CWS Market Review – June 9, 2026

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

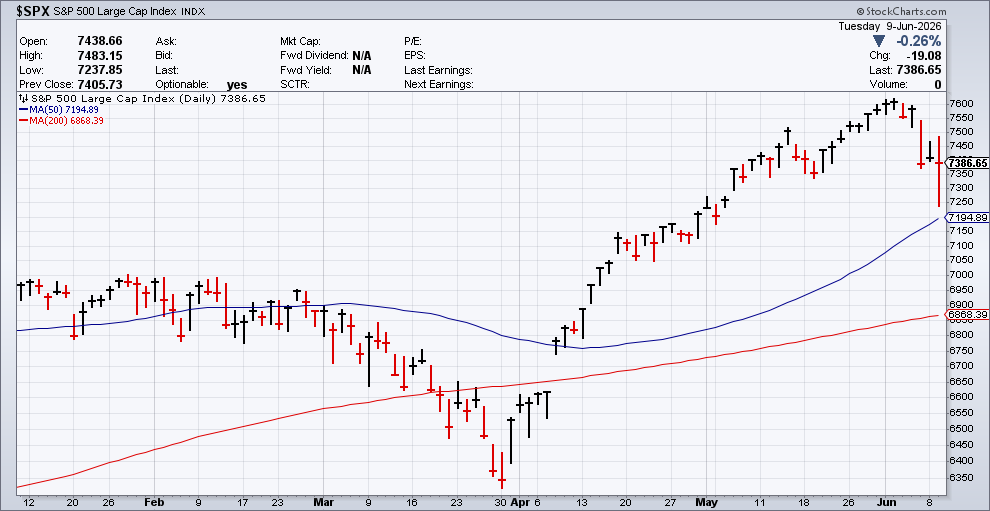

Last Tuesday, the stock market closed at an all-time high. We’ve gotten used to new highs, but what changed was what came after that on Thursday and Friday. That’s when many large-cap tech stocks, semiconductors in particular, got hit very hard. Many semis fell more than 10% in one day.

What caused the semi rout? As usual, it was a combination of factors. For one, valuations are quite high. Also, these stocks have been very popular so some pushback shouldn’t be surprising.

The market was also spooked by Broadcom’s earnings. Actually, the earnings were quite good, but it was disappointing guidance that scared investors.

Semiconductor Stocks Plunge

It sounds almost comical, but the market was upset that Broadcom didn’t increase its revenue guidance for this year and next year. In other words, keeping the guidance the same is seen, in practical terms, as a downgrade. That should tell you something about the current mood on Wall Street.

The stock market rebounded some on Monday but today was more of a raucous day. Stocks opened higher but fell as the morning went on. At one point, the S&P 500 was off by more than 2.2% and the Nasdaq was down much more than that. Later on, the bulls showed up to pare some of the losses. Still, you can see how easily stocks got pushed around. That’s very different from the market’s behavior earlier this spring.

The broader market was briefly helped by optimistic news from the Middle East. The price of oil fell close to 4% after Energy Secretary Chris Wight said that ship traffic is increasing in the Strait of Hormuz. Gold fell more than $130 per ounce on Friday. President Trump said that a deal to open the strait is “two or three” days away. This is encouraging, but I’m a realist about such matters. I’ll believe it when I see it.

On Tuesday, the Dow Jones Transports were up over 1.3% while the Dow Jones Industrials were little changed (+0.2%). These sector rotations are becoming more pronounced.

Over the past week, High Beta stocks have fallen on hard times. By High Beta, I mean stocks that tend to fluctuate a lot. At the other end of the spectrum, low volatility stocks have been remarkably calm.

Over the last five trading days, the S&P 500 High Beta ETF (SPHB) has fallen by 5.4% while the S&P 500 Low Vol ETF (SPLV) has gained 2.8%. That’s a very large spread, especially for such a short period of time. Of course, this is merely the opposite of what the market had been doing for several months.

Here’s a chart of High Beta (red) versus Low Vol (blue):

This week, Bank of America (BAC) warned investors that its stock market signals started flashing red. Charlie Bilello, one of my favorite stats guys, recently said that the yield on the S&P 500 has dropped below 1%, and it’s heading toward its all-time low of 0.94% from 2000.

