CWS Market Review – May 23, 2023

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

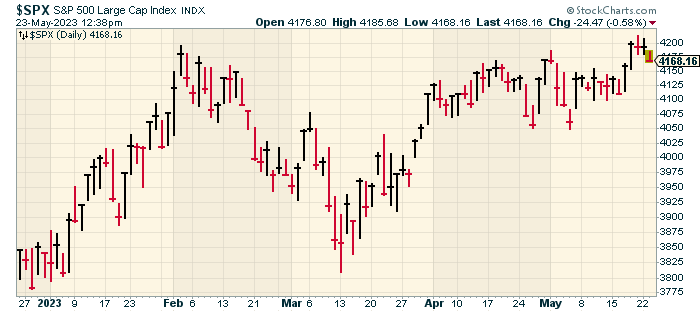

The S&P 500 Briefly Breaks Above 4,200

Wall Street continues to be surprisingly serene. Despite some scary headlines such as the endless debt ceiling debate or a looming recession, stock prices are holding up fairly well.

Last Thursday, the S&P 500 closed at a nine-month high. The index got above that level during the day on Friday and again on Monday but wasn’t able to close at another new high. Today, the market lost a little over 1%.

In this week’s issue, I want to focus on one of the non-traditional ways of looking at the economy which is through corporate earnings reports.

Last week, we discussed Home Depot and its less-than-stellar outlook. This week, we’re going to look at Lowe’s and what that means for the economy. Incidentally, Lowe’s and Home Depot aren’t the only retailers who are offering reduced guidance. Target and Walmart have also cautioned investors over what to expect later this year.

First, though, let’s take a step back and look at the larger picture. The rally that began in October appears to still be going. Measuring for the October low, the S&P 500 is up nearly 20%. That’s a nice run for a few months; however, the index is still far from its all-time high from early last year.

Last year, we talked a lot about bear market rallies. This latest run appears to be something different from the string of head-fakes we got in 2022.

I haven’t written much on the debt ceiling debate because there’s not much to add. I prefer to steer clear of politics, and this is political theater at its most theatrical. Everyone wants to appear tough, principled and uncompromising, but at some point, sensible heads will prevail. There’s too much at risk.

This week, Treasury Secretary Janet Yellen said the U.S. government could default as early as next week. Around Washington, this is being called X-Day. Before, Yellen had said that it’s likely the U.S. government will run out of money. Now she says it’s “highly likely.”

Technically, the government hit the debt limit in January, but it’s been using “extraordinary” measures to keep things going. Secretary Yellen said that due to the volatile nature of tax payments, it’s hard to determine a precise date when we’ll run out of money. The Bipartisan Policy Center said that if Congress doesn’t act, Uncle Sam will go bust sometime between June 2 and June 13. We’ll see.

But what about the stock market? As I said before, the market’s been pretty serene lately. You’d think that if we really were in trouble, the market would be telling us. Another explanation is that the market well understands that this is all for show.

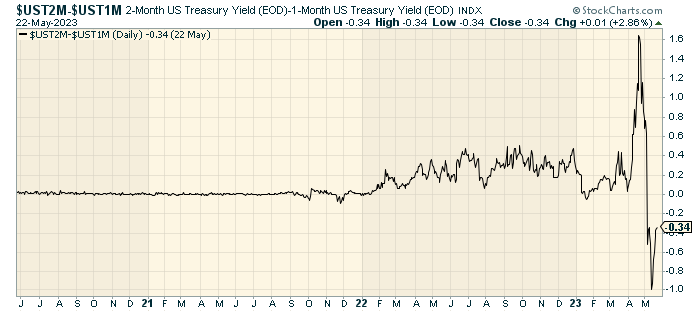

One area where you can see the impact of the debt ceiling debate is on the very short-term yields of the U.S. Treasury market. The yield on the one-month Treasury is currently around 5.7% which is comfortably above the Federal Reserve’s target rate of 5% to 5.25%. This suggests a small risk premium for lenders, especially if you have to miss a debt payment.

The two-month Treasury is much better behaved as its yield is more than 30 basis points less than the one-month Treasury. Again, perhaps the market sees all this quickly passing.

Here’s a chart which really shows you how unusual the short-term Treasury market is right now. This is the spread between the two-month and one-month Treasury bill yields. It looks like a really bad EKG:

You’ll notice that in 2020 and 2021, there was barely any reading on the spread between the two-month and one-month bills. Once the Fed started talking about hiking rates, the spread started to widen.

That makes perfect sense as the spread is like a shorthand way to bet on the Fed raising rates. Still, in 2022, the spread never got very high.

