Archive for 2013

-

Today’s Fed Statement

Eddy Elfenbein, June 19th, 2013 at 2:02 pmInformation received since the Federal Open Market Committee met in May suggests that economic activity has been expanding at a moderate pace. Labor market conditions have shown further (in May, this was simply “some” – Eddy) improvement in recent months, on balance, but the unemployment rate remains elevated. Household spending and business fixed investment advanced, and the housing sector has strengthened further, but fiscal policy is restraining economic growth. Partly reflecting transitory influences, inflation has been running below the Committee’s longer-run objective, but longer-term inflation expectations have remained stable.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with appropriate policy accommodation, economic growth will proceed at a moderate pace and the unemployment rate will gradually decline toward levels the Committee judges consistent with its dual mandate. The Committee sees the downside risks to the outlook for the economy and the labor market as having diminished since the fall (this sentence is new, in May they didn’t say anything about diminishing). The Committee also anticipates that inflation over the medium term likely will run at or below its 2 percent objective.

To support a stronger economic recovery and to help ensure that inflation, over time, is at the rate most consistent with its dual mandate, the Committee decided to continue purchasing additional agency mortgage-backed securities at a pace of $40 billion per month and longer-term Treasury securities at a pace of $45 billion per month. The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. Taken together, these actions should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative. (This paragraph is exactly the same as in May.)

The Committee will closely monitor incoming information on economic and financial developments in coming months. The Committee will continue its purchases of Treasury and agency mortgage-backed securities, and employ its other policy tools as appropriate, until the outlook for the labor market has improved substantially in a context of price stability. The Committee is prepared to increase or reduce the pace of its purchases to maintain appropriate policy accommodation as the outlook for the labor market or inflation changes. In determining the size, pace, and composition of its asset purchases, the Committee will continue to take appropriate account of the likely efficacy and costs of such purchases as well as the extent of progress toward its economic objectives. (Same.)

To support continued progress toward maximum employment and price stability, the Committee expects that a highly accommodative stance of monetary policy will remain appropriate for a considerable time after the asset purchase program ends and the economic recovery strengthens. In particular, the Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that this exceptionally low range for the federal funds rate will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored. In determining how long to maintain a highly accommodative stance of monetary policy, the Committee will also consider other information, including additional measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments. When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. (Same.)

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; William C. Dudley, Vice Chairman; Elizabeth A. Duke; Charles L. Evans; Jerome H. Powell; Sarah Bloom Raskin; Eric S. Rosengren; Jeremy C. Stein; Daniel K. Tarullo; and Janet L. Yellen. Voting against the action was James Bullard, who believed that the Committee should signal more strongly its willingness to defend its inflation goal in light of recent low inflation readings, and Esther L. George, who was concerned that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations. (The voting was the same except for Bullard’s dissent. Esther George’s dissent used the same language as May. So two dissents; one hawk, one dove)

-

Scalpel Man

Eddy Elfenbein, June 19th, 2013 at 8:34 am

Can moral probity go hand in hand with the profit motive? Can one be at once a feared hedge-fund manager and a crusader for Wall Street reform?

If so, it wouldn’t be the least of David Einhorn’s achievements.

At 44, Einhorn is one of the youngest members of the Forbes 400, with a net worth of $1.25 billion. His hedge-fund firm, Greenlight Capital, was started in 1996 with just $900,000, but today is brushing up against $9 billion in assets and has yielded annualized returns of almost 20%. Einhorn is a ferocious investor, one who is unafraid to roll up his sleeves, dig deep into the bowels of a company’s fundamentals, and then report on the patient’s vital state, good or bad. When he does, companies tremble. His talks at investor conferences are eagerly attended by the Street’s best and brightest, and the grinding exhaustiveness with which he researches firms has earned him the near-worship of money managers everywhere. Nor is he loath to stoop for his weapons: his signature strategy is the short sell, which entails betting that a firm’s stock will fall and then profiting from the drop. For this, he has been reviled by some of the Street’s more genteel spokesmen. But Einhorn is cheerfully, boyishly unrepentant. He has clashed with some of the most imposing giants on Wall Street—Lehman Brothers, Microsoft—and (usually) won.

