Author Archive

-

How the Toxic Assets Were Magnified

Eddy Elfenbein, May 3rd, 2010 at 9:28 amOne of the interesting aspects of the financial crisis is how a relatively small sector of the mortgage housing market — subprime — was able to infect the entire financial system. The WSJ has a very good article explaining how this was done (warning, it’s a little on the wonky side):

In a memo last week, panel Chairman Sen. Carl Levin (D., Mich.) said Goldman’s work “magnified the impact of toxic mortgages” by replicating mortgage securities in debt pools known as collateralized debt obligations as well as CDO derivatives, and also in an index that tracks subprime bonds.

The subprime mortgages that caused big losses generally were packaged into CDOs, in which dozens of mortgage-backed bonds were pooled together and slices of the CDOs were sold to investors. Another version of these CDOs didn’t contain actual mortgage bonds but were linked to them via derivatives called credit-default swaps. Through the use of derivatives, banks created many of these synthetic CDOs using the same mortgage securities, all of which would rise or fall in value depending on how the mortgages were performing. With synthetic CDOs, those who had bet that the loans would perform well were on the hook if their performance deteriorated.

In effect, the documents said, Wall Street was “copying and pasting” what turned out to be the worst-performing securities of the mortgage boom. Such activity helped multiply opportunities for hedge funds and traders who wanted to short the housing market, but magnified the losses of those on the other side of the trades. To short a trade, in this instance, is to bet the housing market will turn down.In the Washington Post, Heidi Moore takes on the silly notion that only sophisticated were hurt:

It’s not just the big clients, however, that get hurt. What Wall Street would like to ignore when it is taking bets in its casino is that a big pile of chips on the table come from regular consumers — from their bank deposits, retirement accounts, credit-card balances, car loans and mortgages. That’s why the distinction between these sophisticated investors and everyone else is nonexistent. When Wall Street banks omit information and draw profits from “institutional investors,” that means they are taking money from your pension funds, your school endowments, and your city and state governments. Other sophisticated investors include hedge funds, which take money from those pension funds, or private-equity funds, which own companies that employ 10 percent of all Americans.

Pension funds, for instance, are considered “sophisticated investors” on Wall Street. But those are just pools of retirement money owed to workers. The pension funds, looking to expand their stash, invest in stocks and bonds sold by Wall Street. These pension funds also give their money to other funds, such as hedge funds and private equity funds, that invest that money in riskier investments, perhaps troubled companies or distressed mortgages. Pension funds play the Wall Street game to score a healthy return — but when they lose, the money lost belongs to regular people. -

Weekend Poll

Eddy Elfenbein, May 1st, 2010 at 5:15 pmIn honor of May Day, here’s a weekend tax poll:

-

Barron’s on Johnson & Johnson

Eddy Elfenbein, May 1st, 2010 at 5:07 pmBarron’s gives some love to one of my favorite Buy List stocks, Johnson & Johnson (JNJ). Here’s an excerpt:

One of the health-care giant’s biggest virtues is its prodigious ability to generate cash. That has helped keep its debt load low. Johnson & Johnson is one of just four U.S. industrial companies with a coveted AAA rating from Standard & Poor’s. (The others: Automatic Data Processing, Exxon Mobil and Microsoft.) At the end of 2009, the company had about $14 billion in debt, compared with shareholder’s equity of $50.6 billion. Cash flow from operations came to $16.6 billion last year, up from about $15 billion in 2008. Cash and equivalents weighed in at $15.8 billion on Dec. 31.

The company is devoting some of its cash to its quarterly dividend, which it boosted 10.2% last month, from 49 cents a share to 54 cents — marking the 48th straight annual payout increase. At $2.16 a year, the yield is a very healthy 3.3%. Bill McMahon, president of ThomasPartners, an investment advisory firm in Wellesley, Mass., with a stake in the company, says consistent dividend increases are “a good directional signal of future returns.”

Another priority is buying back stock. In 2007, the board authorized the repurchase of as much as $10 billion in shares; $9 billion worth has been reacquired so far.

The cash hoard also helps Johnson & Johnson to buy companies, typically for $1 billion or less, to expand its product lines or get into new ones. For example, J&J paid $1 billion last July for an 18.4% equity stake in the biotech company Elan (ELN). In exchange, it got access to substantially all of Elan’s anti-Alzheimer’s products, including bapineuzumab, a promising drug now in Phase III trials.

In its quest to come up with new products, Johnson & Johnson pumped nearly $7 billion into R&D last year, even as it was restructuring its operations, an action expected to trim up to $1.7 billion in annual pretax costs. The company has intensified its effort to fatten its margins, which slid in recent years as patents expired on highly profitable prescription drugs. An encouraging sign: In the first quarter, selling, marketing and administrative expenses equalled 30.5% of sales, down from 30.7% a year earlier. -

Let Greece Default?

Eddy Elfenbein, April 30th, 2010 at 11:03 pmA Harvard economist says yes.

