Author Archive

-

This Just In….

Eddy Elfenbein, May 6th, 2010 at 10:49 amOhhhhh!

*Smacks Forehead*

Now they tell us! -

More on Repurchases

Eddy Elfenbein, May 6th, 2010 at 9:53 amI got a number of emails is response to yesterday’s screed against share buybacks. Here’s a thoughtful response from a reader.

First, I’m a fan of your blog, and read it every day. (I even own some NICK 🙂

I’m having trouble understanding your antipathy to buybacks.

If you believed (bear with me) that stocks were always correctly priced, then you would prefer buybacks to dividends for stocks in you taxable accounts because of the tax advantages. And this is true even if the nominal tax levels on dividends and capital gains are the same, because capital gains taxes can usually be deferred for a long time (maybe even forever, for example if you make a lot of charitable contributions), while dividend taxes are impossible to escape.

But of course stocks are not always correctly priced. In this case, you’d want the firm to buy back stock when the stock was cheap and issue stock when it’s expensive. Since the entire premise of your project is that you can identify cheap stocks, you should be happy to hear that one of your holdings is using their cash to buy back shares which you presumable believe are cheap.

You are a buy-and-hold investor, who will hold the firm for as long as it’s cheap, so you don’t need to worry about whether the buyback is immediately correctly reflected in the stock price…the buyback will increase earnings-per-share, and this will eventually be reflected in the price.

This also helps get rid of the excess cash which might otherwise be squandered by the firm. You could also do this via a one-time cash dividend, but then again there would be a big tax hit. You could raise your regular dividend, but then you might find you have to cut it, and firms are reluctant to do that for signaling reasons.

Of course the problem with buybacks is that firms might do them when the stock is expensive. In theory, executives should be able to use their inside knowledge to do more repurchases when the stock is cheap, but it’s not clear how much that really happens. Also, what is seen as “cheap” changes with the overall level of optimism in the economy.

But again, since you believe you can identify and hold cheap stocks, you should be happy when one of your holdings makes a purchase of cheap stock on your behalf. What am I missing?It’s hard for me to argue against this because everything he says is correct. My stand against share buybacks is far more primal. I just want the cash, and I’m happy to leave the theory stuff to someone else.

If it’s not advantageous tax-wise, fine—change the law. If the stock is still cheap, fine—give me the dividend and I’ll decide if I want to reinvest it or not. I just want the money.

David Berman, who writes the terrific Market Blog for the Globe and Mail, writes:Mr. Elfenbein’s argument would be a lot stronger if he could show that companies are notoriously bad at timing share buybacks – that is, buying their own stocks at high prices and therefore wasting their money.

According to Standard & Poor’s, companies in the S&P 500 bought $47.8-billion (U.S.) worth of shares in the fourth quarter of 2009, up more than 37 per cent from the previous quarter. However, this is still well below the frenzy of buyback activity in 2007, a year that coincided with a peak in the S&P 500 before the onslaught of the financial crisis.

Companies, it seems, like their own shares when they’re pricey.For me, it’s a point of principle (and principal, for that matter). I don’t want the companies I own to be in the business of timing their stock. That’s my job. Their job is to run the business and make as much money for me as they lawfully can. I’m the owner. Let me worry about what to do with the profits.

Another reader writes:I definitely agree with you on preferring dividends compared to repurchases, at least in 99% of cases. You cited the case of Cisco, which has spent tens of billions to no apparent effect. The more pernicious thing about repurchases is that many companies only use them to soak up the equity dilution from option issuance to employees. Yet billions of dollars are spent on repurchases, without actually shrinking the float. Take a look at the recent Goldman Sachs quarter; they spent a couple of billion buying back 13.2 million shares to offset option issuance, but actually had 16 million more average shares outstanding (basic) and 6 million more shares outstanding (diluted) at the end of the quarter, compared to the end at Dec. 31/2009.

I’m not sure if all companies are now required to report EPS including option issuance as compensation expense; if they are, that’s fine. But if they’re not, then companies get to boost EPS too, by diverting an expense item into the balance sheet item of retained earnings.

