not a decade of stock euphoria.

I think there’s a natural tendency to reverse engineer a narrative that the world was enthralled to greed and everyone bought stocks without thought. That describes the feeling about Tech stocks in 1999, but it’s not an accurate description of today’s environment. The S&P 500 is going for about 17 times this year’s earnings. That’s about normal. The P/E Ratio has risen over the last two years, but it’s really gone from low to average, not from normal to nose-bleed territory.

Analysts currently estimate that the S&P 500 will earn $120 per share next year. Now’s the time for skepticism. For one, analysts don’t have a great forecasting track record. The critical question is, could fundamentals soon fall apart? Are there hidden factors that might make the S&P 500 earnings, say, $90 or even less next year? This is the question to worry about.

It’s also hard to predict things that are unexpected because, well, they’re not expected. If they were expected, they probably would be much less interesting. Also, it’s the unexpectedness of an event that makes it important.

The things that worry me are the things we aren’t thinking about. For one, corporate profit margins are very high. I think it’s reasonable to expect that earnings growth will be below economic growth over the next several years. Though the high profit margins probably aren’t a reflection of corporate greed, rather they’re a natural byproduct of slow growth and low interest rates.

Earnings recessions generally don’t announce themselves beforehand, but there are some useful warning signs. One good indicator is the yield curve. When short-term rates rise above long-term rates, the economy often runs into trouble soon after. For now, the yield curve is far from inverted.

Another late cycle indicator is rising inflation. According to the latest numbers, that’s not a problem either. I also like to follow the monthly ISM reports. A reading below 45 is often a sign of trouble. Once again, we’re in the safe zone.

(You can sign up for my free newsletter here.)

-

Scattered Thoughts on Twitter

Eddy Elfenbein, November 11th, 2013 at 10:21 amJust about everything that could be said about Twitter’s IPO has been said. Still, I wanted to add a few scattered thoughts.

Twitter is another good example of a stock where fundamental analysis is basically useless. By any reasonable valuation metric, Twitter is vastly overpriced. That’s not a novel insight. However, that doesn’t mean Twitter’s stock won’t do well.

The reason is that fundamental analysis assumes a level of environmental consistency that doesn’t exist in Twitter’s business. Who knows what their business will look like in a few years? Yet I have a pretty good idea what Harris’s business will look like. This is why I’m staying away from Twitter. I simply can’t offer a reasonable estimate as to what their profit will be. But I do wish them well.

After a big IPO like Twitter, you often hear that the company “left money on the table.” Perhaps. But I think that misses a few key points.

Remember that Twitter floated a relatively small amount of shares. Look at it from their point of view. One issue is that the company has a lot of people working for them who were paper millionaires, and their wealth was very illiquid. The company doesn’t want to alienate long-time employees. Now that Twitter is public, those people are much wealthier, and even factoring in a lock-up period, their wealth is far more liquid than it was before.

We also have to consider the major benefit of an inflated stock price. Twitter can now print money for free which they can use for acquisitions. In other words, their shares are a currency. Every central bank in the world longs for this. Expect to see Twitter roll up a lot of small tech firms, and they’ll use their stock to close the deal.

When looking at stocks, we often talk about price versus value. But this is a good example of the two concepts blurring. An elevated stock price is itself a boost to value because it can aid your financial strategy. I wouldn’t say that a rich valuation can turn a bad company into a good one, but it has helped many good companies become better.

There isn’t much better defense than owning stocks of firms that know what they’re doing.

-

Morning News: November 11, 2013

Eddy Elfenbein, November 11th, 2013 at 6:14 amEuro Zone’s Fizzling Growth Seen to Back Draghi Cut Case

German Bonds Climb Before Growth Report as Yield Curve Steepens

Online Shopping Marathon Zooms Off the Blocks in China

Brent Rises After Iran Talks Fall Short of Agreement

Yellen to Get Quizzed as Taper-Timing Debate Rages

Supreme Court to Take Up Challenges to Union Practices

Postal Service to Make Sunday Deliveries for Amazon

Shire Buys U.S. Drug Firm ViroPharma for $4.2 BIllion

Grifols to Acquire a Novartis Diagnostics Business Unit for U.S. $1,675 Million

Transocean Reaches $1.1 Billion Dividend Accord With Icahn

Panasonic Says Ready to Spend $1 Billion on New Deals

If You Believe in Bitcoin, You Should Never Buy Anything in Bitcoin

Jeff Miller: Weighing the Week Ahead: Do Sidelined Investors Face Upside Risk?

Roger Nusbaum: The Dude Who Came Up With 4% Rule Tells Barron’s It Might Not Work and Allowing For The Possibility of Risk

Be sure to follow me on Twitter.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His