Rather than bail out Greece, therefore, the E.U. and IMF should allow it to default. This will hurt Greece’s creditors, but those entities assumed the risk when they loaned to a country long known for its profligate ways. In contrast, a bailout forces unwitting taxpayers to foot the bill for Greece’s sins. This can only breed resentment, not to mention reduced incentives for other countries to restrain their own spending.

If Greece does default, its economy may suffer in the short term. External credit will be scare to non-existent, so Greece will have to live within it means. This will require slashed pay-scales and benefits for civil servants and drastic cuts in the number of such jobs. It will also require the repeal of Byzantine regulation, burdensome taxes and policies that force a large fraction of the population to feed at the public trough.

But however painful this adjustment may be, it is unavoidable if Greece wants to join the first rank of nations; current policies are unsustainable from every perspective, so the sooner Greece abandons them the better. -

Mississippi Fred McDowell

Eddy Elfenbein, April 30th, 2010 at 2:46 pmIt’s a gorgeous day here in our nation’s capital. I think I’ve had enough of earnings reports, Senate committees and weasely bankers for one week. I’m closing the laptop, shutting off CNBC and turning over the festivities to Mississippi Fred McDowell. Enjoy.

-

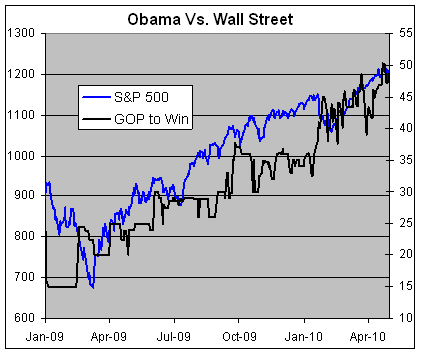

Is the Stock Market Anti-Obama (or Vice Versa)?

Eddy Elfenbein, April 30th, 2010 at 2:30 pmAs the S&P 500 has climbed steadily upward over the past 14 months, so have the prospects for House Republicans.

Here’s a look at the S&P 500 along with the Intrade contract for the GOP to win the House of Representatives this fall.

Just recently, the GOP’s contract hit 50 for the first time. For the record, I don’t think it means anything. Both the state of the GOP and the stock market had just gotten battered, and both have regressed to the mean. That’s all that’s going on.

I’ve tried to warn investors not to read every bump and tick in the market as a political statement (see Kudlow, Larry for details).

But still, it’s an interesting correlation. -

You Know that Goldman Rally…Yeah, About That

Eddy Elfenbein, April 30th, 2010 at 1:48 pm

Last week, I said to stay away from Goldman Sachs (GS) believing it was a value trap. The share had a brief rally but that came to a halt today.Goldman’s Shares Plunge on Inquiries and Downgrades

Already facing investigations on two fronts into its practices in the mortgage market, Goldman Sachs came under pressure from investors as well on Friday.

After reports on Thursday evening that federal prosecutors had opened an investigation into trading at Goldman, raising the possibility of criminal charges against the Wall Street giant, the firm’s stock was downgraded on Friday by two analysts. Standard & Poor’s lowered its rating from hold to sell, and Bank of America Merrill Lynch dropped its rating from buy to neutral, citing the mounting investigations.

Investors responded by sending the stock down 9 percent in midday trading, to $145.89, contributing to an overall decline in financial shares on Wall Street.The downgrade from BofA is noteworthy because it’s so rare. It’s funny how these investment houses are so reticent about downgrading each other.

By no means am I suggesting collusion. Heavens no, dear reader!! All I’m saying is that 1+1 equals something somewhere between 1.99 and 2.01. Any other inference you draw is entirely yours. -

Earnings for Fiserv and Moog

Eddy Elfenbein, April 30th, 2010 at 11:21 amWe had two more earnings reports from our Buy List. After yesterday’s closing bell, Fiserv (FISV) said it made 95 cents per share for the first quarter which was a penny below Wall Street’s consensus (some services the consensus at 97 cents). The stock is getting hit by about 6.6% in today’s trading.

Frankly, I’m not too worried about a pullback in Fiserv. The stock has had a good run so some profit-taking is to be expected. The most important news in yesterday’s report is that the company stuck by its full-year EPS forecast of $3.96 to $4.07. My forecast is for $4.05.

Let’s remember what Barron’s said recently about Fiserv:Because Fiserv’s business is so steady, many investors value it on free cash flow, which has exceeded reported earnings in recent years — a favorable trend. Free cash flow hit $668 million in 2009, up from $603 million in ’08. The company is guiding Wall Street to expect more than $700 million this year. With a market value of $8.2 billion, investors are getting a free-cash-flow “yield” of nearly 9%, at a time when corporate-bond investors are happy to accept 5% or 6%. The stock historically has traded above 14 times free cash flow. With nearly $5 a share of free cash penciled in for 2011, that multiple suggests a price target near 70.

I agree.

