CWS Market Review – April 14, 2026

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

In normal markets, traders keep their eyes on boring but important things like earnings, interest rates, industrial production and manufacturing.

Not anymore! In this market, the main drivers are things like ceasefires, the Strait of Hormuz and anything from Truth Social. Indeed, one tweet from the Commander in Chief can send the markets reeling, in any direction.

Lately, I’m pleased to say that it’s been good news that’s moving the market. To be very blunt, the stock market is chilling out in a major way. Only a few days ago, traders were scared witless.

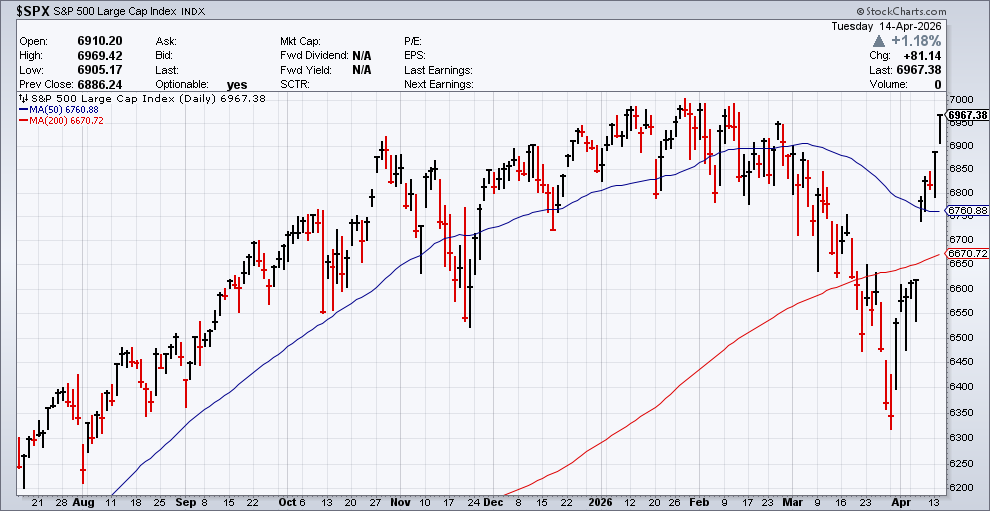

On Tuesday, the S&P 500 closed higher for the ninth time in the last ten days. The index is now above both its 50- and 200-day moving averages. In fact, we’re not too far from a new all-time high. Everything we lost during the war has been made back.

I should also note that the recent shift has been strongly tilted towards growth stocks. Over the last 10 days, growth has outgained value eight times. That’s a revealing stat. It suggests that the fear investors had is starting to wane.

The stock market was helped by President Trump saying that the Iranians want to talk. As Churchill said, it’s better to jaw-jaw than to war-war. The S&P 500 closed Tuesday at its highest level since hostilities began. It’s possible that talks may resume before the ceasefire ends.

Q1 Earnings Season Is Underway

We’re also starting to get earnings reports for the Q1 earnings season. On Monday, Goldman Sachs (GS) got the ball rolling. The big Wall Street bank said it made $17.55 per share which bested Wall Street’s forecast for $16.49 per share.

Despite the earnings beat, some of the details were disappointing. For example, income from Goldman’s fixed income, currency and credit products fell by 10%. On the plus side, Goldman’s investment banking fees rose by 48% to $2.84 billion. That was over $300 million more than expected.

Overall profits were up 19% to $5.63 billion. Shares of Goldman pulled back after the report, but the stock has been a pretty good performer over the last few years.

BlackRock (BLK), the ETF behemoth, said that its quarterly profits were up 46% over last year. For Q1, BlackRock made $2.2 billion. At the end of March, the company managed $13.89 trillion in assets. That’s actually down a tad since the start of the year.

For Q1, BlackRock made $12.53 per share which topped estimates of $11.65 per share. The stock rallied 3% on Tuesday.

Citigroup (C) also had a very impressive Q1. On Tuesday, the big bank said it made $3.06 per share for its Q1. That was above consensus for $2.65 per share. Citi made $1.96 per share for last year’s Q1. Revenue was $24.63 billion which was more than estimates of $23.55 billion.

