CWS Market Review – January 6, 2026

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

I always look forward to the start of the new trading year. It’s a fresh start and all the YTD performance numbers are set back to zero. It’s a time to leave behind last year’s mistakes and look ahead to profits in the new year.

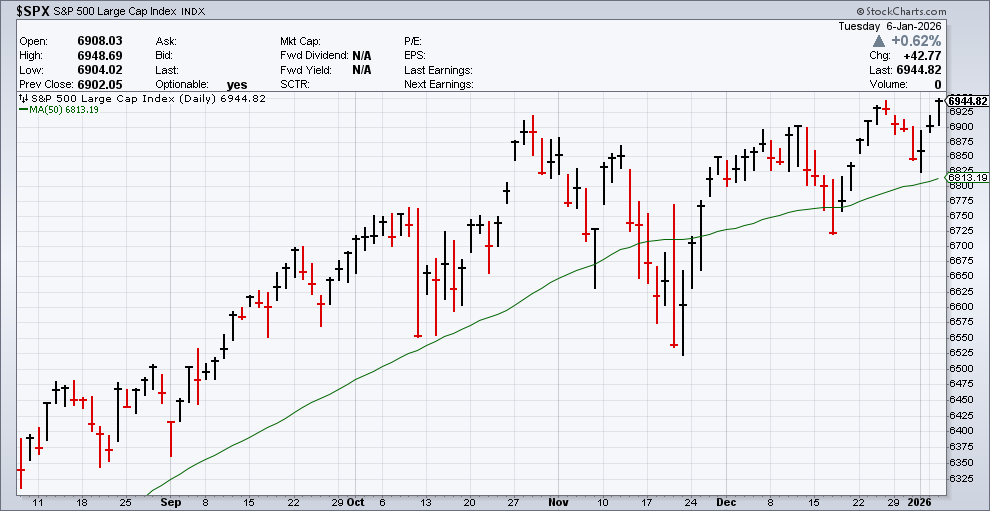

So far, the stock market seems to be in a very happy mood in 2026. The S&P 500 rallied on the first three trading days of the new year, and today the index set a new all-time record closing high of 6,945.82. Before today, the last closing high was set on Christmas Eve.

Not only did the market rally on the first three days of this year, but our Buy List outperformed the market on all three days as well.

The events in Venezuela haven’t been enough to rattle the markets. Indeed, one of our buy List stocks, SAIC, the defense contractor, got a nice lift on the news. It’s already up 8% for us this year. We also had new highs today from stocks like Heico and Thermo Fisher.

Historically, this has been a good time of year for the stock market. From December 20 to February 18, the S&P 500 has gained an average of 3.6%. That’s close to one-third of the market’s annual gain coming in less than one-sixth the time.

Another of our new stocks on the Buy List, Comfort Systems USA, is already up 10.8% this year. Not bad for three days, but we know not to celebrate too soon. The market can and will change its mind very quickly.

The market news has been fairly quiet recently, but that will soon change. Now that the government shutdown is over, we can get back to regular economic reports. This Friday, the government will release its jobs report for December, although the last few labor reports were not very encouraging.

The simple fact is that the labor market has been slowing down. The unemployment rate is currently at a four-year high, even though it’s still at a historically low level. The unemployment rate reached its low point nearly three years ago.

Earlier today, we got the ISM Manufacturing Index for December, and it showed that U.S. manufacturing fell to a 14-month low. The Index fell to 47.9 for December. That’s the lowest level since October 2024. Manufacturing now makes up 10% of the U.S. economy.

The other big news headed our way will be the start of the Q4 earnings season. As usual, many of the big banks will go first. JPMorgan Chase and the Bank of New York Mellon are set to report on Tuesday, January 13. JPM often sets the tone for the entire banking sector.

By the way, JPM’s CEO Jamie Dimon made a cool $770 million last year. That works out to 28 cents per share on a $330 stock. I’m not smart enough to tell you if that’s too high or too low, but the stock gained 34% last year. JPM’s annual profit will probably come in around $20 per share.

On Wednesday, we’ll get earnings reports from Bank of America, Citigroup, and Wells Fargo. The financial sector has been unusually strong lately, and I say that cautiously. Except for a few bursts, finance stocks haven’t been popular in several years. Since late October, the S&P 500 Financial ETF is up by more than 8% while the S&P 500 ETF is up less than 1%.

