CWS Market Review – April 30, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

T.S. Eliot famously wrote that “April is the cruelest month.” Well, this April wasn’t a very kind one for investors. (By the way, Eliot was a Lloyd’s Bank employee.)

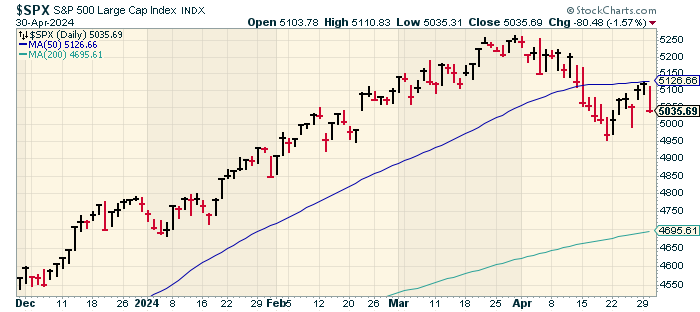

The S&P 500 fell 1.6% today and it was down 4.2% for the month. This snapped the market’s five-month winning streak. The Dow had its worst month since September 2022. In retrospect, we had a charmed market from November through March. It was bound to come to an end.

As it turned out, the S&P 500 reached its closing peak on the final trading day for March, which was the day before Good Friday (Maundy Thursday, to be more precise).

The bulls have clearly been on the defensive this month, and I don’t think the coast is clear just yet. The S&P 500 is still below its 50-day moving average (the blue line). It may soon come up against its 200-day moving average (in green). These aren’t good omens.

Interestingly, defensive sectors like Consumer Staples and Healthcare have started leading the market recently. That comes after an extended period of lagging the market. Defensive sectors typically shine when investors get nervous, and that’s clearly what’s happening. In fact, I wouldn’t be surprised to see defensive sectors start to the lead the market for several months. One of my favorite investing quotes comes from Michael Gayed: “There are no gurus, only cycles.”

It’s true. Consider a boring consumer stock like JM Smucker (SJM). It’s been running against the Magnificent 7 cycle for a long time. The jelly stock is currently going for 11 times next year’s earnings, and the dividend yields 3.7%. Smucker has increased its dividend for the last 26 years in a row. I get it. Smucker isn’t that exciting, but at some point, a company that owns Twinkies and Meow Mix has a certain future.

We’re in the middle of Q1 earnings season. The overall results are improving but this hasn’t been a terribly strong season for Wall Street. Q1 earnings growth is currently tracking at 3.4%. That’s kinda blah.

Shares of Starbucks (SBUX) got dinged after its earnings report fell short of expectations. It’s rare to see SBUX miss.

The only bright spot of this earnings season is that many companies are exceeding their very low expectations. Of the companies that have reported earnings so far, 78.8% have beaten their earnings estimates while 59.6% have beaten on revenue. Slightly more than half (52.7%) have beaten on revenue and earnings.

Financials stocks are providing a big help. Earnings growth for financials is currently running at 7.94%, but that’s up from 3.22% one month ago. Technology is another big winner. Earnings growth for that sector is running at 21.79%.

For Q1, the S&P 500 is expected to earn $54.50 per share. That’s the index-adjusted figure. For all of 2024, the index is expected to earn $240.74 per share. That’s up 9.78% over last year. That translates to a forward P/E Ratio of 21. That’s elevated but not extreme.

The Fed Will Continue to Hold Rates Steady

In addition to all the earnings reports, the Federal Reserve started its two-day meeting today. I’ll spoil the drama for you: the Fed won’t be making any changes to interest rates this meeting. According to the futures market, traders are placing a 99.5% chance that the Fed will leave interest rates alone. That seems low.

It will be interesting to hear what Fed Chairman Jerome Powell has to say about the economy and the path for inflation. I suspect that the Fed wants to cut rates, but the recent data isn’t cooperating. Powell said that the economic numbers have “clearly not given us greater confidence” that inflation is falling back to the Fed’s 2% range.

The conventional wisdom has shifted markedly this year. Not that long ago, it was widely assumed that the Fed would be cutting rates by now. Not only is the Fed not cutting, but it looks like the Fed won’t cut rates until September, and that could be the only rate cut this year. Tomorrow’s policy statement will be released at 2 p.m. ET.