Lately, however, everything’s gotten completely chaotic. The one-month/two-month spread has jumped from negative 100 basis points to positive 150 basis points. This has happened over the course of a few days.

Even if the Fed has to delay a debt payment, I don’t see that lasting very long. That means many Americans won’t be getting paid on their fixed-income investments. That’s a voting block I would not want to upset.

For now, don’t be worried about the debt ceiling debate. The stock market isn’t worried – neither should you be.

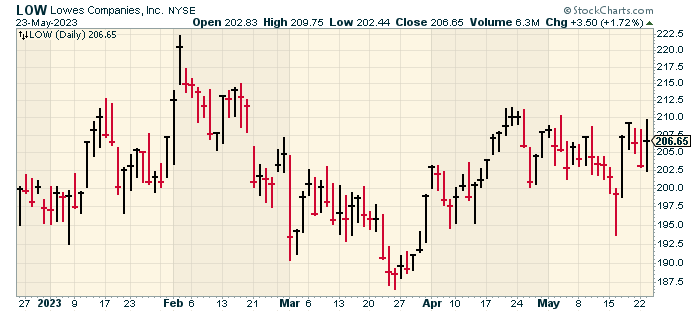

Lowe’s Lowers Guidance

Last week, I told you about the problems at Home Depot (HD). The company posted its worst sales miss in 20 years. As I said, the Home Depot earnings report probably tells us more about the true state of the U.S. than several government reports do.

The same can be said for Lowe’s (LOW), and today we got their earnings report. For its fiscal Q1 (ending in early May), Lowe’s said that it made $3.67 per share. That was above Wall Street’s estimate of $3.44 per share. LOW’s revenue was $22.35 billion which topped estimates by $750 million. Same-store sales fell by 4.3%. That was below Wall Street’s forecast for a decline of 3.4%.

The good news is that shares of LOW closed higher today. This is a good example of a stock closing higher not because of good results but simply because Wall Street was expecting something a lot worse. As always, investing is a game of expectations.

The big takeaway is that Lowe’s lowered its guidance for the rest of this year. The company now sees sales coming in between $87 billion and $89 billion. That’s down from the previous range of $88 billion to $90 billion. Lowe’s sees same-store sales falling by 2% to 4%. The previous forecast was flat to down 2%.

Lowe’s also said that full-year earnings will range between $13.20 and $13.60 per share. That’s down from the previous forecast of $13.60 to $14.00 per share.

That means that Lowe’s is going for about 15.2 to 15.7 times this year’s earnings estimate. That’s not bad, but I would hold off from Lowe’s just yet. Earnings warnings are like cockroaches — for every one you see, there are always a few more hiding.

As an investor, I’m happy to be a little late to a good story. There’s no need in trying to be a hero by investing at the precise low. I don’t mind holding off on picking up a stock like Lowe’s until interest rates start to fall or the company raises guidance. I want to see better news from Lowe’s before I would build a position.

I should add that we got one piece of encouraging news from the housing sector today. The report on new homes sales was better-than-expected. New homes were up 4.1% in April and up 11.8% over the last year. Right now, the inventory of homes is very low.

Update on Previous Stocks

Last month, we looked at Whirlpool (WHR). This is an interesting case because conventionally, Whirlpool appears to be an inexpensive stock. Looks, however, can be deceiving.

Shortly after we profiled Whirlpool, the company released a very strong earnings report. For Q1, Wall Street had been expecting $2.28 per share. Instead, WHR earned $2.66 per share. The company also reaffirmed its guidance for earnings this year of $16 to $18 per share.

Traders hated the report. In two days, WHR lost over 8%.

The story here is that Whirlpool is working to change its entire business. The company has divested its businesses in Africa and the Middle East, but it’s not leaving Europe. Instead, Whirlpool plans to work with Arcelik, a Turkish company, to make a company that’s focused on the European market.

Whirlpool recently closed on a $3 billion acquisition of Emerson Electric’s InSinkErator business. Whirlpool has also been cutting costs. The company expects to save between $800 million and $900 million this year.

Like Lowe’s, Whirpool appears to be cheap. The dividend yield is over 5%, but it all depends on how well the company can transition itself. I’m going to continue to watch Whirpool, but, like Lowe’s, I want to see hard evidence first.

One recent winner, in addition to United States Lime & Minerals (USLM) is Hingham Institution for Savings (HIFS). On May 2, I said it was my favorite regional bank and the stock is up over 10% since then.

This has been a slow period on Wall Street but that may soon change. The Fed minutes are due out tomorrow. On Thursday, we’ll get an update on the Q1 GDP report. Then on Friday, we’ll see the latest PCE price data.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on May 23rd, 2023 at 7:21 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His