Our first batch of Buy List earnings reports probably won’t be until the third week of January. Companies often need a little more time to compile their Q4 reports. That’s why the Q4 earnings season tends to be more spread out compared with the other quarters.

Tomorrow, we’ll get an early look at the jobs report when ADP releases its private payrolls report. Wall Street expects a gain of 48,000. Also on Wednesday, we’ll get reports on job openings and factory orders. Job openings have fallen over the last three years, but the losses may have stabilized. We’ll know more soon.

On Thursday, we’ll get initial jobless claims plus reports on productivity and the trade deficit. The big jobs report is on Friday. Wall Street expects to see a gain of 73,000 jobs which is pretty good. Expectations are for the unemployment rate to fall by 0.1% to 4.5%.

I’m also paying close attention to average hourly earnings. Economists are looking for a gain of 0.3%. If that’s close to accurate, then it tells me that the government shutdown didn’t have the impact I feared it would have.

Inflation has also been calm. The next CPI report will be out on January 13. The January Federal Reserve meeting is still three weeks away, and it increasingly looks like the Fed is ready to hold off on lowering rates. Not only that, but the odds of a rate cut in March are looking iffy.

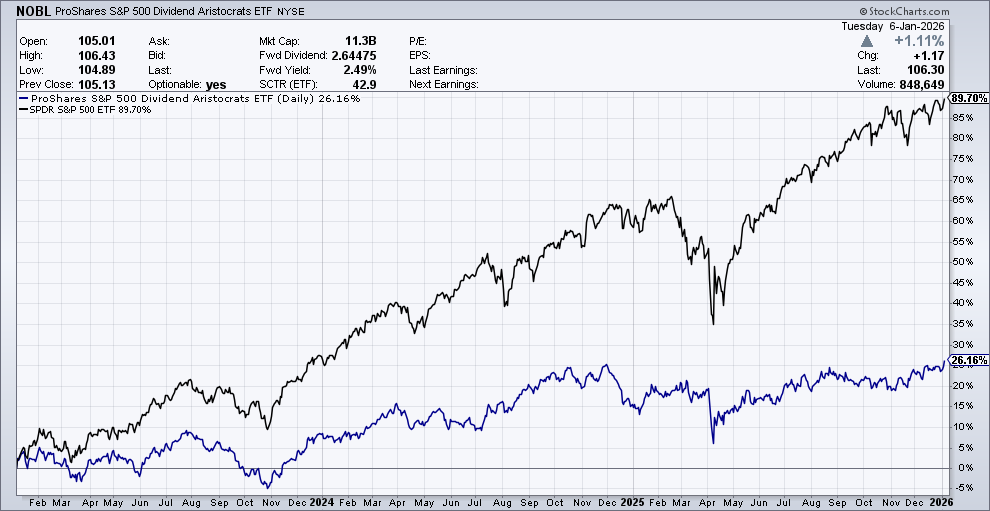

I want to share this chart with you because it might be the most frustrating chart about the recent market. The chart below shows the S&P 500 ETF (in black) against the S&P 500 Dividend Aristocrats ETF (in blue).

You can see that the overall market has soundly beaten the Dividend Aristocrats over the last three years. The market has more than tripled the Aristocrats. Actually, this chart understates the impact because the Dividend Aristocrats are inside the S&P 500.

The Dividend Aristocrats are companies that have raised their dividend every year for the last 25 years. Many have raised their dividend every year for 40 or 50 years.

I think of the Dividend Aristocrats as a good proxy for high quality companies. When I use the words “blue chip stocks,” this is what I mean. Many index makers have a “quality” factor for their indexes but I’m never exactly sure what metrics they use. With the Dividend Aristocrats, I have a good idea.

I find it alarming that high quality stocks have lagged the market by so much over the last three years. I certainly expect periods of underperformance, but this long stretch is very unusual.

This chart also shows us just how much the market has been influenced by a small number of lower quality stocks. The sad fact is that being safe and prudent has not been the most profitable strategy.

It’s not that conservative investors have lost money, but they’ve been left out of the biggest gains in a thriving bull market. I’m concerned that investors make take away the wrong lesson, but it’s hard to argue with success.

I’m not about to predict a resurgence of high-quality stocks, but these stocks can only lag the market for so long.

That’s all for now. The jobs report is due out Friday morning. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on January 6th, 2026 at 6:16 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His