Einhorn can thus hunt with the fiercest of the wolves. But—and this is the intriguing part—there’s also a lamb under his lupine exterior. For him, aggressive investing strategies, short-selling included, are a kind of moral scalpel for the ailing patient that is the U.S. financial system.

The New York Times’ Op-ed page, January 3, 2009: “short-sellers [are] the only market players who have a financial incentive to expose fraud and abuse.”

A case in point was Einhorn’s 2002 battle with Allied Capital, a mid-cap lender whom he accused of cooking its books and defrauding the Small Business Administration. In May of that year, after the hedge-fund manager publicly trashed the company at the Ira W. Sohn Investment Research Conference in Lincoln Center, the stock opened down 20 percent. Greenlight Capital, of course, had shorted its shares of Allied, and came out with a hefty profit. But Einhorn had to go through countless headaches for years afterwards as Allied fought a dirty campaign against him, gaining illegal access to his phone records, charging him with market manipulation, and even enlisting the SEC on its side. The SEC later vindicated Einhorn, finding evidence of collusion between Allied and its own bureau chief in charge of the investigation. The hedgie-turned-author later detailed the whole ordeal in a book, Fooling Some of the People All of the Time, arguing that good corporate governance and sound investor strategy need not, indeed should not, be in conflict.

Then there’s Einhorn’s subsequent clash with Lehman Bros., where again he was forced to state some unpleasant, if now obvious, truths. In November of 2007, he publicly criticized the now-defunct firm for being overleveraged and hiding huge liabilities on its balance sheet, principally from asset-backed securities. Once again Greenlight shorted the stock, and once again the resulting drop yielded the fund sizeable profits while simultaneously exposing the Emperor’s state of undress. Einhorn was pilloried as “rabble-rousing” and excessively bearish in the New York Times, a veritable profiteer of panic, but when Lehman went bankrupt less than a year later, the market again vindicated his predictions. He later said short-selling the firm was not just profitable but “the right thing to do.”

Einhorn has been outspoken about the systemic corruption of the American financial system. In his op-ed for the New York Times, he charges that too often, the institutions responsible for keeping Wall Street’s excesses in check, principally the SEC and credit-rating agencies such as Moody’s, have been corrupted and are now acting in tandem with the companies they are supposed to regulate. As a result, the financial system becomes ever more rabid in its quest for short-term profits—and ever more heedless of the long-term consequences, moral as well as monetary, of its actions. Einhorn’s own experiences would seem abundantly to bear this out.

Not all of Einhorn’s arrows have hit the mark. In 2012, Greenlight made some bad deals, finishing the year with a 7.9% return, significantly below the S&P’s 16%. Worse still, the fund became entangled in protracted legal squabbles with Apple, largely over technicalities, in what increasingly seemed to be a losing attempt to force the computer giant to issue preferred stock and so pay out some of its cash reserves to shareholders. This battle pitted him not just against The California Public Employees’ Retirement System and Institutional Shareholder Services (as well as Apple’s management), but against other respected investors such as Warren Buffett, and at times even against the market itself, which continued to boost Apple’s share price before it hit a high last September. But Einhorn has never been afraid to go against the grain. And as with his previous clashes, time will reveal whether his ideas are visionary or merely eccentric.

Bad calls aside, what makes Einhorn an exemplary investor is his fierce independence of mind, coupled with sound fundamental principles. The Wall Street hothouse is much given to using the epithet “genius” for anyone who trumps the market for a few quarters, but Einhorn has always followed a strategy any bright seventh-grader can understand: at the end of the day, your portfolio is only as solid as the companies it contains. Do your homework, ask the hard questions, and always do the right thing. If you don’t, sooner or later you’ll wish you had.

