CWS Market Review – September 23, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Normally I’m not in the bubble-calling game, and I’m not going to start now, but I have to concede that the current stock market is getting pricey.

Very pricey. Even Jerome Powell admitted today that “equity prices are fairly highly valued.”

It seems stocks have gone up every day. Over the last 20 trading sessions, the S&P 500 has closed lower only seven times. The market has gone 36 days in a row without a drop of more than 0.7%, which really isn’t a big drop. Since August 1, the market is up more than 6.7%, and since April 8, it’s up over 33%.

Don’t get me wrong — I’ll take it — but I understand that it’s not normal.

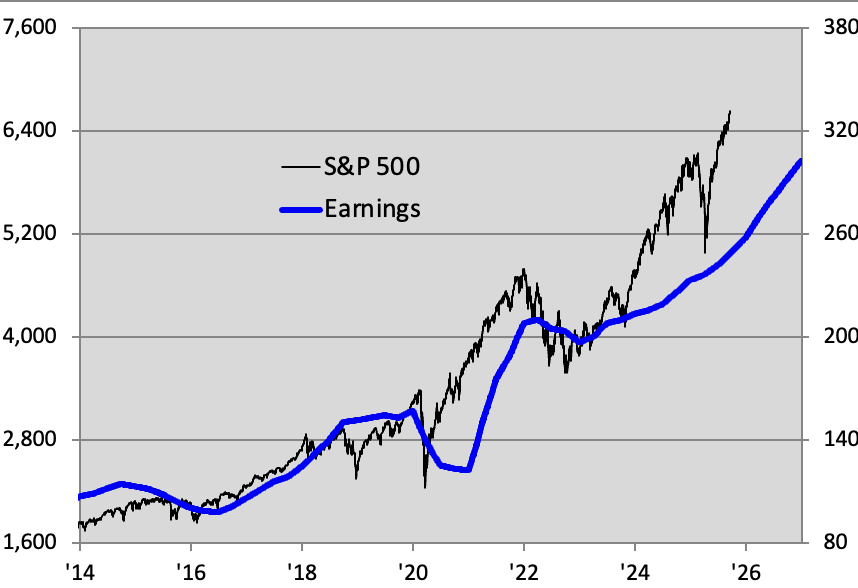

Let’s look at some valuation numbers. The S&P 500 is expected to have earnings this year of $258.30 per share, and $302.90 per share for 2026. (Those are index-adjusted numbers.) That means the market is going for 25.9 times this year’s earnings, and 22.0 times next year’s earnings. That’s quite high.

Tobias Carlisle points out that the forward P/E of the S&P 400 Mid-Cap is at 16.2 and the S&P 600 Small-Cap is at 15.9, which is right in line with their long-term averages.

Not only are stocks up, but gold is at a new all-time high. In fact, gold has finally surpassed its 1980 peak adjusted for inflation. There’s nothing gold loves more than lower real interest rates, and that’s what it’s going to get. And if Jerome Powell is to be believed, then more rate cuts are coming (more on that in a bit).

In a roaring bull market, the best move is to sit back and let it run. One of my favorite Peter Lynch quotes is, “Far more money has been lost by investors trying to anticipate corrections than lost in the corrections themselves.”

Here’s a chart of the S&P 500 (in black) along with its earnings (in blue). I scaled the two lines at a ratio of 20 to 1. That means whenever the lines cross, the S&P 500’s P/E Ratio is exactly 20.

But there’s a key difference with the current rally. As I’ve stressed many times, it’s not so much that the entire market is going higher, but it’s the kinds of stocks that are rallying.

Lately, that’s been the High Beta sector. In fact, ever since I’ve been highlighting the tremendous outperformance of High Beta, the market has only grown more lopsided.

Over the last 23 trading sessions, High Beta has beaten Low Vol 17 times. Since Augst 21, High Beta has gained 10.2% while Low Vol is -2.7%. Over the last five months, High Beta is up about 50% while Low Vol is flat. Sure, Wall Street is having a party, but it has a very exclusive guest list.

The big market news today was that Fed Chairman Jerome Powell gave a speech at the Greater Providence Chamber of Commerce luncheon in Warwick, Rhode Island.

This was a chance for Powell to explain what the Fed has been doing and why. I often make fun of “Fedspeak” because it’s unnecessarily complex and filled with useless jargon.

