CWS Market Review – May 8, 2026

“We suffer more in our imagination than in reality.” – Seneca

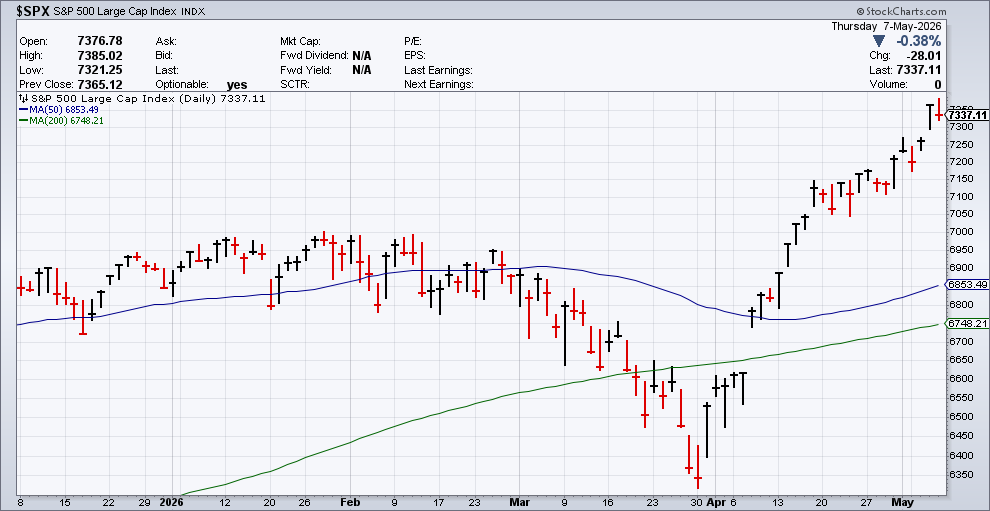

It’s hard to not be impressed by this latest market surge. As you know, I’m not one for predicting bubbles, but things are getting a bit unreal.

Since March 30, the S&P 500 has gained 15% while the Nasdaq is up more than 24%. Over that time span, the S&P 500 Tech ETF is up by 33% while the non-tech part of the index is up a scant 9%.

It’s an odd market when you’re up by 9% in a little over a month and yet feel that you’ve badly underperformed the market.

Crude oil fell recently on the hopes that some deal can be reached between Iran and the U.S. regarding the Strait of Hormuz. Consumers are feeling stretched. Shares of Whirlpool got clocked on Thursday after the appliance maker said that its business has run into a brick wall.

The New York Fed released a report this week that said that lower-income folks are feeling the pinch of higher gasoline prices.

So far, this has been a good earnings season for our Buy List. Except for American Water Works and Stryker, every stock either beat or met earnings.

Last Friday, IES Holdings had a blowout earnings report and the shares rallied to a 52-week high. Allison Transmission beat earnings by more than 20%. Henry Schein beat earnings and reaffirmed guidance. McKesson beat earnings and offered strong guidance.

FactSet gave us a nice dividend hike. This is the 27th year in a row that FDS has raised its dividend. Cencora beat earnings and raised guidance, but it lowered its sales forecast. I’ll go over the details in a bit. But first, let’s look at our final Earnings Calendar for Q1.

Q1 Earnings Calendar

Here’s our complete earnings calendar for the first quarter of 2026:

Five Buy List Earnings Reports

Last Friday, shortly after I sent you last week’s issue, IES Holdings (IESC) reported its fiscal Q2 earnings. For the quarter, the company made $4.16 per share. That’s up 26% over last year’s Q2. Not enough analysts follow IESC for us to say there’s an earnings consensus.

The numbers were pretty good. Quarterly revenue rose 17% to $974 million. Operating income was up 21% to $112.3 million. As of March 31, IES had a backlog of approximately $3.9 billion. That’s a good sign for future business. The company’s business is divided into four divisions: Communications, Residential, Infrastructure Solutions and Commercial & Industrial.

Management said that while the other divisions were doing well, their Residential division “faced continued pressure from weak housing starts and unfavorable weather.” The company also said that it’s started “to see growth in our multi-family backlog.”

IESC said it “ended the quarter with $49.5 million of cash, $35.0 million debt, and $214.0 million of marketable securities.” During the quarter, the company bought back 4,112 shares for $1.7 million, or an average price of $418.31 per share. IESC ended the quarter with $166.2 million left in the current buyback authorization.

IESC is a large and multifaceted business. If you want to learn more about the details of IESC, you can check out this Investors presentation from earlier this year. This week, I’m raising our Buy Below on IESC to $700 per share.

After the close on Monday, Allison Transmission (ALSN) reported very good earnings for its fiscal Q1. This is good to see because Allison missed its Q4 earnings but offered reassuring guidance.