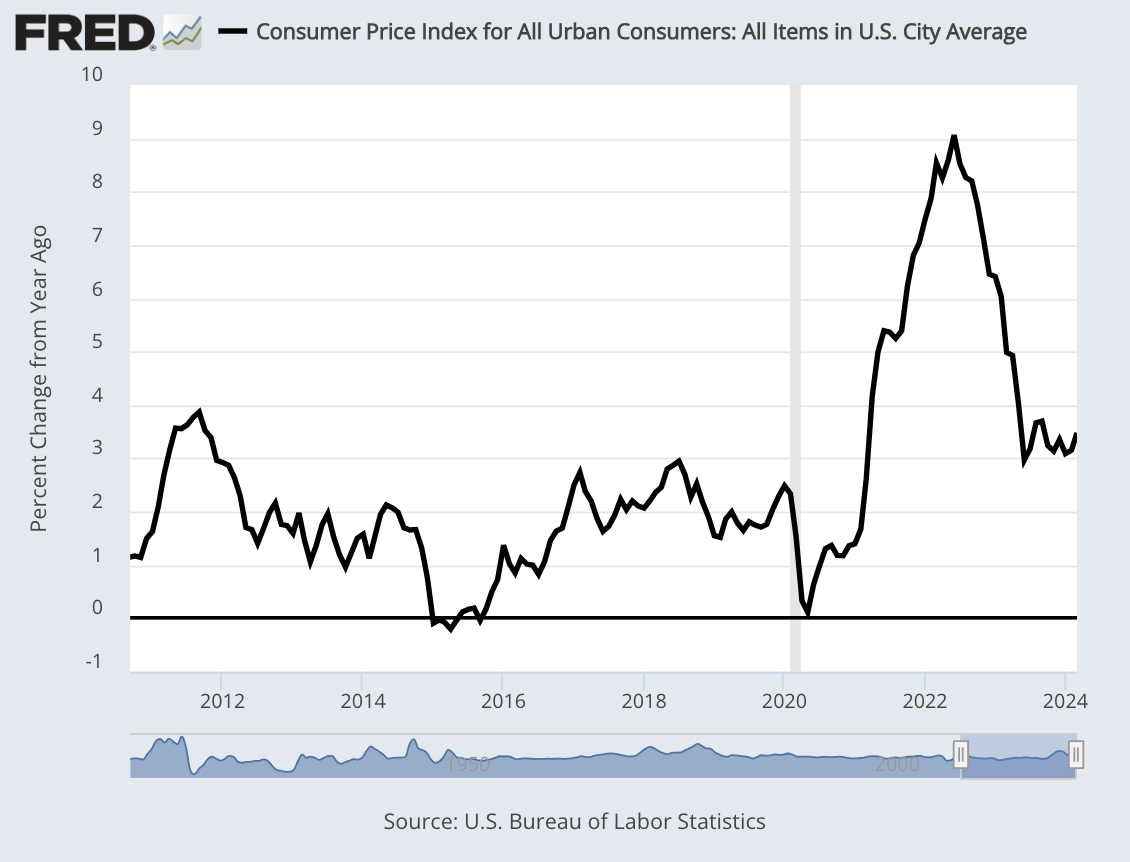

It seems that it was relatively easy to get inflation to fall from 9% to 3% but getting it from 3% to 2% is proving to be quite difficult. In fact, I wouldn’t be surprised if the next move from the Fed is a rate hike.

We’re in an unusual period where the Fed has done nothing to interest rates, but that nothing has reflected a big change in the Fed’s outlook. The Fed has changed from expecting to cut rates soon to a wait-and-see stance.

Indeed, on Friday, we got more evidence that inflation continues to be stubborn. The Commerce Department released its PCE price data for March. This is important because it’s the Fed’s preferred measure of inflation, but the downside is that the data appears much later than the CPI reports.

For March, the PCE price index increased by 0.3%. The core PCE increased by 0.3% as well. Over the last year, the headline PCE price index has increased by 2.7% which was 0.1% above expectations. The core PCE price index increased by 2.8% over last year, and that also was 0.1% above expectations.

The PCE report also showed that personal spending increased by 0.8% in March. Wall Street had been expecting an increase of 0.7%. Personal income increased by 0.5% which matched expectations. The savings rate dropped to 3.2%. That’s down 2% over the last year.

