CWS Market Review – May 12, 2026

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

It’s hard not to be impressed by the market’s recent rally. Through yesterday, the Nasdaq jumped more than 26% in six weeks, but this rally has been heavily skewed to tech stocks. Make that very heavily skewed. If we exclude tech names, then the market was up just 8.5% over those six weeks.

Today was one of the first days in a long time that the Nasdaq finally got some pushback. Here’s a remarkable stat: Ending on Friday, The Nasdaq Composite has outperformed the S&P 500 20 times in 24 days. The S&P 500 retreated today after closing at an all-time high on Monday.

There are a lot of folks out there sounding the “bubble alarm.” I prefer to ignore scaremongering. Peter Lynch famously said, “Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

Decent Jobs Report with Some Red Flags

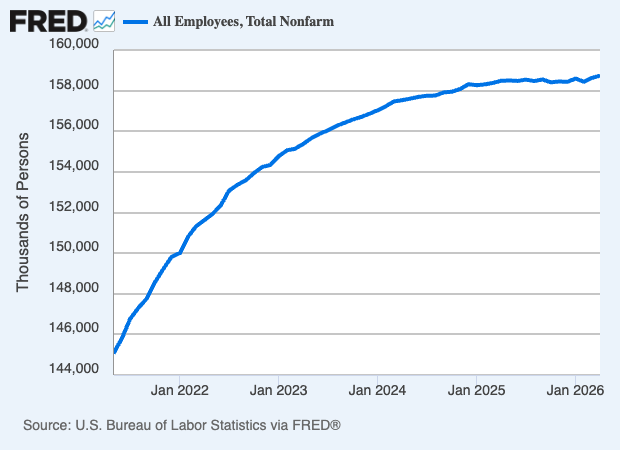

On Friday, the Bureau of Labor Statistics said that the U.S. economy created 115,000 net new jobs last month. That’s not bad. Economists had been expecting a gain of 55,000. April’s number was down from March, but that month was unusually strong with a gain of 185,00 new jobs.

As good as the report is, there are a few worrying items. For example, one problem spot is wages. Last month, average hourly earnings rose by just 0.2%. That was 0.1% lower than expected. Over the last year, earnings are up by 3.6%. That’s less than inflation, but not by much (I’ll have more on inflation in a bit). The overall unemployment rate held at 4.3% which is still low. It appears that we’re still in the no-hire, no-fire economy. Here’s a look at nonfarm payrolls. The line appears to be cresting:

Another concern is that the labor force is getting smaller. Also, the number of tech jobs is falling.

Here are some details:

Following recent trends, healthcare led with 37,000 new positions, though multiple other sectors also saw gains.

Transportation and warehousing added 30,000, retail rose by 22,000, and social assistance saw a gain of 17,000.

On the downside, information services lost 13,000, part of a continuing trend that has seen the category down 342,000 jobs since November 2022, coinciding with the rise of artificial intelligence. That has equated to a loss of 11% of jobs during the period.

The broader U-6 rate inched upward to 8.2%. The labor force participation rate dipped to 61.8%. That’s the lowest in close to five years. The jobs figure for March was revised upward by 7,000 while February was revised downward by 23,000 to a loss of 156,0000.

I don’t want to sound alarmist. The labor force is fine for now. My concern is if it will remain so in another six months. Frankly, those wages numbers need to get better.

The futures market doesn’t see the Fed making any changes on interest rates for the rest of this year, and they’re probably right. This week, the Senate looks to vote on Kevin Warsh’s confirmation to be the new Fed chairman. Jerome Powell’s term as Fed chairman expires on Friday, but he will stay at the Fed as a governor. The last Fed policy statement had the highest number of dissenting votes in 34 years. Get the popcorn, this could get interesting.