Give me the dividend!This is an excellent point. I don’t mind executives being compensated with stock, but share repurchases make it very easy for them to mask shareholder dilution.

-

Leucadia’s Earnings

Eddy Elfenbein, May 6th, 2010 at 9:04 amYesterday, Leucadia National (LUK) reported its earnings results. I almost have to place an asterisk next to Leucadia. The company is, shall we say, reserved about corporate communications. If you want to see what I mean, this is the company’s website. Yes, that’s the whole thing.

Let me back up and explain. Leucadia is very similar to Warren Buffett’s Berkshire Hathaway except it’s about one-thirtieth the size. The stock has done about as well as Berkshire over the last few decades. The big difference is that the owners, Ian Cumming and Joseph Steinberg, are extremely media shy. The company owns a grab bag of companies involves in several industries. It’s not an easy stock to evaluate. Leucadia has no analyst coverage and the earnings reports are celebrated by very thin press releases.

This is what they had to say yesterday:Leucadia National Corporation today announced its operating results for the three month period ended March 31, 2010. Net income attributable to Leucadia National Corporation common shareholders for the three month period ended March 31, 2010 was $191,479,000 or $.78 per diluted common share as compared to net loss attributable to Leucadia National Corporation common shareholders for the three month period ended March 31, 2009 of $(140,007,000) or $(.59) per diluted common share.

If you want to check out the details of their business, you can read the latest 10-Q. It’s fairly detailed. I’m pleased to note that Leucadia has a stake in AmeriCredit (ACF) which is in the lucrative field of financing for used cars.

Here’s a Barron’s article on Leucadia from 2008.

-

The Crossing Wall Street Tax Code

Eddy Elfenbein, May 6th, 2010 at 8:58 amI want to thank everyone who participated in our weekend poll, “How much federal income tax should a family of four that makes $25,000 pay?” We had over 600 responses.

This is the fifth time we’ve run that poll. The other income values we used were $40,000, $100,000, $250,000 and $1 million.

Using some interpolation, I tried to find the median vote for the tax rate for each poll. Here’s what we have:

$25,000: 2.66%

$40,000: 8.31%

$100,000: 16.33%

$250,000: 22.69%

$1,000,000: 28.23%So the collective wisdom favors a progressive income tax. (Please note that this is not necessarily my opinion, it’s what the poll said.)

Using a little math, we can make a three-bracket tax code that links the data above. It looks like this:

The first $21,249 is tax free.

$21,249 to $74,266 is taxed at 17.79%

$74,266 to $250,000 is taxed at 26.93%

Above $250,000 is taxed at 30.08%There are lots of ways to connect the poll results, and without more data, the three-bracket result is the simplest. We could add a fourth bracket to make things a bit more realistic. For example, if we added a 10% bracket at around $18,000, then a 20% bracket at $28,000, we could push the 27% bracket to $85,000 while leaving $250,000 and over at 30%. That’s just one example.

I didn’t have any larger point I was trying to prove with the poll. I was simply curious about what our readers thought.

-

Thumbs Down to Bristol-Myers Share Repurchase

Eddy Elfenbein, May 5th, 2010 at 1:56 pmI felt the need to do quick post on the news that Bristol-Myers Squibb’s (BMY) board approved a $3 billion share repurchase.

Ugh, these announcements make me groan. I loath share buybacks. After watching company after company waste billions of dollars buying their shares, I’ve come to the conclusion that these repurchases are a waste of time and money. I’d much rather see shareholders get more dividends.

In theory, it’s all the same money—share buyback or dividend—so it shouldn’t make a difference how shareholders are paid. The problem is that the stock market is far too volatile for investors to accurately see the results of a share repurchase.

Cisco (CSCO) is a prime example. The company has wasted several billion dollars buying back its stock. Would the stock have done worse without it? Probably, but I can’t say for certain. However, I absolutely know that shareholders would be wealthier with quarterly dividend checks.