For Q1, Allison made $2.57 per share compared with estimates of $2.10 per share. Net sales were up 84% to $1.4 billion, but that figure includes Allison’s Off-Highway which was added at the start of this year.

Allison ended Q1 with $311 million of cash and cash equivalents, and $845 million of available borrowing capacity under its revolving credit facility.

For this year, Allison expects consolidated net sales of $5,575 to $5,925 million, and net income in the range of $600 to $750 million. Both of those are unchanged from the previous guidance. The guidance works out to 2026 earnings of about $2.50 per share.

Allison is turning into a nice winner for us this year. We’re sitting on a 26% YTD gain. Allison remains a buy up to $130 per share.

On Tuesday afternoon, Henry Schein (HSIC) reported Q1 earnings of $1.32 per share. That’s up 15% over last year’s Q1 and it topped Wall Street’s consensus by 10 cents per share.

If you’re not familiar with Henry Schein, it’s a one-stop shop for healthcare products with a focus on dental supplies and veterinary products.

This was a good quarter for HSIC. CEO Fred Lowery said, “I am pleased with our strong first quarter results that reflect continuing momentum from the second half of last year as we grow market share and expand gross margins.”

Total net sales were up 6.3% to $3.4 billion. Adjusted EBITDA for the quarter was $289 million, up from $259 million for last year.

During Q1, HSIC bought back $1.6 million shares at an average price of $77.64 per share for a total of $125 million. They’re not done. The company has another $655 million authorized to buy back more shares.

The company also stood by its guidance for this year. HSIC expects earnings to range between $5.23 and $5.47 per share. It also sees sales growth of 3% to 5%. This week, I’m dropping our Buy Below on Henry Schein to $80 per share.

On Wednesday, before the opening, Cencora (COR) said it had Q2 sales of $78.4 billion. That’s up 3.8% over last year but it was below Wall Street’s expectations. Cencora also lowered its full-year sales guidance to growth of 4% to 6%. The previous guidance had been for sales growth of 7% to 9%.

Cencora blamed the lower guidance on “lower expectations for revenue growth in the U.S. Healthcare Solutions segment.” Traders punished the stock on Wednesday’s trading. By the closing bell, Cencora had lost 17%.

Still, the company had a decent Q2, plus it raised its earnings guidance. Cencora’s Q2 earnings rose 7.5% to $4.75 per share. That beat the Street by two cents per share. Cencora raised its full-year guidance range to $17.65 to $17.90 per share. The previous guidance was $17.45 to $17.75 per share.

Cencora recently bought the equity it didn’t already own in OneOncology, a leading management-services organization for oncology practices.

CEO Robert P. Mauch said, “As we move into the second half of our fiscal year, we are pleased to have made progress on debt paydown and to be in a position to resume opportunistic share repurchases.” Cencora said it’s aiming to buy back $1 billion in shares this year.

I know this was a tough week for Cencora, but I still like the stock. It’s been a nice winner for us. This week, I’m dropping our Buy Below on Cencora to $275 per share.

On Thursday, McKesson (MCK) reported fiscal Q4 sales of $96.3 billion. That’s an increase of 6%. Earnings rose 16% to $11.69 per share which was 12 cents more than estimates.

McKesson started a $2.25 billion accelerated share buyback program. The board also approved a $5 billion increase to the current buyback program. That brings the total authorization to $7.7 billion.

For the entire fiscal year, McKesson increased its revenues by 12% to $403.4 billion. Earnings increased 18% to $39.11 per share. Cash flow from operations was $6.2 billion and free-cash flow was $5.4 billion. Last year, McKesson returned $5.1 billion to shareholders through $4.8 billion of stock repurchases and $381 million of dividends.

For the new fiscal year, McKesson expects earnings of $43.80 to $44.60 per share. That’s an increase of 12% to 14%. The company targets a long-term growth of 13% to 16%.

I’m impressed by these numbers. McKesson is a buy up to $1,000 per share.

Buy List Updates

FactSet (FDS) announced that it’s raising its quarterly dividend from $1.10 to $1.16 per share. This is the 27th consecutive year that FactSet has increased its dividend. The new dividend will be paid on June 18 to holders of record at the close of business on May 29.

A few weeks ago, FactSet reported very good earnings. For its fiscal Q2, FactSet made $4.46 per share which was eight cents better than Wall Street’s forecast. The company also increased its full-year guidance range to between $17.25 and $17.75 per share. The Q3 earnings report will be sometime in mid-June. FactSet is a buy up to $220 per share.

That’s all for now. No more earnings next week. However, we’ll soon be upon our off-cycle stocks. That means will soon get earnings reports from stocks like Heico and Intuit. The big econ report to look out for will be Tuesday’s CPI report. We know Americans are paying more for gasoline, but has that spilled over into other areas? On Thursday, we’ll get the retail sales report. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on May 8th, 2026 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His