In his own words:

I think that there is a social value in identifying companies that are doing bad things and betting against them. I’ve seen the demise of a fair number of these companies, and it’s not because we’ve bet against them, it’s because these were flawed companies.…[With short selling,] it’s self-evidently true that if the stock goes down we are positioned to make a profit. The question is, is that the whole story? And the answer is, it really isn’t.

Indeed, with Einhorn, it really isn’t.

(Click here to sign up for my free weekly newsletter.)

-

Morning News: June 19, 2013

Eddy Elfenbein, June 19th, 2013 at 7:46 amIMF Gives Spain A Thumbs Up, Warns Of Risks

King Eyes Parting Shot at Bankers Gearing Up for Carney

EU Fines Drug Firm Lundbeck Over ‘Pay For Delay’

G-8 Agrees Proposals to Tackle Tax Evasion, Avoidance

Treasuries Are Little Changed Before Bernanke Speaks on Stimulus

Inflation at 53-Year Low Gives Bernanke Time to Press on With QE

U.S. Mortgage Applications Down 4% Last Week

FedEx Earnings Jump, But Company To Cut Express Capacity Between Asia And The U.S.

GM Says China Luxury Vehicle Demand Slower Than Expected

Deloitte to Pay NY $10 Million For Misconduct Over Standard Chartered

Alcatel-Lucent Confirms Plan to Slim Down, Refinance

Softbank Closer To Acquiring Sprint After Dish Abandons Bid For Now

Dell Special Committee Responds to Icahn’s Latest Proposal

Pragmatic Capitalism: The Urgent Need to Recapitalize Europe

Phil Pearlman: The Best Thing I Read Today: Chris Nelder & Alt Energy

Be sure to follow me on Twitter.

-

Financial Sector Thinks It’s About Ready To Ruin World Again

Eddy Elfenbein, June 18th, 2013 at 2:21 pmFrom The Onion:

NEW YORK—Claiming that enough time had surely passed since they last caused a global economic meltdown, top executives from the U.S. financial sector told reporters Monday that they are just about ready to completely destroy the world again.

Representatives from all major banking and investment institutions cited recent increases in consumer spending, rebounding home prices, and a stabilizing unemployment rate as confirmation that the time had once again come to inflict another round of catastrophic financial losses on individuals and businesses worldwide.

“It’s been about five or six years since we last crippled every major market on the planet, so it seems like the time is right for us to get back out there and start ruining the lives of billions of people again,” said Goldman Sachs CEO Lloyd Blankfein. “We gave it some time and let everyone get a little comfortable, and now we’re looking to get back on the old horse, shatter some consumer confidence, and flat-out kill any optimism for a stable global economy for years to come.”

“People are beginning to feel at ease spending money and investing in their futures again,” Blankfein continued. “That’s the perfect time to step in and do what we do best: rip the heart right out of the world’s economy.”

According to sources, the overwhelming majority of investment bankers are “ready to get the ball rolling” by approving a host of complex and poorly understood debt-backed securities that are doomed to quickly default, as well as issuing startlingly high-risk loans certain to drive thousands of companies into insolvency.

Top-level executives also told reporters that when it comes to depleting the life savings of millions of people and sending every major national economy into a tailspin, they feel “refreshed and raring to go.”

“The other day I actually overheard someone on the sidewalk utter the words ‘I’m saving up for retirement,’ and right away I thought to myself, ‘Well, time to get down to work,’” said Morgan Stanley chairman James P. Gorman, adding that the increasing number of individuals entertaining ideas of starting their own businesses or buying houses was the financial sector’s cue to set off another devastating global recession. “We’re definitely thinking on a huge scale again, because we all really enjoy toying with the livelihoods of millions of people overseas and forcing them to wonder why reckless, split-second decisions made thousands of miles away dictate their whole country’s socioeconomic future.”

“Plus, it’ll be nice to finally wipe out the Euro once and for all this time,” Gorman added.

