CWS Market Review – March 24, 2026

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

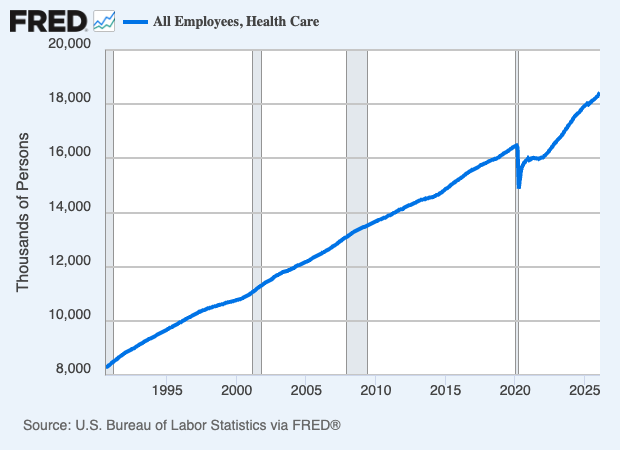

I recently came across a stunning fact in the Wall Street Journal. It said that over the last two years, the healthcare sector has accounted for 77% of all jobs growth.

That’s one of those facts that initially strikes you as amazing, but the more you think about it, the more it makes sense. As the rest of the economy gets weaker, the healthcare sector is doing most of the heavy lifting.

Check out the growth of healthcare jobs:

The WSJ notes that over the last year, the U.S. economy has added 156,000 new jobs and healthcare was responsible for 375,000 new jobs. That means that if we take away the healthcare sector, then the economy is shedding jobs. If you’re not at the doctor’s office, then you’re probably in a recession.

Don’t expect these trends to let up anytime soon. According to the WSJ, by 2035, the number of Americans over the age of 85 is expected to double. Now let’s look at what’s had the market so annoyed recently.

The Fed’s Next Move May Be a Rate Hike

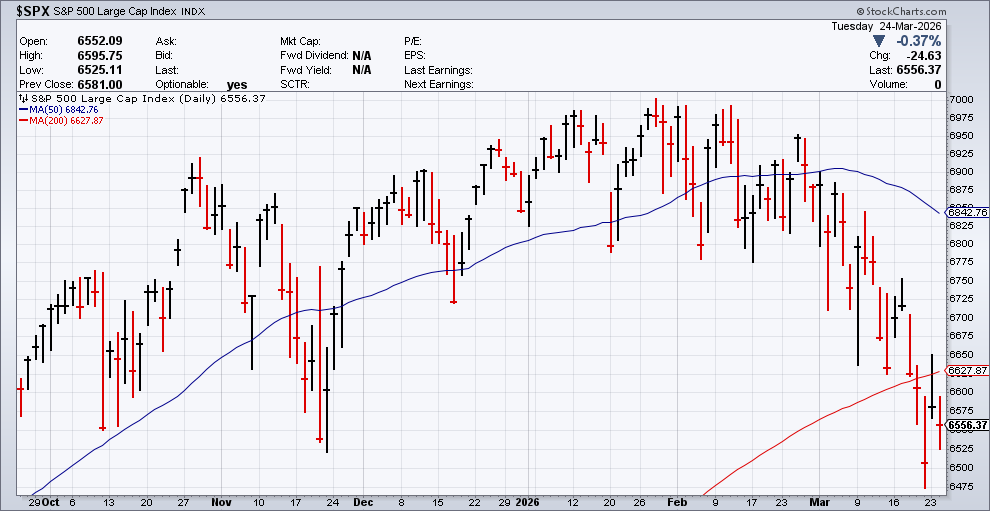

The stock market is starting to show some cracks. During the day on Friday, the S&P 500 fell to its lowest point in six months. We got a minor relief rally on Monday, but Tuesday was another down day. The S&P 500 has closed lower eight times in the last eleven sessions. The index is below its 50- and 200-day moving averages. Historically, that’s not a good sign.

There’s even talk of the Fed’s next move being an interest rate hike. To be sure, that possibility is still a long way from being a certainty, but the futures traders peg the odds of a Fed hike before the end of the year at around 20%. The odds of an upcoming interest rate cut are…well, in the garbage can. In a very short period of time, the odds of a Fed cut went from probable to not happening.