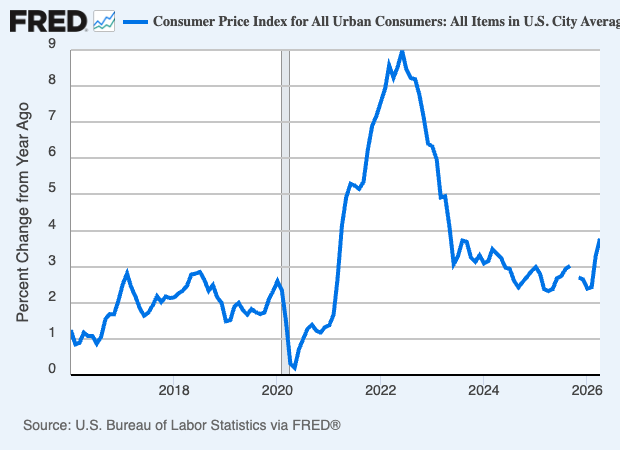

Inflation Hits a Three-Year High

This morning, we got the CPI report for April, and it wasn’t very good. Last month, headline inflation rose by 0.6% (yikes!) and the 12-month inflation rate is now at 3.8%. That’s the highest since May 2023. Wall Street had been expecting a monthly increase of 0.6%.

Of course, high energy prices are a significant factor, but even discounting that, inflation is still a problem. For April, the core rate, which excludes food and energy, rose by 0.4%. Over the last year, core inflation is running at 2.8%.

Here’s a look at gasoline prices via Gas Buddy:

The numbers from the energy sector are shocking. Last month, energy prices rose by 3.8% and food prices were up by 0.5%. For the last 12 months, energy prices are up 17.9%, and gasoline is up 28.5%. As always, bear in mind that energy prices impact everyone.

From CNBC:

Shelter costs rose 0.6% after easing in prior months, indicating that inflation is a problem beyond the Iran war impacts. The tariff-sensitive apparel category increased 0.6% and airline fares accelerated 2.8%, putting the 12-month gain at 20.7%. Tariffs also seemed to hit other areas, with household furnishings and operations up 0.7%.

New vehicle prices fell 0.2% while the index for used cars and trucks was flat. Medical care costs decreased 0.1% and hospital services were down 0.3%. Health insurance also declined 0.4%, while motor vehicle insurance increased 0.1%.

The report also contained bad news for workers, as real average hourly wages slipped 0.5% for the month and fell 0.3% annually.

These numbers put the Fed in a difficult spot. It’s as if the economy needs higher and lower rates at the same time. It needs higher rates to curb any inflation, but lower rates to prevent the labor market from deteriorating.

The Atlanta Fed’s GNDNow model currently sees Q2 GDP tracking at 3.7%. That’s high. If that’s right, then the economy is doing much better than expected. We’ll learn more later this week when the retail sales report comes out. Then on Friday, we’ll get the latest report on industrial production.

Sprouts Soars on Strong Earnings

Since we just finished the Q1 earnings season, I wanted to share our big winner with you, and that was Sprouts Farmers Market (SFM). Sprouts is new to our Buy List but it’s already making a splash.

Sprouts’s business idea is simple: take the look and feel of a farmer’s market and bring it indoors. Think of a big open space, but instead of waiting until the weekend, you can go to Sprouts any day of the week. Sprouts specializes in fresh and organic produce.

I’m particularly impressed by Sprouts’s loyal fan base. Sprouts tends to be less expensive than Whole Foods (owned by Amazon). Its smaller stores aren’t as crowded as Whole Foods, and Sprouts has found an overlooked part of the market: people who want good, fresh, organic produce but not at Whole Foods’s prices.

After the closing bell on April 29, Sprouts said it made $1.71 per share for its fiscal Q1. That’s for the 13-week period ending on March 29. The stock jumped 15% the next day. The CEO said the quarters “played out largely as we expected.”

SFM’s Q1 sales were up 4% over last year. The key figure is that same-store sales were down 1.7%. That’s not good, but it shows some signs for optimism. During the quarter, the company owned six new stores, which brings the total to 483 stores.

For Q2, Sprouts sees earnings between $1.32 and $1.36 per share and same-store sales growth between -2% and flat.

For all of 2026, SFM sees same-stores sales growth between -1% and +1% and earnings between $5.32 and $5.48 per share. The shares have rallied another 6% since the big jump after its earnings. I currently rate Sprouts a buy up to $90 per share.

That’s all for now. The retail sales report is due to come out on Thursday. It will be interesting to see if the war in Iran has had an impact on shopping. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on May 12th, 2026 at 7:11 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His