CWS Market Review – May 22, 2026

“In a roaring bull market, knowledge is superfluous and experience is a handicap.” – Benjamin Graham

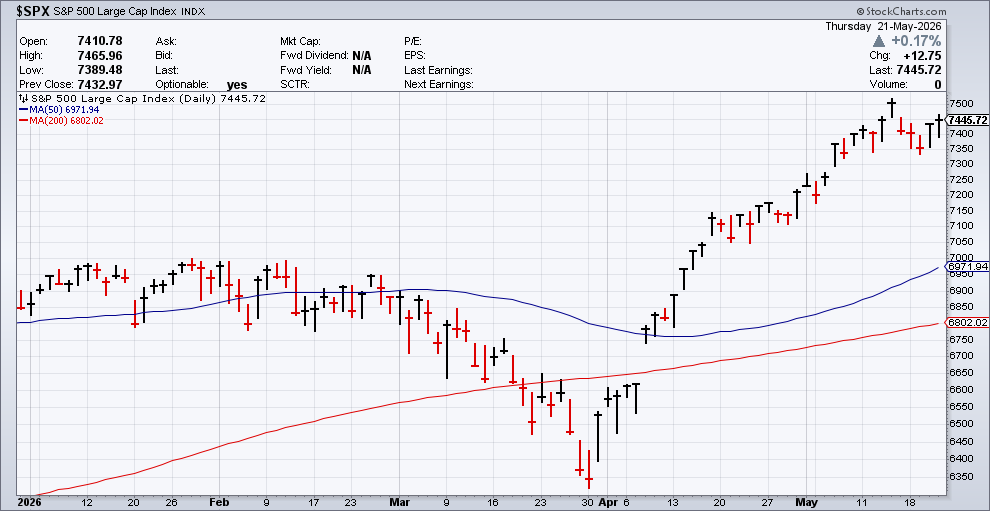

On Thursday, the S&P 500 came very close to falling for the fourth time in the last five days, but a late-day rally staved off the decline. In the grand scheme of things, the market’s recent hit is barely a flesh wound. The market is still up a good 17% since late March.

What’s notable about the downturn is that it’s been led by growth stocks. That’s something new. For the last several weeks, growth stocks have pulverized value. Every day, it seemed, tech stocks led and defensive stocks lagged. But now, the market could be turning.

A good example is healthcare stocks. Historically, this has been a great sector for investors, but healthcare has gone nowhere in 2026. That is, until a few weeks ago. Now healthcare is finally out in front.

Healthcare isn’t alone. On our Buy List, stocks like FactSet and FICO are finally showing some strength. In the last week, FICO is up 14%.

Could this be the start of a large-scale rotation? Eh, I’m not so sure. The major concern on Wall Street at the moment is finding out how badly higher oil prices are hurting consumer spending. Higher prices at the pump act like a tax on consumers.

This week, Walmart reported same-store sales growth, excluding fuel, of 4.1%. That’s pretty good, and it beat expectations. The problem was that guidance was sluggish. Walmart said that its customers are buying less gasoline. In Thursday’s trading, Walmart had its largest drop in nearly three years.

Earlier this week, the Federal Reserve released the minutes from its most recent meeting. The minutes showed that the Fed is beginning to consider raising interest rates. The idea of rate cuts seems to be off the table.

That’s not a big surprise. The important metric to watch is the yield on the two-year Treasury, which is often a tell for what the Fed may do. The yield on the two-year has been on the way up, and it recently broke above 4.1%, which is well above where the Fed currently has rates.

The key is inflation. The problem for the Fed is that it’s not just about oil prices. The price for fuel finds itself buried inside the price for nearly everything. The next CPI report will be out on June 10, and the Fed’s next meeting will be on June 16-17.

If there is movement on interest rates, it may not happen for some time. The futures market currently sees the Fed raising rates, but not until December.

Decisions within the Fed may soon get interesting. Mr. Warsh has just taken over, and the last policy statement had four dissenting votes, three of which didn’t want to include language regarding an easing bias.

I should explain. The Fed’s minutes are a study in the use of indefinite pronouns. Fed watchers carefully try to parse what exactly “some said this” and “a few said that” truly mean. In this case, “many” said they also didn’t want an easing bias. This could signal that there are more votes for higher rates. But how many is “many”? I don’t know, but we may soon find out.

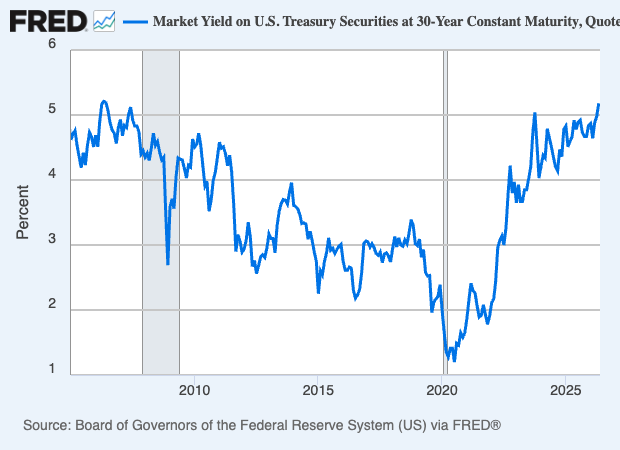

What’s changed recently is that interest rates have moved higher. The yield on the 30-year Treasury recently got to 5.18%, which is a 19-year high (see chart above). For comparison, during the initial Covid panic, the yield got down to 0.99%. The 10-year yield has risen from 4% in February to as high as 4.67% this week. This impacts everything from mortgages to corporate mergers.