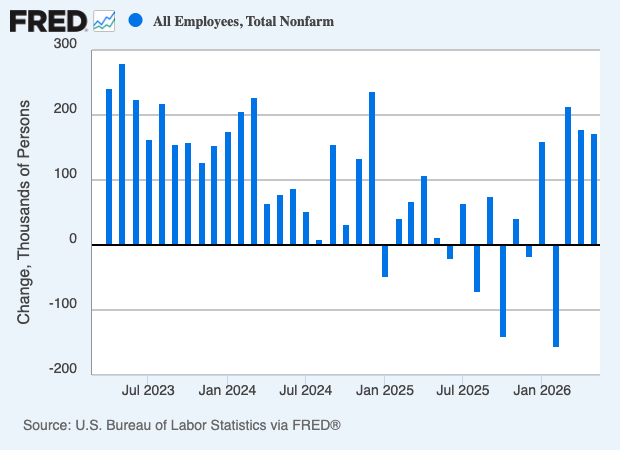

The Economy Created 172,000 New Jobs in May

On Friday, the government released a surprisingly strong jobs report. The Bureau of Labor Statistics said that 172,000 net new jobs were created in May. That more than doubled expectations. The number for April was revised higher to 179,000.

The unemployment rate held steady at 4.3%. The unemployment rate has been either 4.3% or 4.4% for each of the last six months.

They key number that I’ve been looking for is average hourly earnings. More pay for workers means more business for companies. For May, average hourly earnings increased by 0.3% which matched expectations. That’s a good number but not a great one. Over the last year, average hourly earnings are up by 3.4%.

Here are some details:

Leisure and hospitality led all sectors with 70,000 jobs, well above the 14,000 per month average over the past year and a possible reaction to hiring needed for the World Cup.

Local government added 55,000.

Health care, which has been the leading sector, contributed 35,000 new hires, about in line with its average. Social assistance added 12,000.

It’s frustrating to see job growth concentrated in a few sectors. In addition to the strong job numbers for May, revisions for prior months also presented an even better picture.

The nonfarm payroll report for April was revised higher by 64,000. The number for March was raised to 214,000, which is a gain of 29,000. The labor force participation rate was stable at 61.8%. The broader U-6 unemployment rate dropped a little to 8.1%.

The Federal Reserve meets again next week. Don’t expect any movement on interest rates, but the Fed’s outlook could be slowly changing. The yield on the two-year Treasury has climbed higher in recent weeks. The yield recently hit its highest point in over a year. The 10-year yield recently broke above 4.6%.

Traders don’t see the Fed hiking rates next week, or at the meeting after that or the meeting after that. But in the one after that, in December, the market sees the Fed hiking interest rates by 0.2%. I’m skeptical of forecasts going out that far, but it does signal to investors that the market sees the Fed getting more aggressive sometime soon. Last week’s jobs report is more evidence.

On Wednesday, we’re going to get the CPI report for May, and it could be an ugly one. FactSet said the median estimate is that inflation is running at 4.2%. The Atlanta Fed’s GDPNow model sees Q2 GDP growth running at 3.3%. We did get some negative news this morning. Small business optimism fell to its lowest level since October 2024.

FICO Announces $2.0 Billion Share Buyback

We had good news from one of our Buy List stocks. Yesterday, FICO’s (FICO) Board of Directors approved a stock repurchase program. Under the program, FICO will buy up to $2.0 billion of the company’s outstanding stock.

The new program replaces what’s left in the previous $1.5 billion stock repurchase program. FICO also said it will borrow $1.5 billion to fund its accelerated share repurchase plan.

Shares of FICO have done well in recent weeks, Since April 22, FICO is up 32.8% for us.

The last earnings report was quite good. On April 28, FICO said its net income jumped 60% to $12.50 per share. Free-cash flow was $214.3 million, compared with $65.5 million last year. Quarterly revenue rose 30% to $691.7 million.

FICO also raised its guidance. Before, FICO expected full-year revenues of $2.35 billion. Now it expects revenues of $2.45 billion. FICO raised its full-year earnings guidance from $38.17 to $40.45 per share. The next earnings report should be out sometime late next month.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on June 9th, 2026 at 7:28 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- August 2026

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His