Bristol-Myers is an excellent company and there’s a lot to like about the stock. They just had a very good earnings report. The company pays a quarterly dividend of 32 cents a share which translates to a yield of 5.1%. That’s about 150 points better than a 10-year Treasury.

Let’s look at some of the numbers: Bristol-Myers, like many other healthcare stocks, recently adjusted downward its 2010 earnings forecast due to Obamacare. They now see EPS coming in between $2.15 and $2.25. That means that the quarterly dividend of 32 cents (or $1.28 annualized) is very safe.

On top of that, Bristol-Myers is sitting on a mountain of cash. They have a net cash position of $3.4 billion which comes to $2.02 a share. This means they’re probably a bigger net lender than most banks. In short, they ain’t going bankrupt anytime soon. As a shareholder, wouldn’t it be so much nicer to get a check?

I actually get a little afraid when companies acquire too large a position in cash. This is what I like to call the “Bladder Theory of Corporate Finance.” Little mergers are fine, but mega-mergers are almost always trouble.

What’s most aggravating is that BMY’s board might be making the sensible move. If Congress doesn’t act soon, then dividend taxes are set to nearly triple for high-earners, rising from 15% now to 43.4% in 2013. President Obama wants dividends and capital gains to be taxed at the same level which would hopefully stem the tide of these silly share repurchases. -

The Cyclicals Continue to Plunge

Eddy Elfenbein, May 5th, 2010 at 10:16 amThe trading day is still young but the markets are heading lower and once again, it’s the cyclicals doing most of the damage. The Cyclical Index (^CYC) is currently off -1.29% (it had been more) while the S&P 500 is down -0.56%. The energy stocks seem to be getting hurt the most. Many consumer staples, like Reynolds American (RAI), are actually up on the day.

I’m very happy to see that Nicholas Financial (NICK) is now over $9 a share. Gilead Sciences (GILD) continues to fall and the stock has made another fresh 52-week low. As I’ve said before, trends can last much longer than you thought possible. Remember, it was only a little over one year ago that NICK was going for $1.80 a share (pre-split). -

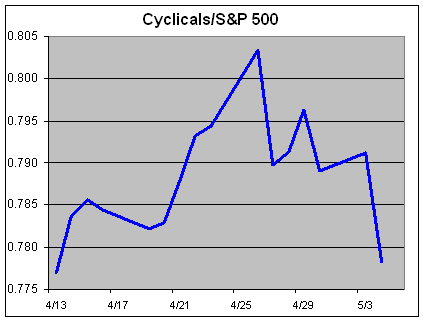

Update on Cyclicals

Eddy Elfenbein, May 4th, 2010 at 11:16 pmTwo weeks ago, I highlighted the fact that cyclical stocks had been on a roll. I was smart enough not to call a peak in cyclical outperformance, but it may have occurred just a few days after my post.

Last Monday, April 26, the ratio of the Morgan Stanley Cyclical Index (^CYC) divided by the S&P 500 broke 0.8 for the very first time and reached an all-time high. Since then, however, cyclicals have underperformed the market and yesterday was an especially ugly day. Since April 26, the S&P 500 has lost -3.17% while the CYC has lost dropped -6.19%. So if you’re a money manager, you can see where you don’t want to be.

It’s still far too early to say whether this is a turn in the cycle. But investors should take notice because once cyclicals start to underperform, the trend can last for a few years.

-

The Onion’s Stockwatch

Eddy Elfenbein, May 4th, 2010 at 7:37 pmAmerica’s Finest News Source:

C

Citigroup

$4.15 $.16 (up 4.0%)

Markets reacted positively to CEO Vikram Pandit’s announcements that the troubled financial titan would soon repay bailout money to the government in the form of a $45 billion prepaid Visa gift card.

GS Goldman Sachs $50.4 $1.23 (up .89%)

A large early-morning protest in front of the company’s headquarters Tuesday led to speculation that Goldman was once again making a lot of money.