While most private equity firms, investment banks, and hedge funds are reportedly still undecided on the precise route to take in order to torpedo the job market and crash all international stock exchanges, sources confirmed they are nearly in position to resume gambling away trillions of dollars belonging to the American populace.

“We’ve got a lot of options on the table; it’s just a matter of picking which one we want to use to paralyze every single sector of the world economy,” said Capital One executive vice president Peter Schnall. “We already burst the dot-com and housing bubbles, so this time we can maybe mix it up by popping the education bubble and shattering the lives of everyone with outstanding student loans. Or maybe we’ll artificially inflate prices of stocks in social media companies and then pull the rug out, bankrupting every investor tied to companies like Facebook and Twitter. Or do both.”

“On second thought, maybe we’ll wipe out the housing market again too, just for the hell of it,” Schnall quickly added. “Might as well, right?”

According to a recent survey of Wall Street officials, 82 percent said they were “excited to shake off the rust” and send the Dow and NASDAQ into another freefall. Additionally, 75 percent of respondents admitted they have been “champing at the bit” for months to wholly undermine the nation’s local banks and money market accounts, leaving Americans too terrified to leave their savings anywhere.

Moreover, the chief financial officers from Bank of America, Citigroup, JPMorgan Chase, and Wells Fargo unanimously told reporters that it has been “way too long” since they last saw the utterly dejected faces of American families whose homes had just been foreclosed on due to circumstances totally beyond their control.

“Now that the public’s efforts to curtail questionable Wall Street trading practices have all but ceased, it’s time for us to bring the world to its knees again,” said AIG CEO Robert Benmosche. “There are still plenty of opaque financial derivatives, high-frequency trading operations, and off-balance sheet transactions out there, all with virtually no federal regulation. Trust me, we can definitely work with that. And if anything, we can always just lobby for further concessions and deregulation in Washington—which, by the way, is so, so easy to do—and then we can cause as much damage as we want.”

Added Benmosche, “And while we’re at it, we’ll make sure we once again come away from this whole thing scot-free and far wealthier.”

-

What to Look for in Tomorrow’s FOMC Statement

Eddy Elfenbein, June 18th, 2013 at 1:32 pmHere’s a look at the last FOMC policy statement and possible changes they may make. This is all just speculation on my part.

The policy statement has six paragraphs. The key tomorrow is the third paragraph which outlines the goals of the QE program.

FIRST PARAGRAPH:

Information received since the Federal Open Market Committee met in March suggests that economic activity has been expanding at a moderate pace.

Same.

Labor market conditions have shown some improvement in recent months, on balance, but the unemployment rate remains elevated.I’d change “some” to “disappointing,” and “but” to “and.”

Household spending and business fixed investment advanced, and the housing sector has strengthened further, but fiscal policy is restraining economic growth.

Same. This statement is key because Fed policy has a more direct impact on housing than it does other sectors.

Inflation has been running somewhat below the Committee’s longer-run objective, apart from temporary variations that largely reflect fluctuations in energy prices.

I’d delete the “somewhat,” but that’s just me.

Longer-term inflation expectations have remained stable.

This should go. Inflation expectations have trended downward.

SECOND PARAGRAPH

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability.

Boilerplate.

The Committee expects that, with appropriate policy accommodation, economic growth will proceed at a moderate pace and the unemployment rate will gradually decline toward levels the Committee judges consistent with its dual mandate.

Blah blah blah.

The Committee continues to see downside risks to the economic outlook.

Same. But what’s on my mind, and others in the Fed, is any negative problems potentially caused by prolonged low rates. The “reach for yield” argument.

The Committee also anticipates that inflation over the medium term likely will run at or below its 2 percent objective.

Same, but I’d be curious if they say anything about the potential of deflation. Actually, it seems very likely that inflation will be below 2% for the short-term.

THIRD PARAGRAPH

To support a stronger economic recovery and to help ensure that inflation, over time, is at the rate most consistent with its dual mandate, the Committee decided to continue purchasing additional agency mortgage-backed securities at a pace of $40 billion per month and longer-term Treasury securities at a pace of $45 billion per month.

