CWS Market Review – December 16, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Circle your calendars for Friday, December 26. That’s when I’ll send you the Buy List portfolio changes for 2026.

As usual, I’ll add five new names to the Buy List, and I’ll delete five current ones. The Buy List stays at 25 stocks. The new Buy List goes into effect on January 2 which will be the first day of trading of the new year.

Once the changes are made, the Buy List is locked and sealed, and I can’t make any changes for the next 12 months. I like to release the portfolio changes a few days early just in case someone claims I’m somehow manipulating the numbers.

Our Buy List has been live on the Internet every hour of every day for the last 20 years. Thanks to everyone who’s been a supporter of high-quality, low-turnover investing.

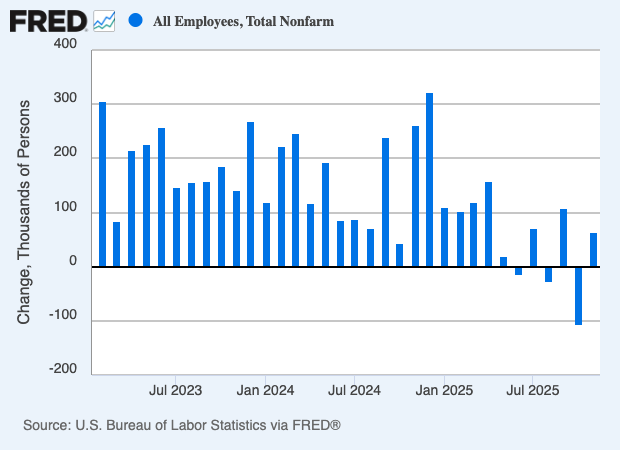

Now let’s look at our long-delayed jobs report. This morning, the Labor Department finally released the jobs report. The good news is that last month, the U.S. economy gained 64,000 jobs which topped Wall Street’s forecast of a gain of 45,000.

Here’s a look at nonfarm payrolls:

The bad news is that the unemployment rate rose to 4.6% which is the highest in four years. This appears to be more evidence of the “low hire, low fire” jobs market.

The real surprise is that in October, the economy shed 105,000 jobs. For September, there was a surprise increase of 108,000. The broader U-6 rate increased to 8.7% which is the highest since August 2021.

The government shutdown heavily impacted the numbers, and the effect may continue for a few months. During October, the number of government jobs fell by 162,000. During November, it continued to fall by 6,000.

The report also had revisions to previous months. For example, the jobs total for August was revised downward by 22,000 to show a loss of 26,000. For September, the number of jobs was revised lower by 11,000.

Here’s a look at some of the details from the report:

The establishment numbers showed most of the gains in November came from a familiar source — health care added 46,000 jobs, accounting for more than 70% of the total net increase. Construction rose by 28,000, while social assistance contributed 18,000.

On the downside, transportation and warehousing was off 18,000, part of a continuing trend in job losses for the sector. Leisure and hospitality also posted a loss of 12,000.

“The U.S. economy is in a jobs recession,” said Heather Long, chief economist at Navy Federal Credit Union. “The nation has added a mere 100,000 in the past six months. The bulk of those jobs were in healthcare, an industry that is almost always hiring due to America’s aging population.”

If I had to guess, I don’t think today’s release will have much sway over the Federal Reserve. However, the next jobs report, due to come out in early January, could be very important to the Fed.

After lowering interest rates at the last three meetings, the Fed will probably take a rest at the January meeting. Traders currently think there’s only a 24% chance that the Fed will cut rates again next month. After that, traders see two 0.25% cuts coming next year.

The other key input in this equation is average hourly earnings. Last month, average hourly earnings rose by only 0.1%. Frankly, that’s pretty weak. Wall Street had been expecting a gain of 0.3%. Over the last year, average hourly earnings were up by 3.5%. That’s the slowest annual gain in four years. If inflation is a problem, then I doubt it’s coming from the labor market.

According to the data, household employment increased by 407,000 over the last two months. At the same time, the labor force increased by 323,000. The labor force participation rate increased to 62.5%.

We also got the retail sales report. For September, retail sales were flat. Wall Street had been expecting a gain of 0.1%. If we don’t count autos, then retail increased by 0.4%. That beat Wall Street’s estimates of 0.2%.

In other economic news Tuesday, the Commerce Department reported that retail sales were flat in September, against a forecast for a 0.1% increase, according to numbers adjusted for seasonality but not inflation. Excluding autos, however, sales increased 0.4% which doubled Wall Street’s estimate of 0.2%.

Last Wednesday, the Fed voted to cut interest rates and the stock market rallied. The S&P 500 rallied again on Thursday to reach a new all-time high. It was the first time the index closed above 6,900. Since the market’s low in April, the S&P 500 has added nearly 40%.

What’s important to understand is that the nature of the rally has gradually changed. Before, only a small group of stocks were doing the heavy lifting. Now, more stocks are joining in.

For example, since late October, financial stocks have been leading the market. That sector hasn’t done much of anything for the last 15 years. Healthcare stocks have been a train wreck for the last three years, but now they’re showing some strength.

Consumer staples have also edged up some in recent weeks. Industrial stocks have been gaining as well. In fact, the Dow Jones Industrials are outpacing the S&P 500. For the seven years prior to September, the Dow badly lagged the S&P 500.

The stock market has fallen for the last three days in a row. Today the index briefly fell below its 50-day moving average.

What’s happening is that Wall Street has adopted a more conservative outlook. That means that some of the boring sectors are suddenly in favor again. Since late October, the S&P 500 has been basically flat, but the S&P 500 Tech Index has fallen by more than 5%.

This trend is an outcome of lower interest rates from the Fed. As rates drop, investors desire stable stocks with stable dividends.

Last week, Abbott Labs (ABT), one of our Buy List stocks, announced that it’s raising its quarterly dividend from 59 to 63 cents per share. That’s an increase of 6.8%. What makes this notable is that this is the 54th year in a row that Abbott has increased its dividend. There aren’t many stocks with a streak like that. Abbott has been on our Buy List for the last five years.

Too many investors tend to overlook dividends, but they’re a key part of long-term investing success. Since 2020, Abbott has increased its dividend by 70%. The new dividend is payable on February 13 to shareholders of record on January 15.

Abbott is also a good example of the kind of stock that’s been leading the market in recent days (+5% to -1%).

Here’s a 42-year chart of Abbott Labs with its dividends reinvested (black) and without dividends (blue). Those little payments really do add up.

That’s all for now. The CPI report is due out tomorrow. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on December 16th, 2025 at 5:54 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His