CWS Market Review – September 30, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The third quarter of 2025 comes to an end today and it was another good one for Wall Street. For Q3, the S&P 500 gained 7.79%, and if we include dividends, then the S&P 500 was up 8.12%. With three months to go, the stock market is on track for another winning year (+13.72% or +14.83% with divs). This was the market’s second-best September of the last 27 years.

What’s remarkable is that the stock market has rallied despite all the scary pitfalls that we were told would certainly derail the bull market (wars, tariffs, the Fed).

The latest worry is that a potential government shutdown will sink the market. At midnight tonight, the money runs out. I won’t get into the politics of the shutdown, but the major sticking point is money for enhanced Affordable Care Act subsidies.

I will say that previous government shutdowns (there have been several) haven’t hurt the stock market. Economists generally believe that any short-term damage from a shutdown can quickly be rectified.

On Monday, there was a last-ditch effort to stave off a shutdown but that went nowhere, as expected. The Senate plans one more vote before Zero Hour but that also appears to have little chance of passing.

Asked if there’s any room for negotiations on Obamacare subsidies by Tuesday’s midnight shutdown deadline, Republican Sen. John Kennedy said, “Not unless Chuck stops smoking wizard weed.”

The condensed version of the story is that the Republicans are blaming the Democrats, and the Democrats believe the exact opposite.

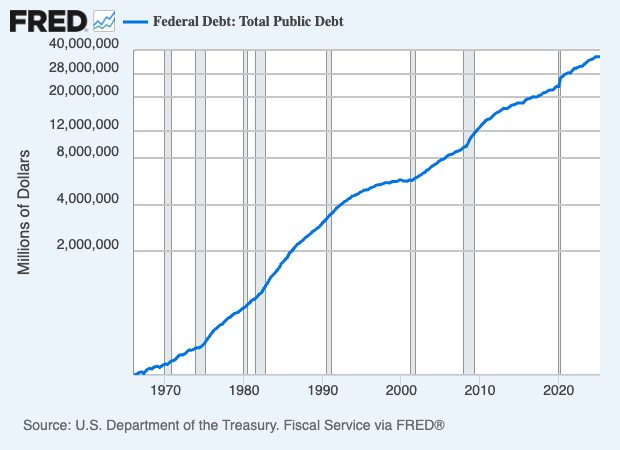

Our fiscal issues are indeed very large, and there’s no easy fix. Fiscal 2025 also comes to an end tonight, and it looks like the deficit will be about $2 trillion. When I say “about,” I’m speaking of a range of hundreds of billions of dollars.

More than half the federal deficit racked up over the last 230 years has come about since 2020. Over the last 11 months (ending in August), the IRS has collected 6% more taxes than the same period last year.

The White House budget office has threatened mass firings if there is a shutdown.

The move by Senate Majority Leader John Thune is intended to maximize pressure on his counterpart, Senate Minority Leader Chuck Schumer, who has so far blocked a plan for a status-quo funding bill without commitments to extend the Obamacare subsidies. Schumer, for his part, said the outcome is up to Trump and his GOP leaders.

“It’s now in the president’s hands. He can avoid a shutdown if he gets the Republican leader to go along with what we want,” Schumer said Monday night, hours after Congress’ top four party leaders met with Trump for a last-ditch meeting at the White House.

I’m definitely not the person who will add any insight to this political standoff. I’m only interested in any possible economic or financial outcomes, and there are several.

For one, when the money gets tight, the government can furlough workers. During the 2018-19 standoff, 340,000 employees were furloughed. Although at that time, the government had passed some bills to keep parts of the government working. Not this time. Some estimates say that furloughs could be as high as 800,000. Salaries for government employees could also be delayed which would have a further impact on consumer spending.

Another outcome of a government shutdown would be a delay of important economic data. That would include the September jobs report which is due out on Friday. The inflation report may also be delayed.

Wall Street expects Friday’s jobs report to show a gain of 51,000 net new jobs last month. Economists also expect to see a 0.3% increase in wages and it expects the unemployment rate to stay at 4.3%. I’d really like to see those wage numbers improve. Consumer spending is the main driver of the U.S. economy.