For the immediate future, I expect to see growth stocks continue to lag, but it will probably be in a zigzag fashion. Many tech stocks are due for a reckoning.

In this week’s issue, we’ll look at Thursday’s earnings report from Intuit. The company beat expectations and raised guidance, but got hit hard after it said it will lay off 17% of its workforce. I’ll have the details in a bit.

I’ll also preview next week’s earnings report from Heico. I also have some Buy List updates for you. First, though, let’s look at what Intuit had to say.

Intuit Falls after Earnings Beat

After the closing bell on Wednesday, Intuit (INTU) said its global revenues rose 10% to $8.6 billion, and its earnings rose 10% to $12.80 per share. Wall Street had been expecting earnings of $12.57 per share. Intuit is the company behind TurboTax and QuickBooks and Credit Karma.

Intuit’s consumer revenue grew 8% to $5.3 billion. TurboTax revenue was up 7% to $4.4 billion, and Credit Karma revenue grew 15% to $631 million.

Global Business Solutions revenue was up 15% to $3.3 billion. Excluding Mailchimp, Global Business Solutions revenue grew 17%, and Online Ecosystem revenue grew 22%.

Intuit’s CEO, Sandeep Aujla, said, “We delivered a strong third quarter of fiscal 2026, reflecting our operational focus and scaling of our growth engines across the business. As a result, we are raising our full-year revenue guidance for fiscal 2026.”

During Q3, Intuit bought back $1.6 billion worth of stock, and the board approved a new $8 billion buyback authorization. Inuit also increased its dividend by 15% to $1.20 per share.

The biggest news is that Intuit said it will reduce its full-time workforce by 17% in order to “simplify its organizational structure and become a faster, leaner, more focused company.” Intuit estimates that it will incur restructuring charges of $300 to $340 million that will be recognized in Q4.

For its Q4, which ends on July 31, Inuit expects revenue growth of 11% to 12% and earnings between $3.56 and $3.62 per share. For the entire year, Intuit sees revenue growth of 13% to 14%. That’s up from the prior guidance of 12% to 13%.

For earnings, Intuit sees a range of $23.80 to $23.85 per share. That’s an increase from the previous range of $22.98 to $23.18 per share. Despite the earnings beat and higher guidance, traders focused on the job cuts. By the closing bell, Intuit traded down 20% to $307 per share. I’m lowering our Buy Below on Intuit to $320 per share.

Preview for Heico’s Earnings Next Week

Heico (HEI) is due to report its fiscal-Q2 earnings after the closing bell on May 27. The stock has started off slow for us this year, but I still like this company. The shares have improved some in recent weeks. The stock is on pace for a 15% gain this month.

In February, Heico reported fiscal-Q1 earnings of $1.35 per share. That’s up 13% over last year, and it topped Wall Street’s consensus by six cents per share. Quarterly sales were up 14% to $1.179 billion, and Heico’s operating margin increased a little bit to 22.1%.

Heico has two operating segments, the Flight Support Group and the Electronic Technologies Group. For Q1, Flight Support reported sales growth of 15% and operating-income growth of 21%. Electronic Technologies had quarterly sales growth of 12%, but its operating income fell 4% to $73.2 million.

Heico said the decrease in operating income was due to “a less-favorable product mix of defense products and the previously mentioned decrease in net sales of space products.”

The weakness in Electronic Technologies upset the market, and shares of HEI fell after the report. I’m not worried about Heico at all. This is a very good company. For next week, the consensus on Wall Street is for Heico to report earnings of $1.33 per share.

Buy List Updates

Shares of FactSet (FDS) and FICO (FICO) have become popular in recent days. Over the last month, FICO is up by 25%. This week, I’m raising our Buy Below on FICO to $1,300 per share.

The Motley Fool had nice things to say about Comfort Systems USA (FIX). The stock still isn’t well known, but it’s been a very big winner for us.

Barron’s recently profiled Casey’s General Stores (CASY). The shares have been on a nice run this year. The company is also having success with its new chicken wings.

Barron’s writes:

Gas prices show no signs of retreating from north of $4.50 a gallon on average in the U.S., crimping household budgets, and though convenience stores benefit from price volatility, consistently high levels are a headwind for the group.

Consensus calls for Casey’s earnings per share to climb 26.7% to $3.33, while a majority of the 19 analysts tracked by FactSet have raised their estimates for the quarter in the past three months.

Nonetheless, even if there is an understandable post-earnings dip, it would be wrong to assume that Casey’s run is done.

The stock was added to the S&P 500 last month. The next earnings report is due out on June 9. Casey’s remains a buy up to $900 per share.

That’s all for now. The stock market will be closed on Monday in honor of Memorial Day. There are a few important economic reports to look out for. On Tuesday, we’ll get the report on consumer confidence. Thursday is new-home sales, orders for durable goods and initial jobless claims. On Friday, the government will revise its report on Q1 GDP growth. The initial report said that the U.S. grew in real annualized terms of 2.0%. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on May 22nd, 2026 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His