If you ever want to know what the Fed is thinking, the cheap and easy way is to look at the yield on the two-year Treasury. On February 28, the two-year yield was at 3.38%. By March 20, it got to 3.88%. That’s a jump of 50 basis points in less than one month. War has been the forerunner of inflation so many times in history.

What’s interesting is that the price of gold has been dropping lately. When hostilities started, gold was around $5,400 per ounce. Yesterday, gold got down below $4,100 per ounce. Gold often rallies during times of geopolitical stress. This time, the drop in gold makes sense if real interest rates rise. In plain English, lower gold hints that the Fed will have to raise rates well above the level of inflation. That’s not good for the economy.

There’s still a lot of fear in the markets, and the big issue is, not surprisingly, the price for oil. While oil is still well below its peak (near $120) from two weeks ago, it’s still elevated. For what it’s worth, betting markets don’t see traffic in the Strait of Hormuz returning to normal for several weeks.

The market was helped on Monday by an optimistic tweet from President Trump regarding “a resolution of hostilities” in the Middle East. The Iranians, however, said there have been no direct talks. Oil dropped down to $88 per barrel on Monday which is the lowest in two weeks. Before the war, oil was around $65 per barrel.

Oil stocks have been the big winner so far this year. The S&P 500 Energy ETF (XLE) is up about 38% in 2026, and the year isn’t yet one quarter over. I also like to keep my eye on the performance of the S&P 500 Industrial Sector (XLI). This is often an overlooked part of the market, but it’s very important for the overall economy.

Starting in December, industrials performed very well compared with the rest of the market. It was one of their best runs in 20 years, and it lasted through February. Since hostilities started, industrials have started to lag. That could be a sign for the entire economy.

We still don’t know the impact of Operation Epic Fury, outside of oil prices. It’s true that the U.S. economy is far less dependent on oil than it used to be. We’ll soon learn more. Next Friday, April 3, the government will release the March jobs report. This will show us how well the economy has been holding up.

We should also bear in mind that the labor market has been quite weak for the last several months. Less jobs growth means less money to go shopping and that cuts into corporate profits. For February, the U.S. economy shed 93,000 jobs.

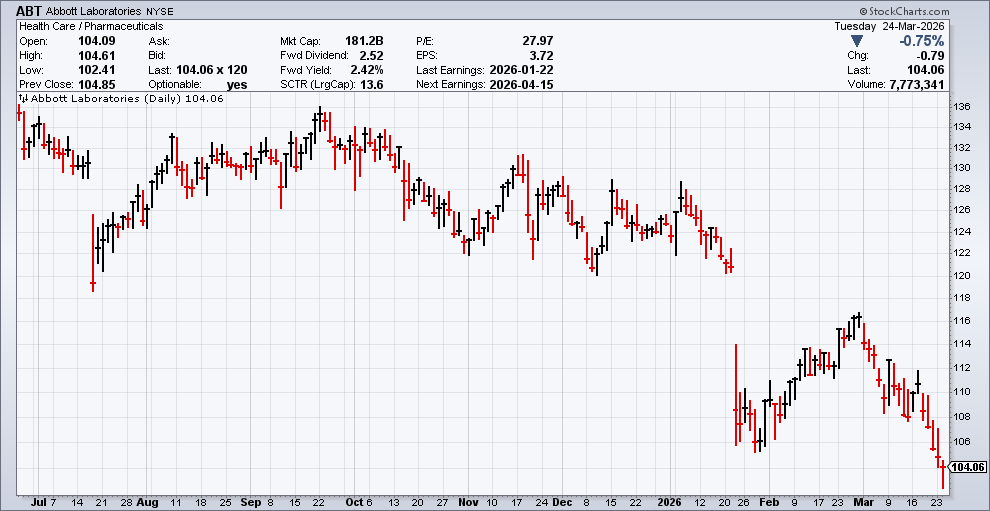

Abbott Labs Drops to a Good Price

One of our favorite Buy List stocks, Abbott Labs (ABT), has performed poorly. That puts off a lot of investors, but I always pay attention when the stock of a good company does poorly. That’s where you can often find a good bargain.