This paragraph is the biggie, and I would expect any tapering language to be here. As far as continuing the $85 billion, I strongly doubt will see any change in the short-term.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction.

Same.

Taken together, these actions should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative.

This sentence is difficult to maintain since long-term rates have come up while inflation expectations have fallen. This means that higher real rates have risen. Well, risen to 0%, but you get the idea. I suspect that’s in anticipation of stronger growth, but I don’t know what the Fed will say.

I’d be very interested to hear if the Fed ties any tapering language to specific metrics like NFP. I doubt that will happen, but you never know. It will probably be something like, “with a stronger housing market and financial markets, the Committee doesn’t anticipate asset purchases continuing into 2015.”

FOURTH PARAGRAPH

The Committee will closely monitor incoming information on economic and financial developments in coming months.

Sure.

The Committee will continue its purchases of Treasury and agency mortgage-backed securities, and employ its other policy tools as appropriate, until the outlook for the labor market has improved substantially in a context of price stability.

I’m not sure this sentence will stay. I think the market wants specifics.

The Committee is prepared to increase or reduce the pace of its purchases to maintain appropriate policy accommodation as the outlook for the labor market or inflation changes.

Or reduce? I think this sentence will be gone.

In determining the size, pace, and composition of its asset purchases, the Committee will continue to take appropriate account of the likely efficacy and costs of such purchases as well as the extent of progress toward its economic objectives.

This doesn’t really say much, but it may be gone due to more specific language about QE. While I doubt QE will end soon, the Fed may make it clear that QE will end at some point.

FIFTH PARAGRAPH

To support continued progress toward maximum employment and price stability, the Committee expects that a highly accommodative stance of monetary policy will remain appropriate for a considerable time after the asset purchase program ends and the economic recovery strengthens.

No change here.

In particular, the Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that this exceptionally low range for the federal funds rate will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored.

Same but the inflation language may be updated to reflect more recent data.

In determining how long to maintain a highly accommodative stance of monetary policy, the Committee will also consider other information, including additional measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments.

More boilerplate.

When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent.

Blah.

SIXTH PARAGRAPH

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; William C. Dudley, Vice Chairman; James Bullard; Elizabeth A. Duke; Charles L. Evans; Jerome H. Powell; Sarah Bloom Raskin; Eric S. Rosengren; Jeremy C. Stein; Daniel K. Tarullo; and Janet L. Yellen.Probably the same.

Voting against the action was Esther L. George, who was concerned that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations.

Hmm. This is a wildcard. The inflation expectations argument seems to be a non-starter, but there is the issue of financial distortions caused by prolonged low rates. It’s like putting a magnet near a compass. Bernanke has downplayed this concern before but it will be interesting to see if others on the FOMC are on board. It will be news if there are more than two dissenting votes. Three or more would be very big news.

More to come.

-

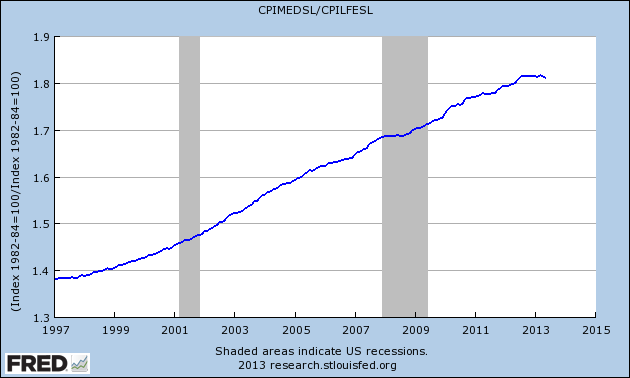

The Most Important Economic Chart in the World

Eddy Elfenbein, June 18th, 2013 at 10:54 amHere’s an update to the Most Important Economic Chart in the World.