The bank has been paring back on its operations in an attempt to make itself leaner. So far, Wall Street appears to approve. Citi has been the best performer of the major banks on Wall Street. Since the beginning of 2024, shares of Citi are up 170%.

Not all the companies that reported on Tuesday were banks. Johnson & Johnson (JNJ) also reported Q1 results. For the quarter, JNJ’s revenue rose nearly 10% to $24.1 billion. Earnings were $2.70 per share which was four cents above consensus. Like Goldman and JPMorgan, Johnson & Johnson is a member of the Dow Jones Industrial Average.

Johnson and Johnson had a super block-buster drug with Stelara. At one point it was brining over $10 billion in annual sales, but now it’s lost its patent protection and it faces competition. Sales of Stelara fell by 60%. JNJ also raised its full-year revenue estimates by a little bit. Since July, the stock is up over 55%.

Energy Prices Soared Last Month

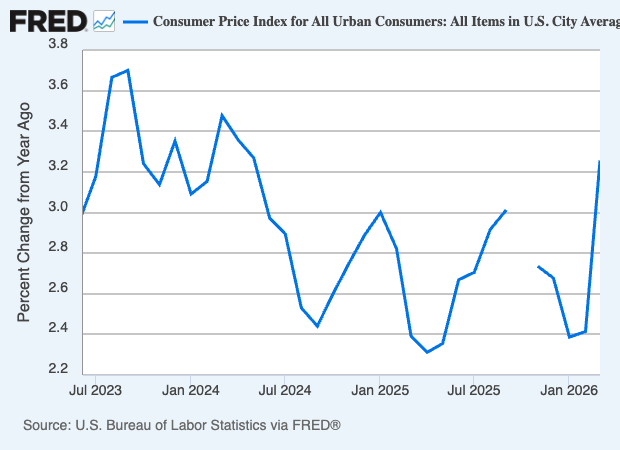

There’s been a lot of debate about Operation Epic Fury and its impact on the economy. For a long time, there’s been a lot of guessing but little in the way of hard evidence. We finally got a clue on Friday when the government released the inflation report for March.

For March, the CPI increased by 0.9%. Not surprisingly, that was helped by a 10.9% jump in energy prices, and gasoline prices were up by 21.2%. Over the last year, the CPI is up by 3.3%.

If we look past oil, then inflation isn’t so bad. For March, the core rate of inflation rose by just 0.2%. That was 0.1% less than forecast. Over the last year, the core rate is up by just 2.6%.

Here are some more details:

Services excluding energy rose 0.2% for the month and were up 3% from a year ago. Similarly, shelter was up 0.3% monthly and 3% annually, tied for its lowest level since August 2021.

Food prices were unchanged for the month and up 2.7% annually, with food at home falling 0.2%. Meat prices declined 0.6% while eggs fell another 3.4% and have tumbled 44.7% over the past year. New vehicle prices rose just 0.1%.

There were some signs of tariff and war impacts: airline fares jumped 2.7% while apparel climbed 1%.

The surge in the CPI meant that real earnings for workers decreased 0.6% for the month, as average hourly earnings rose just 0.2%. For the 12-month period, real average hourly earnings increased 0.3%.

The Federal Reserve meets again in another two weeks, and once again, I think we can dismiss any plans for a rate cut. In fact, I think it’s very doubtful that the Fed will make any changes to interest rates before the end of the year. According to futures traders, the earliest possible rate cut won’t be for another 14 months. That would bring us close to the middle of next year.

Wall Street is very concerned about rising energy prices, but it apparently thinks that won’t last. Next month, Kevin Warsh is due to take over as Fed Chair. By the way, we learned today from Mr. Warsh’s financial disclosure forms that he’s worth at least $135 million.

One concern is that the U.S. economy could find itself in “stagflation.” That’s when the economy weakens but prices rise, which is what we had in the late 1970s.

The problem with stagflation is that it puts the Fed in a tight spot. The economy needs lower rates in order to grow, but it needs higher rates in order to stave off inflation. In the early 1980s, the Fed raised rates to the ceiling. Interest rates came close to 20%. The economy faced a brutal recession, but it finally cleansed the economy of inflation.

That’s all for now. This week will mostly be about Q1 earnings and any news of ceasefire talks. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on April 14th, 2026 at 7:30 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His