On January 22, Abbott reported solid earnings results, but the shares took a bath. Abbott Labs reported fiscal-Q4 earnings of $1.50 per share. That beat expectations by one penny. That was also inside the company’s own guidance for Q4 earnings of $1.47 to $1.53 per share. Abbott’s quarterly earnings were up 12% over last year.

For the full year, Abbott made $5.10 per share, which was up 10% over last year. CEO Robert Ford said, “Abbott is well positioned for accelerating growth in 2026.”

Despite the earnings beat, the stock got dinged due to poor results from its baby-formula business. The company offered mostly optimistic guidance. For 2026, Abbott sees earnings coming in between $5.55 and $5.80 per share. At the midpoint, that’s 10% growth. Wall Street had been expecting $5.68 per share. Abbott sees full-year organic-sales growth of 6.5% to 7.5%. For Q1, Abbott expects earnings between $1.12 and $1.18 per share. Wall Street had been expecting $1.19 per share.

Abbott’s Q4 sales rose by 4.4%. That’s organic growth of 3.0% to 3.8% when excluding Covid-testing sales. For 2025, sales were up 5.7%. That’s organic growth of 5.5%, or 6.7% when not counting Covid sales.

Abbott had Q4 sales of $11.5 billion, which was $300 million below expectations. Nutrition sales were $1.9 billion, which was well below expectations. Abbott said it was forced to raise the price for baby formula when manufacturing costs increased.

Medical devices are Abbott’s largest business. Quarterly sales were $5.67 billion, which matched estimates. The company just completed its acquisition of Exact Sciences for $21 billion. This should help the company expand its footprint.

In December, Abbott increased its dividend by 6.8% to 63 cents per share. This marks the 54th year in a row that Abbott has increased its dividend. Since 2020, the dividend has grown by 70%.

On Tuesday, shares of ABT fell to a new 52-week low. Going by the most recent price, ABT is currently going for about 17 to 18 times this year’s earnings. Bear in mind that Abbott’s estimates tend to be quite conservative. In our premium service, we rate ABT a strong buy up to $115 per share.

That’s all for now. The first quarter comes to a close next week. On Friday, April 3, we’ll get the jobs report for March. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. You can sign up for our premium service here.

P.P.S. Here’s something for fun I wrote earlier this week about math and March Madness:

Today is the day I’ll take something fun and ruin it with math! Who’s with me?

We’re in the middle of the NCAA basketball tournament. Most brackets are scored linearly, but here’s the big secret: basketball teams generally follow a Power Law distribution.

Simply put, this means that the difference in quality of teams tends to get smaller the lower you go. In practical terms, this means the #1 seed is really, really good. The quality difference between #2 and #3 tends to be smaller than the difference between #1 and #2. This continues through the entire bracket.

How can we see this in action? A good example is the bettor’s favorite, the #12 vs #5 game. Despite the difference of seven places, the teams aren’t that far apart. Historically, #12 wins about 35% of the time. It’s an upset, but a pretty minor one.

Interestingly, that’s close to the record of #3 against #1 (36%). In other words, the implied quality difference between those two spots is about the same difference with the seven spots between #5 and #12. That’s the Power Law in action.

For basketball fans, the Power Law means avoiding the #1 as long as you can, or hoping they get knocked out early. Earlier I mentioned the #12 seed. They’ve made it to the Sweet Sixteen 22 times, and 20 times they’ve faced off against #1. They’ve lost every single time.

The Power Law means the worst seed is #8 or #9. That means you have a very hard time getting to the Sweet 16 because you face #1 in Round 2. #1 has beaten #9 92% of the time.

The best seed is #11. Why? Because you avoid #1 for a long time. Assuming the higher seed wins, #11 plays #6, then #3, then #2, then #1.

Here’s the most remarkable stat. #11 has made to the Final Four more than #16, #15, #14, #13, #12, #10, #9, #8 and #7. #11 is tied with #6 and since they play each other in the first round, this means #6 follows the same course as #11.

The NFL avoids these issues because it “reseeds” its playoffs. Personally, I prefer how March Madness does it.

Posted by Eddy Elfenbein on March 24th, 2026 at 5:34 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His