CWS Market Review – May 13, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

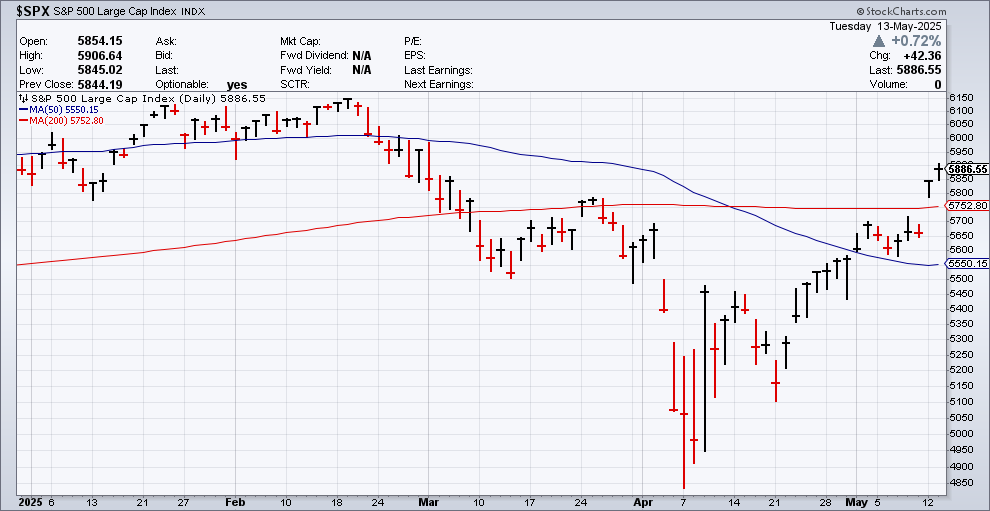

I have great news! The stock market is now flat for the year!

OK, I realize that may not sound that great, but it would have completely shocked, dumbfounded and flabbergasted any investor from three weeks ago. Since April 8, the stock market is up 18%. The S&P 500 is now above its 50- and 200-day moving averages.

Remember how the Great Trade War of 2025 was going to crash the economy and the stock market? Well, it seems those predictions were just a wee bit premature.

Yesterday, the White House and China agreed to defuse a trade war that was getting uglier by the day. President Trump said, “We’re not looking to hurt China.” From the New York Times:

The move by the United States, after President Trump had repeatedly declared that he would not lower tariffs without concessions from China, represented an acknowledgment of the costs of an all-out trade war with China. Despite the White House’s bluster, the Trump administration ultimately backed off, for now, from the steepest tariffs, and agreed to hold more formal talks with Beijing after companies and consumers started showing signs of economic strain.

The stock market took the hint and prices soared.

Yesterday the stock market had its second-best day in the last 2-1/2 years. For the day, the S&P 500 soared 3.26%.

The best market’s best day in the last 2-1/2 years—in fact, one of its best days in decades—came one month ago, on April 9th. It’s still early, but that day may go down as the start of a new bull market.

Here’s where it gets interesting, because both days (yesterday and April 9th) were surprisingly similar. In both cases, the markets rallied on news that the trade war tensions were easing. The S&P 500 is only about 4% from a new all-time high.

It’s as if yesterday’s gain was about one-third that of April 9th’s gain, even by category. Yesterday, the Nasdaq gained 4.35%. The S&P 500 High Beta index gained 5.46% while the S&P 500 Low Volatility Index gained a measly 0.15%. That’s very similar to the kind of action we saw on April 9th, just not as severe.

Many of the high-risk, fast-growth stocks did very well on Monday. For example, the Mag 7 ETF (MAGS) gained 5.8%. On the other hand, many high-yielding stocks like Altria (MO) and Duke Energy (DUK), lost ground. The lesson here is that investors were leaving safe havens and chasing risk.

It’s as if investors had been itching to do this for several week but were just waiting for official permission. Thanks to the president’s decision, they finally got it.

This was also reflected in the bond market where yields rose. The two-year Treasury, which is usually the most sensitive to the Federal Reserve, saw its yield rise ten basis points to 3.98%.

In the futures pits, traders altered their bets as to what the Fed will do. Now it looks like a June rate cut is off the table. In fact, traders don’t see the Fed cutting rates until September. This happened even as we got favorable inflation news today.

Much of the trading action we saw on Monday continued into Tuesday. The S&P 500 gained 0.72% on Tuesday. Again, it was a divided market. For example, the Nasdaq gained 1.61% while the Dow was down 270 points, or -0.64%. The S&P 500 Growth ETF gained 1.67% while the S&P 500 Value ETF lost 0.44%. This shows that investors are rotating out of safer areas in search of bigger returns. I don’t expect this trend to last long.