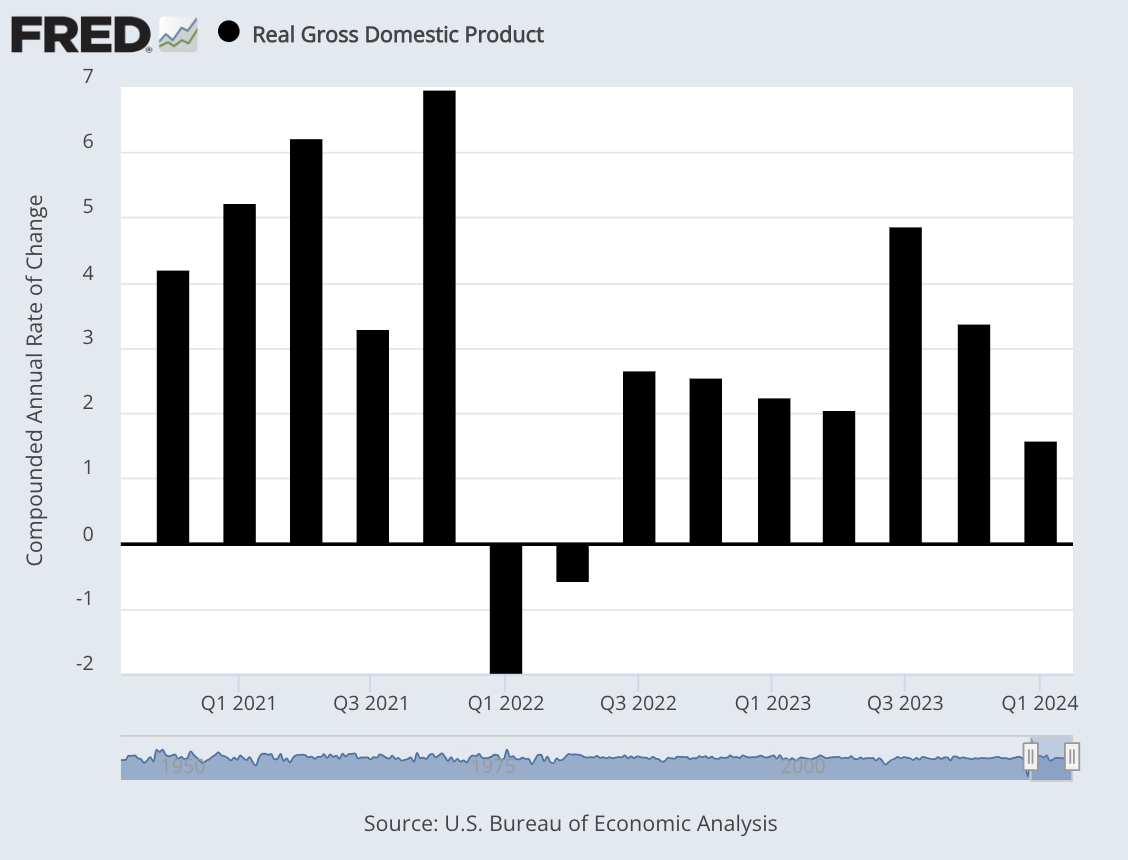

The other major economic report we got recently was last Thursday’s GDP report. That was our first look at Q1 GDP, and it wasn’t very good. For the first three months of this year, the U.S. economy grew at a 1.6% real annualized rate. That was below consensus for 2.4%.

In other words, inflation is running higher than expected and economic growth is lower than expected. It looks as if we’ve entered a period of stagflation.

Within the GDP report, I like to look at the level of consumer spending because that’s the key driver of the economy. For Q1, consumer spending increased by 2.5%. That’s down from the 3.3% rate for Q4. Wall Street had been expecting an increase of 3%. One hopeful sign is that residential investment jumped 13.9% for Q1. That was its largest gain in more than three years.

The next big test for the market comes this Friday with the April jobs report. The consensus on Wall Street is that the U.S. economy added 240,000 net new jobs last month. That’s down from 303,000 jobs added in March (although that number will be revised on Friday). The unemployment rate is expected to remain at 3.8%.

I’ll be paying close attention to the numbers for wages. Those numbers have been getting better, but inflation continues to take a sizeable bite out of so many wage increases. For Friday, Wall Street expects to see a gain in average hourly earnings of 0.3%. For the past 12 months, the expectation is that earnings increased by 4.0%.

Is the regional banking crisis still on? That’s a good question. My tentative answer is “probably not,” but we got a jolt on Friday when the Federales seized Philly-based Republic First Bank (FRBK). This was the first bank failure this year. Republic First is not to be confused with First Republic which went kablooey last year.

Two years ago, the bank was going for about $5 per share. Today it closed at one penny.

It’s important to stress that Republic First Bank was a relative small fry. They had $4 billion of deposits and $6 billion in assets.

It’s actually kind of cool how the FDIC seizes on a busted bank. They’ll shut the bank on a Friday, do a full accounting, then move to sell the bank as soon as possible. They’ll often offer a neighboring bank a sizable discount to take on all the deposits.

The winner this time was Fulton Bank (FULT) of Lancaster, PA. By Saturday, the FDIC got Republic First’s 32 branches to open under the Fulton name. On Monday, shares of Fulton gained 7.5%. This is nowhere close to Silicon Valley Bank or First Republic which had assets of more than $200 billion.

The problem with a banking crisis is that you don’t know what you don’t know. You’ll think Bank A is well protected only to learn that it was heavily exposed to a particular sector of the economy that’s cratering. A bank can be perfectly fine but once investors start demanding their deposits, it can quickly become not so fine.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on April 30th, 2024 at 5:48 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His