I’m glad to say that Powell was more plain spoken today. In his remarks, Powell noted that the economy has slowed down, and unemployment has edged up. He also said that inflation has ticked higher and remains “somewhat elevated.” Powell said that at the FOMC’s last meeting, it was time to move policy closer to neutral. In other words, it was time to cut rates.

Powell said:

GDP rose at a pace of around one and a half percent in the first half of the year, down from 2.5 percent growth last year. The moderation in growth largely reflects a slowdown in consumer spending. Activity in the housing sector remains weak, but business investment in equipment and intangibles has picked up from last year’s pace. As noted in the September Beige Book, a report that gathers qualitative information from across the Fed System, businesses continue to say that uncertainty is weighing on their outlook. Measures of consumer and business sentiment declined sharply in the spring; they have since moved up but remain low relative to the start of the year.

That’s a pretty good summary. The question mark is the labor market. There’s been a drop off in both the supply and demand for workers (i.e., immigration) which, in Powell’s words, has made for an “unusual and challenging development.”

Payroll job gains slowed sharply over the summer months, as employers added an average of just 29,000 per month over the past three months. The recent pace of job creation appears to be running below the “breakeven” rate needed to hold the unemployment rate constant. But a number of other labor market indicators remain broadly stable. For example, the ratio of job openings to unemployment remains near 1. And multiple measures of job openings have been moving roughly sideways, as have initial claims for unemployment insurance.