Tomorrow we’ll get the ADP report on private payrolls. That report won’t be delayed since it’s from a private company. I’ll caution you that the ADP report is a very imperfect bellwether of the BLS’s report. Also tomorrow, we’ll get the ISM Manufacturing Index for August. I like this report since it’s a survey, and we get it with very little lag time.

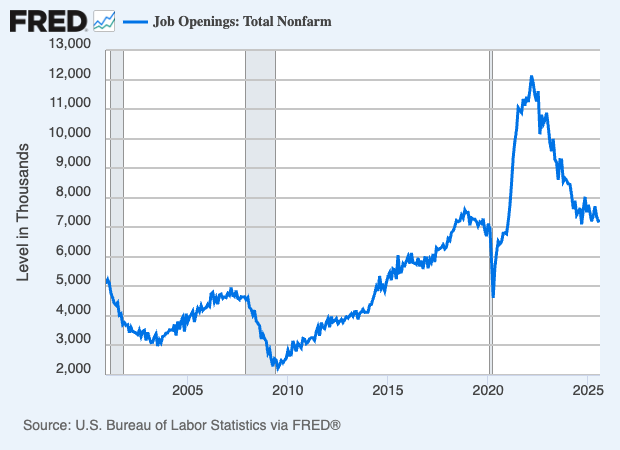

We got the August job openings report today, which is officially called the Job Openings and Labor Turnover Survey, or JOLTS report. It showed that jobs openings increased a little bit in August. Job openings rose by 19,000 to 7.227 million. Economists had been expecting 7.185 million.

Hiring decreased by 114,000 to 5.126 million, and layoffs fell by 62,000 to 1.725 million.

This is further evidence that the labor market isn’t completely healthy. Exxon said today that it plans to cut 2,000 jobs, which is 3% to 4% of its workforce. Over the last three months, job gains have averaged 29,000 per month. That’s down from 82,000 over the same period last year. We’re at an odd point because the demand and supply for labor are falling. It would be nice to have more data.

If the government shuts down, economic data from the Federal Reserve would continue since the Fed isn’t funded by the government. The weekly jobless claims report also won’t be impacted since it’s collected at the state level, but I am concerned about the jobs report and the CPI report.

RIP: Larry Mendelson

We had some sad news this week. HEICO said that its long-time CEO Larry Mendelson died. In the 1950s, he took a finance class taught by David Dodd. Fans of value investing will recognize Dodd’s name. He was the co-author of Security Analysis with Ben Graham. Security Analysis is probably the foundational text of value investing.

Mendelson took those lessons to heart. He made a good deal of money in real estate and wanted to diversify his holdings. That led him to invest in an under-performing industrial company. He really didn’t care what he bought, as long as it was cheap and had potential to be retooled for future growth. He chose well.

Since 1995, the stock has increased more than 1,000-fold.

HEICO was originally founded in 1957 by Dr. William Heinicke as Heinicke Electronics. By the 1980s, Mendelson controlled a sizeable share in the company and was able to make himself CEO. The family still owns a large chunk of the voting shares, and several family members hold key positions within the company.

HEICO makes replacement parts for the airline industry. If a commercial aircraft needs some obscure new part, the airline can’t run down to the local hardware store. Instead, it needs to special-order it. Moreover, there’s a great deal of cost pressure on the airlines to keep the older planes serviceable.

Also, the aircraft parts often need to meet strict regulatory guidelines. The part maker really has to know what it’s doing. That’s where HEICO comes in. The business is lean and well run.

When airplane owners need a new part and go back to the original equipment manufacturer (OEM) to get replacements, they’re often charged a steep price. The profit margins can exceed 30%. That provides enormous opportunity for HEICO. Consider that many aircraft are over 20 years old.

The aviation industry is broadly diversified, and HEICO is also able to get sales from commercial and military customers. That means that if there’s a drop-off on one end of the business, the other side can pick up the slack. Wherever there’s a demand to cut costs, HEICO has the potential to do well.

HEICO’s role is like that of a generic drugmaker. HEICO provides a low-cost copy of the original product, which is regulated by the Federal Aviation Administration. HEICO does more than aircraft parts. They also supply parts for satellites, rockets, missiles and even medical instruments.

HEICO is in an enviable position and nearly dominates its market. The company sells to 19 of the top 20 airlines in the world, and their customers love them.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on September 30th, 2025 at 6:24 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His