CWS Market Review – November 25, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Federal Reserve meets again on December 10. Until very recently, it was looking like the Fed was ready to skip raising interest rates. That’s what the many Fed watchers and the futures market were thinking.

Then it all changed.

On Friday, John Williams, the top banana at the New York Fed, said the central bank should consider lowering rates at this upcoming meeting. This is a big deal because Williams is seen as being close to Chairman Jerome Powell. Also, the President of the FRBNY is the first among equals inside the Fed.

Now it looks like another Fed rate cut is ready to go.

What caused the change in sentiment? Williams said that he’s concerned about a weakening jobs market, and I have to agree with him. He’s also worried that any inflation from the tariffs could be persistent. The conventional wisdom appears to be that any inflation via tariffs will be transitory. I’m not so sure about that.

“My assessment is that the downside risks to employment have increased as the labor market has cooled, while the upside risks to inflation have lessened somewhat,” he said at an event in Santiago, Chile. “Underlying inflation continues to trend downward, absent any evidence of second-round effects emanating from tariffs.”

Mr. Williams affirmed that he still believes interest rates, which are in a range of 3.75 percent to 4 percent, are still “restrictive,” meaning they are weighing on economic activity. After two quarter-point cuts at the September and October meetings, the degree of restraint had lessened, but he said he still believed the Fed had room to reduce interest rates further to get to a “neutral” stance that neither revs up nor slows down growth.

“I still see room for a further adjustment in the near term to the target range for the federal funds rate to move the stance of policy closer to the range of neutral,” he said.

At last look, traders see the odds of the Fed cutting again at near 85%. One week ago, the odds were at 42%. Whatever happens, I think there’s a good chance we’ll see a few dissents at the upcoming meeting. Under Powell, dissents have been rare.

Christopher Waller and Stephen Miran are clearly on the rate-cutting side of the debate. Miran, in fact, favorited cutting by 50 basis points at the last two meetings. There’s a good chance that Waller could replace Jerome Powell as Fed chair when the latter’s term is up in May. However, the conventional wisdom is that Kevin Hassett is President Trump’s top choice to lead the Fed.

Yesterday, the market responded with a nice, happy rally. As you might expect, all those High Beta names were in rally mode. Google and Tesla were both up by more than 6% and Broadcom closed higher by 11%.

The Nasdaq Composite was up more than 2.7% on Monday. The High Beta ETF was up more than 2.0% while the Low Vol ETF closed down 0.3%. In other words, the market sees lower rates as an excuse to party. I’m not so sure that’s the right take.

The fact is that there are a lot of reasons to be concerned about the state of the economy. Unfortunately, the government shutdown left us without recent economic data. Still, many signs are pointing to a slowdown.

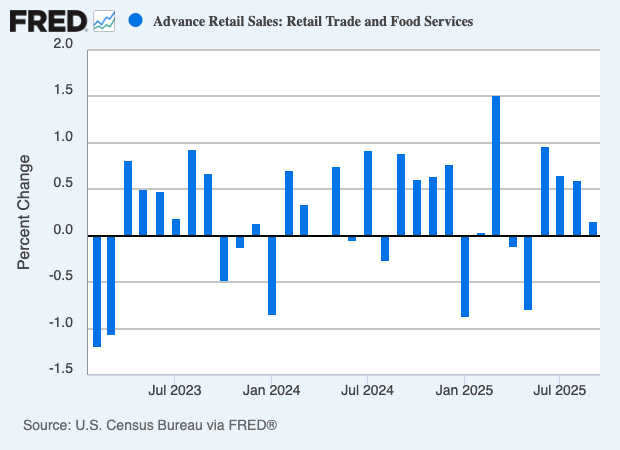

On Tuesday, the Census Bureau said that retail sales rose by 0.2% in September. That was 0.1% less than forecast. But if we don’t include auto sales, the retail sales were up 0.3% which was in line with estimates.

Miscellaneous retailers saw a 2.9% increase on the month, while gas stations, owing to the higher prices, increased 2%. Sporting goods, hobby and music stores saw a 2.5% decline while online sales were off 0.7%.

Sales at eating and drinking establishments, an indicator of discretionary spending, increased a solid 0.7% on the month and were up 6.7% from a year ago.

Retail sales, which are adjusted for seasonality but not inflation, increased 4.3% from a year ago, ahead of the 3% CPI rate for the month.

We also learned that consumer confidence fell to its lowest point since April. The percentage of workers saying that jobs are “plentiful” fell to 6%. That’s down from 28.6% in October.

Home sellers are taking their houses off the market at the fastest pace in nearly a decade. Nearly 85,000 sellers took their homes off the market in September. That’s up 28% from last year.

We still have the problem of missing economic data. Unfortunately, that will take a few more weeks to fix. The next jobs report is due out on Tuesday, December 16. The CPI report will be out on Thursday, December 18 and the GDP report will be out on December 23.

Going into Tuesday, the market was able to extend its rally. The Dow closed up more than 660 points. The S&P 500 closed above its 50-day moving average. The rally was also broader as the S&P 500 Equal-Weighted Index closed higher by 1.45%.

The Healthcare and Consumer Discretionary sectors were especially strong today. Many of the more conservative stocks on our Buy List did well on Tuesday. For example, Mueller Industries (MLI), Cencora (COR) and Rollins (ROL) all made new 52-week highs today.

IES Holdings Soars 8.5%

In last week’s issue, I told you about IES Holdings (IESC). The company is an electrical contractor that provides design, build and maintenance services. The division offers service capabilities including constant presence, critical plant shutdown, troubleshooting, emergency service, testing, and preventive maintenance.

The stock has more than doubled for us this year.

IESC currently has a market value of $7.2 billion and about 9,400 employees. The company currently operates through four business segments: Electrical, Communications, Infrastructure and Residential.

Last Friday, IESC reported outstanding results for its fiscal Q4, and the shares rallied 8.5% on Monday. Revenue rose 16% to $898 million. Operating income was up 39% to $104.3 million, and diluted adjusted EPS was $3.77 compared with $2.61 one year ago.

For the whole year, IESC made $23.66 per share. That’s up from $9.56 per share last year. The outlook is bright for IESC. At the end of the quarter, the company had a backlog of $2.7 billion.

CEO Matt Simmes said, “Looking forward to fiscal 2026, we expect continued growth in our Communications, Infrastructure Solutions and Commercial & Industrial operating segments, which are positioned to benefit from continued strong demand, particularly in our data center end market.”

I’ll have more to say on IESC in our premium letter (you can subscribe here). If you’re not familiar with IES Industries, you can read the latest investor presentation here.

That’s all for now. The government’s econ reports may be out soon. Until then, several Fed officials will be speaking this week. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. This got me a lot of hate but I was right.

— Eddy Elfenbein (@EddyElfenbein) November 20, 2025

Posted by Eddy Elfenbein on November 25th, 2025 at 7:04 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His