Inflation Falls to Four-Year Low

This morning, the government said that inflation rose by 0.2% last month. That was in line with Wall Street’s forecast. The inflation report brings the 12-month rate to 2.3% which is a four-year low. I should add that these numbers don’t fully reflect the effects of the trade war.

The core rate also increased by 0.2%. That was 0.1% below expectations. Over the last 12 months, core inflation has increased by 2.8%. The core rate excludes food and energy prices which can be very volatile.

After posting a 2.4% slide in March, energy prices rebounded, with a 0.7% gain. Food saw a 0.1% decline.

Used vehicle prices saw their second straight drop, down 0.5%, while new vehicles were flat. Apparel costs also were off 0.2% though medical care services increased 0.5%. Health insurance increased 0.4% while motor vehicle insurance was up 0.6%.

Interestingly, egg prices fell by 12.7% last month but are still up nearly 50% in the last year. While the inflation numbers are good, the tariff issue could still be a problem for prices. The stock market is clearly pleased that President Trump is willing to back away from his most aggressive stand on tariffs.

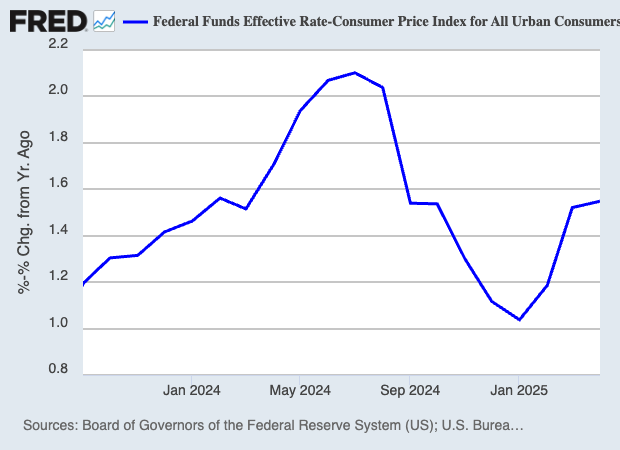

Here’s a look at “real” interest rates, meaning after adjusting for inflation. I used the core rate rather than the headline inflation, which I think presents a more accurate picture.

Many of the trends we saw in Monday’s market continued into today. Tech stocks, for example, did very well. Also, growth stocks outpaced value. This is what to expect if investors see interest rates staying higher for longer.

We recently completed a very good earnings season for our Buy List. Fifteen of our Buy List stocks beat earnings, one missed, and another reported inline.

We’re nearly done with Q1 earnings season so let’s look at where we stand. According to the latest data, 90% of the companies in the S&P 500 have reported results so far. Of those, 78% have beaten on earnings. That’s a little bit better than the long-run average. Companies are reporting earnings that are 8.5% better than expected. That’s also a little better than the long-term average.

Earnings growth is currently tracking an increase of 13.4% over last year’s Q1. That’s pretty good. At the end of March, Wall Street had expected growth of just 7.1%. If that number holds, and I think it will, then Q1 will be the seventh quarter in a row of positive growth and the second in a row of double-digit growth.

For revenues, 62% of companies in the S&P 500 have beaten on sales. That’s not so hot, and it’s below the long-term average. Companies are beating sales by only 0.7%. Revenue growth is currently tracking at 4.8%. If it holds up, then Q1 will be the 18th quarter in a row of revenue growth.

For Q2, Wall Street expects earnings growth of 5.2%, and 9.3% growth for the whole year. The much-predicted recession still hasn’t come.

Amphenol Jumps to New High

One of our Buy List stocks that’s done especially well for us lately is Amphenol (APH). We added the stock to our Buy List last year and it’s up 86% for us in a little over 16 months.

If you’re not familiar with Amphenol, it’s one of the world’s largest makers of fiber optic connectors, antennas, sensors and high-speed cables. Amphenol’s products are used in several different industries such as automotive, broadband communications, commercial aerospace, industrial, IT, data communications, military, mobile devices and mobile networks.

Three weeks ago, Amphenol reported outstanding results for its Q1. The company earned 63 cents per share, which easily topped Wall Street’s estimate of 52 cents per share. Sales were up 48% in U.S. dollars, and up 33% organically.

Amphenol’s operating margin improved to 23.5% and free-cash flow was $580 million. During the quarter, Amphenol bought back 2.7 million shares for $180.9 million and paid out $200 million in dividends. That means that $380 million was returned to shareholders.

For Q2, APH expects sales between $4.9 and $5 billion. That represents sales growth of 36% to 39%. Amphenol also sees Q2 earnings ranging between 64 and 66 cents per share. That represents growth of 45% to 50% over last year’s Q2.

Traders loved the report, as did I. In three days, APH gained 20%. I’m expecting more gains in the months ahead.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on May 13th, 2025 at 7:25 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His