Moog‘s (MOG-A) earnings report caught us by surprise. We knew it was coming soon, but didn’t realize it was today.

Nevertheless, the company reported earnings of 55 cents a share which was three cents better than Wall Street’s expectation. Moog made 55 cents per share in the same quarter one year ago.

This was the second quarter of Moog’s fiscal year. Overall, the company’s earnings are bouncing back nicely. In 2008, they earned $2.75 per share and that dropped to $1.98 per share last year. Last November, Moog said to expect EPS for this fiscal year between $2.15 and $2.35. They reiterated that in February. Today, Moog said it now expects $2.35 per share, so that’s good news.

This is from the company’s press release:The Company’s twelve month backlog of $1.1 billion is up over 20% from a year ago.

The Company has updated its guidance for the year. Sales for the year will be down very slightly from $2.12 billion to $2.1 billion, but the Company increased its forecast for net earnings and earnings per share. Net earnings are now projected at $107.4 million and earnings per share at $2.35, an increase of 19% over the previous fiscal year.

“The Company’s second quarter results exceeded our plan, particularly in Aircraft and in Space and Defense,” said R.T. Brady, Chairman and CEO. “Our Components Group delivered another solid performance. Wind energy and Medical Devices sales are developing a little more slowly than we’d planned but both show signs of improvement. The overall result will be a year better than our original forecast and we’re now forecasting a 19% improvement in earnings per share.”Although it’s one of the quietest stocks on the Buy List, Moog is having a very good year. The shares are up over 30% for us and the year is only one-third over.

Both Moog and Fiserv are excellent buys. -

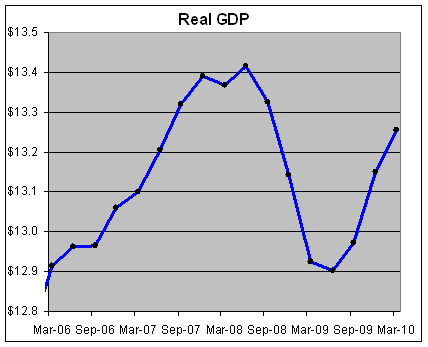

The Economy Grew by 3.2% for the First Quarter

Eddy Elfenbein, April 30th, 2010 at 9:34 amThe government reported that the economy grew by 3.2% for the first quarter. Normally, that’s not so bad but for coming out of a deep recession, it’s very unimpressive.

Federal government spending, which includes remaining stimulus money, grew at an annualized rate of 1.4 percent in the first quarter of 2010. But this was more than offset by continued spending cuts from state and local governments, whose spending decreased 3.8 percent. It was the third quarter in a row in which state and local spending fell.

“Government spending contracted, for all the ballyhoo about stimulus,” said John Ryding, chief economist at RDQ Economics. “This recovery is going to have to stand on the backs of private-sector demand, not on government demand, given all the current fiscal challenges.” Even though any pickup in business is welcome, modest improvement may not be enough to alleviate the pain caused by the so-called Great Recession, many economists say.

The nation’s gross domestic product — a broad measure of goods and services produced in the country — is far below its potential, according to economists’ projections of where the economy would have been if it followed its long-term trend. Output would need to grow at least 5 percent annually for several years to get back on track — and perhaps more importantly, to lead to enough job creation to employ the 15 million Americans already out of work and the 100,000 new workers joining the labor force each month.Earlier this week, I took a stab at giving a letter name to this recovery. My guess for Q1 was pretty close but a tad too high (I had 3.5% instead of 3.2%). Here’s the up-to-date chart:

Thanks to several emailers, I’m going to call it an N-Shaped recovery.

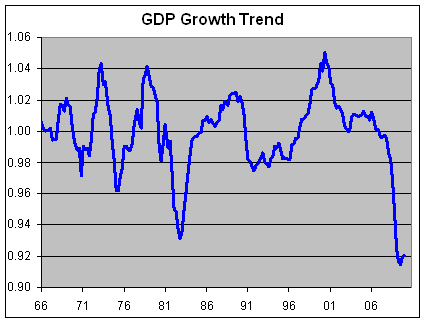

Here’s a more sobering way to look at GDP. This chart shows real GDP divided by a trendline growing at 3.08% which is about the long-term rate of growth.

In other words, this shows you how well GDP is doing compared with its historic growth rate. We’ve fallen off a cliff and are in the process of splatting.

In previous recessions, the economy has snapped back sharply to its historic trendline (1.0 on the chart). By growing at 3.2% last quarter, the economy is barely making headway.

At 0.92, we’re 8% below the trendline. This is what the NYT means by growing at 5% for a few years to get back on track. If the economy grew by 5% a year — 2% higher than the long-term trend — for four years, then we’d finally get back to something resembling normal. -

Behold!

Eddy Elfenbein, April 29th, 2010 at 3:09 pmWhen Alexander saw the breadth of his domain he wept for there were no more worlds to conquer.

In other news:

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His