The chart below shows the Medical Care portion of the CPI divided by core CPI. Healthcare costs have outrun the cost of everything else for decades. Suddenly, that trend has come to an end. Over the last year, healthcare costs have actually trailed broader consumer prices.

If this trend keeps up, the impact of slower healthcare inflation will have far-reaching effects. Here’s a closer look at the same chart since 2011:

-

FactSet Research Earns $1.15 Per Share

Eddy Elfenbein, June 18th, 2013 at 9:35 amShares of FactSet Research Systems ($FDS) are poised to open about 7% lower today. This morning, the company reported fiscal Q3 earnings of $1.15 per share which matched estimates. Revenue rose 6% to $214.6 million.

“We again delivered double-digit diluted EPS growth and our free cash flow reached an all-time high of $92 million during the third quarter of fiscal 2013. Off-market conditions, especially on the sell-side, continue to interrupt client buying patterns and limited our ASV growth this quarter as expected,” said Philip A. Hadley, Chairman and CEO. “We continue to return capital to shareholders as evidenced by a 13% increase in our dividend and a $200 million expansion to our share repurchase program during the quarter.”

ASV is Annual Subscription Value, and that rose by only $2 million last quarter to $864 million. For Q4, FactSet sees earnings ranging between $1.18 and $1.21 per share. The Street was expecting $1.18 per share. FactSet sees revenues between $218 million and $221 million.

-

Inflation Is Still Low

Eddy Elfenbein, June 18th, 2013 at 8:52 amThe government released the Consumer Price Index report for May, and it showed that inflation is still very low. Headline inflation rose by just 0.15% last month. That’s the seasonally adjusted number, which had actually fallen in March and April. Over the last seven months, seasonally adjusted inflation has risen by an annualized rate of 0.15%. Over the last three months, the annualized rate is -1.6%.

The “core rate,” which excludes food and energy prices, rose by just 0.167% in May. Annualized, that’s almost exactly 2%.

The Fed begins its big two-day meeting today, and this morning’s CPI continues to show that inflation is not a problem. In fact, inflation is running below the Fed’s target. This is why I think fears of the Fed tapering are greatly exaggerated.

-

Morning News: June 18, 2013

Eddy Elfenbein, June 18th, 2013 at 4:56 amYen Drops as Asian Stocks Swing Before Fed; Rubber Slides

Abenomics for Women Undermined by Men Dominating Japan’s Rulers

Directors Refuse to Go Naked for Chinese IPOs

U.S. and Europe to Start Ambitious But Delicate Trade Talks

Homebuilder Confidence in U.S. Rises to a Seven-Year High

Setbacks for Pacts That Delay Sale of Generics

Five Ways The Sprint-Clearwire Drama Might End

Shareholder Says Smithfield Undervalued In Chinese Takeover Bid

Royalty Pharma’s Bid for Elan in Jeopardy

J&J to Buy Aragon Pharmaceuticals for Cancer Candidate

Third Point Raises Sony Stake, Presses For Entertainment Spin-Off

Protests Spreading Across Brazil Are Getting Ugly

JCI Looks To Private Equity To Sell Auto Electronics Unit

John Hempton: Self Assessment Monday: An Old Letter to a Client…

Howard Lindzon: The SnapChat Stock Market, Machines and The SEC

Be sure to follow me on Twitter.

-

Home Builder Index at Seven-Year High

Eddy Elfenbein, June 17th, 2013 at 11:29 amThe stock market is doing well this morning. Tech, energy and financials are leading. The S&P 500 is up to 1,644 which is on track for its highest close this month. Our Buy List just broke the +17% mark for the year, and I see that Medtronic ($MDT) is at a fresh 52-week high. I expect a dividend increase soon from MDT.

The all-important Fed meeting starts tomorrow. The National Association of Home Builders said that their index hit 52 in June. This is the first time it’s been over 50 in seven years.

Also tomorrow, FactSet Research ($FDS) is due to report earnings, and the stock is near a new high.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His