BRKB Berkshire-Hathaway (up ) $3,32 $38.9 (+1.18%)

Investors have been aching to get their hands on this hot stock ever since the premiere of Lil Wayne and Birdman’s latest music video in which the two hip-hop icons shower strippers with fistfuls of the conglomerate’s famously high-priced shares. -

Nicholas Financial’s Earnings

Eddy Elfenbein, May 4th, 2010 at 2:08 pmGreat news! NICK made 28 cents a share (adjusting for two cents lost on swaps):

CLEARWATER, Fla., May 4, 2010 — Nicholas Financial, Inc. announced that for the three months ended March 31, 2010, net earnings, excluding change in fair value of interest rate swaps, increased 52% to $3,113,000 as compared to $2,048,000 for the three months ended March 31, 2009. Per share diluted net earnings, excluding change in fair value of interest rate swaps, increased 44% to $0.26 as compared to $0.18 for the three months ended March 31, 2009. See reconciliations of the Non-GAAP measures below. Revenue increased 8% to $14,256,000 for the three months ended March 31, 2010 as compared to $13,224,000 for the three months ended March 31, 2009.

For the year ended March 31, 2010, net earnings, excluding change in fair value of interest rate swaps, increased 80% to $10,228,000 as compared to $5,673,000 for the year ended March 31, 2009. Per share diluted net earnings, excluding change in fair value of interest rate swaps, increased 74% to $0.87 for the year ended March 31, 2010 as compared to $0.50 for the year ended March 31, 2009. See reconciliations of the Non-GAAP measures below. Revenue increased 6% to $56,472,000 for the year ended March 31, 2010 as compared to $53,102,000 for the year ended March 31, 2009.

According to Peter L. Vosotas, Chairman and CEO, “Our positive results for the fourth quarter and year were favorably impacted by a solid increase in revenues and a reduction in the net charge-off percentage of 41% and 26% for the three and twelve months ended March 31, 2010, respectively. We plan to open three to five new branch locations this year and will continue to evaluate additional markets for future branch locations.”Wow, the provision for credit losses dropped to 3.01%!! That’s huge! That’s the lowest since September 2007. This was another very good quarter for Nicholas.

Let’s run through some of the numbers. Most of my forecasts were pretty close to the mark. Average receivables rose to $229.4 million. I said to expect $230 million. Revenue was $14.2 million. I was expecting $14.5 million.

I pegged interest expense to rise to 2.4% but it rose even higher to 2.66%. However, NICK’s debt actually fell from last quarter so total interest expense was $1.5 million. I was expecting $1.4 million.

Even though I was slightly overly optimistic on those projections, I was too pessimistic on the provision for credit losses. I thought it would fall to 4.8%. Instead, it fell all the way to 3.01%. That made all the difference.

Twenty-eight cents is great news. Congratulations to everyone at Nicholas. This was a job well done.

The company made $3 million in three months. Now that cash can be used to grow the portfolio or pay down debt. If they keep this up, then NICK should easily make $1.10 for this calendar year.

For stat geeks, here are the numbers. -

The World’s Simplest Portfolio

Eddy Elfenbein, May 4th, 2010 at 12:39 pmScott Adams of Dilbert fame gives us his suggestion for the World’s Simplest Portfolio (“that is better than what the average money managing expert might concoct”).

He suggests half in the Vanguard Total Stock Market ETF (VTI) and half in the Vanguard Emerging Market ETF (VWO).

That’s not bad, but I can make it even simpler—put all of your money is a Treasury set for the date you need the money. Simple, right? Even better, use a zero-coupon Treasury which is like automatically reinvesting your dividends.

You can skip the transaction costs by buying the bond right from the Treasury. Your default risk is nil.

There’s a chance that you might not perform as well as the market as a whole, but over the past few decades, the equity premium hasn’t been much to write home about. Plus, most of the premium would be eaten away by expenses, even tiny ones from Vanguard.

If you were to design a ratio of Performance-to-Headaches, this portfolio is hard to beat.

This chart above shows how the two ETFs Adams recommends have performed, plus the American Century Target 2025 fund which I’m including as a proxy for long-term Treasuries.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His