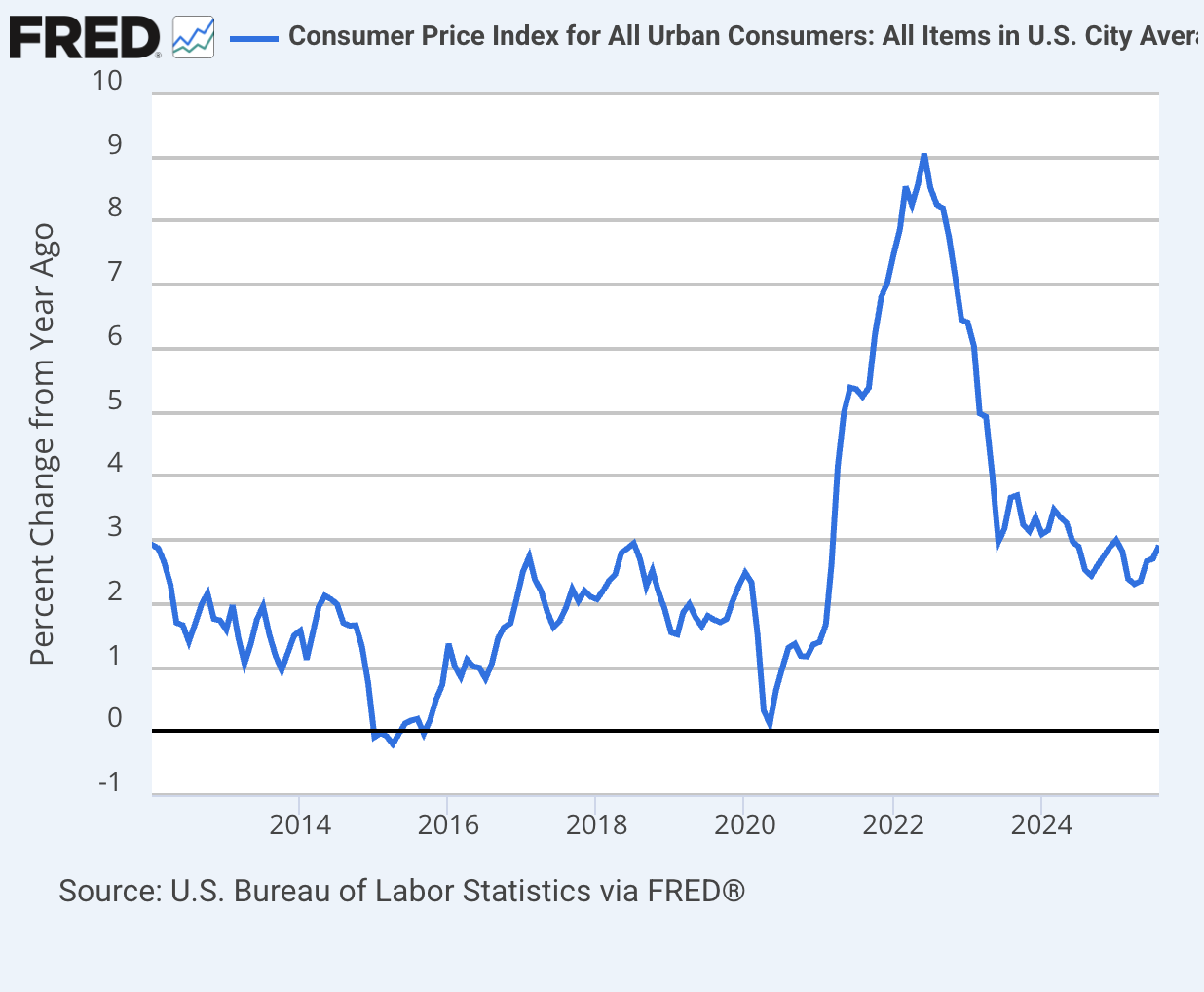

Powell said that since 2022, the Fed has made significant gains with inflation but it’s still above the Fed’s target for 2%. Over the last year, the core PCE is running at 2.9%.

What’s behind the recent increase in inflation? It appears that prices for goods are the chief culprit. This comes after goods prices fell much of last year. Also, the available evidence suggests that tariffs are causing the higher prices rather than broader pricing pressures.

For services, the rate of inflation has been falling, and it looks to continue to fall. (Mind you, this is the rate of increase that’s falling.) Powell said that beyond the next year, most inflation points toward the Fed’s 2% goal.

There’s also the issue of the tariffs. Powell said that the best-case scenario will be a one-time shift in prices. Powell stressed that “one-time” doesn’t means “all at once.” It’s simply a matter of time. Tariffs will have to work their way through supply chains. That means the one-time may even take several quarters.

Personally, I’m baffled by the Fed’s strong commitment to 2% inflation. There’s nothing magical about it. As an investor, the important thing is that they got inflation down from 9% to 2.9%. Getting the extra 0.9% doesn’t seem like that big a deal, especially if it means hurting an already damaged labor market.

Powell said that with the dual threat of fewer jobs and higher prices, there’s no risk-free path. There’s a danger of moving too aggressively, and there’s danger if they stand still for too long. One detail that caught my eye is that Powell said that he still sees the current policy as “modestly restrictive.” In other words, he’s opening the door for more rate cuts.

Wall Street currently expects another interest-rate cut at the Fed’s next meeting in October, and another cut in December. After that, traders see three more cuts in 2026.

On Monday, new Federal Reserve Governor Stephen Miran made the case for aggressively lower interest rates. The current target range for the Fed funds rate is 4.0% to 4.25%. Miran thinks it should be in the low 2% area.

In the Summary of Economic Projections, Miran wants to cut rates by 1.25% this year. Miran was the sole dissenting voice at last week’s FOMC meeting.

Miran makes an interesting case. Miran believes that “changes in tax and immigration policy along with easing rental costs, deregulation and incoming revenue for tariffs” are changing the economic landscape and as a result will allow for much lower interest rates.

Miran contends that the “neutral interest rate” has fallen. By neutral rate, we mean the level at which the Fed is neither pushing nor pulling. The problem with the neutral rate is that we never know exactly where it is. It’s a big guessing game. Right now, the Fed thinks the neutral rate is around 1% to 2%, but Miran thinks it’s near 0%.

Miran’s term is a short one. It ends in January. Later this year, he could return to the Fed as its new chairman.

There are a few important economic reports coming this week. On Thursday, we’re going to get reports for durable goods and existing home sales. Also on Thursday, the government will update its report on Q2 GDP growth.

Of course, Q2 is starting to be far away from us. It started six months ago and ended three months ago. Still, the GDP report is a biggie. The last report said that the U.S. economy grew at a real annualized rate of 3.3% during Q2. That’s quite good.

But what about Q3? Wall Street is starting to parse the numbers for this report. The Atlanta Fed’s GDPNow model currently pegs Q3 GDP growth at 3.3%. If that’s right, it would be back-to-back quarters of 3.3% growth.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on September 23rd, 2025 at 10:08 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- August 2026

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His