Author Archive

-

Kling on the Senate Hearings

Eddy Elfenbein, April 28th, 2010 at 9:41 amArnold Kling sums it nicely:

Too bad somebody at Goldman could not have called out a Senator. It must have been tempting to say, “Look. You can’t make a market by bending over backwards giving buyers every reason not to buy and sellers every reason not to sell. Sophisticated investors understand how we operate. Just like everybody who goes to play blackjack understands that some of the cards are dealt face down. You can complain that you think all the cards should be face up, but that would totally change the game. Do you hold to such high standards in your election campaigns? Do you think your disclosure of the consequences of your votes is honest? Do you disclose how lobbyists told you to vote? Do you go out of the way in your campaigns to give people all the possible reasons not to vote for you? You want to tell me about my responsibility to my clients? How would you like to hear my opinion about your responsibility to your constituents?”

-

AFLAC’s Earnings

Eddy Elfenbein, April 27th, 2010 at 4:17 pmAfter the bell, AFLAC (AFL) reported first-quarter operating earnings of $1.41 per share. With insurance companies, it’s more important to focus on operating earnings since net earnings can be heavily influenced by investments. The Street was looking for $1.32.

This is what AFL had to say about guidance:With one quarter of the year complete, we continue to believe we are positioned for another year of solid financial performance. Although challenges posed by weak economic conditions clearly persist, particularly in the United States, we still believe our goal for increasing operating earnings per diluted share is reasonable and attainable. As such, our goal remains an increase of 9% to 12% this year in operating earnings per diluted share, excluding the impact of the yen. If the yen averages 90 to 95 to the dollar for the full year, we would expect reported earnings to be in the range of $5.24 to $5.56 per diluted share. Using that same exchange rate assumption, we would expect second quarter operating earnings to be $1.33 to $1.38 per diluted share.

The stock is at $52.41 and they see full-year EPS coming in between $5.24 and $5.56. That’s a forward P/E Ratio of 9.4 to 10. AFLAC is a very good buy.

-

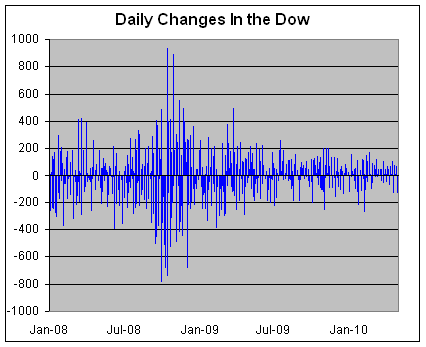

Putting Today In Perspective

Eddy Elfenbein, April 27th, 2010 at 3:30 pmThe Dow is off about 150 right now. I see that people are concerned.

My how we forget what real volatility looks like!

Here’s a look at the daily changes in the Dow since the beginning of 2008:

Update: The Dow closed down 213 points. -

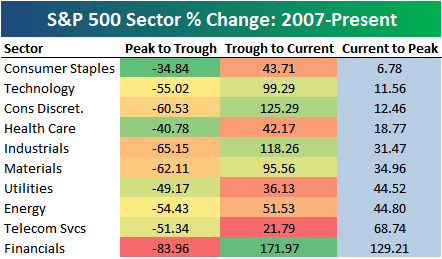

Sector Performance

Eddy Elfenbein, April 27th, 2010 at 2:42 pmBespoke has a handy round-up of how the S&P 500 sectors have performed over the past few years:

The important lesson for investors is to see how much less volatile the consumer staples are (these are the stocks that are the opposite of cyclicals). Staples tend to fall the least and rally the least.

Here’s a listing of the 41 stocks in the S&P 500’s Consumer Staples sector. I’ve included each stock’s dividend yield:ADM Archer-Daniels-Midland 2.13% AVP Avon Products 2.67% BF-B Brown Forman 2.05% CAG ConAgra Foods 3.27% CCE Coca-Cola Enterprises 1.27% CL Colgate-Palmolive 2.52% CLX Clorox 3.12% COST Costco 1.21% CPB Campbell Soup 3.12% CVS CVS Caremark 0.96% DF Dean Foods 0.00% DPS Dr Pepper Snapple 1.79% EL Estee Lauder 0.83% GIS General Mills 2.81% HNZ H.J. Heinz 3.68% HRL Hormel Foods 2.14% HSY The Hershey Company 2.71% K Kellogg 2.84% KFT Kraft Foods 3.90% KMB Kimberly-Clark 4.33% KO Coca-Cola 3.31% KR Kroger 1.65% LO Lorillard 5.11% MJN Mead Johnson Nutrition 1.78% MKC McCormick & Company 2.65% MO Altria Group 6.66% PEP Pepsico 2.79% PG Procter & Gamble 3.05% PM Philip Morris 4.73% RAI Reynolds American 6.69% SJM J.M. Smucker 2.26% SLE Sara Lee 3.19% STZ Constellation Brands 0.00% SVU SuperValu 2.34% SWY Safeway 1.57% SYY Sysco 3.24% TAP Molson Coors 2.22% TSN Tyson Foods 0.81% WAG Walgreen 1.57% WFMI Whole Foods Market 0.00% WMT Wal-Mart Stores 2.23% -

Watch The Senate Hearings Live

Eddy Elfenbein, April 27th, 2010 at 9:55 amYou can see the Senate testify before Goldman Sachs here.

Wait, I might have that backwards. It’s getting hard to tell.

Here are live blogs from:

TBI

WSJ

NYT

FT

Reformed Broker

Dealbreaker

Guardian

Simon Johnson at PBS

This is a perfect opportunity for a Godfather 2-like scene when Frank Pentangeli testified before the Senate. Fab starts reading his testimony and Blankfein walks in with Fab’s brother Olivier and takes a seat in the back row. Then Fab suddenly recants: “Abacus? I never heard of an Abacus.” -

Wright Express’ Earnings

Eddy Elfenbein, April 27th, 2010 at 9:32 amOne more Buy List stock reported earnings this morning. Wright Express (WXS) said it earned 61 cents per share for its first quarter which was four cents better than Wall Street’s expectations. In February, Wright said to expect Q1 earnings between 53 and 58 cent per share so they’re doing even better than their own forecasts. The company’s revenues rose 22.3% to $83.8 million which was just shy of expectations.

Wright said that Q2 earnings should range between 61 and 66 cents per share. For all of 2010, Wright sees earnings-per-share coming in between $2.39 and $2.54. This is a big increase from the earlier range of $2.26 to $2.46.

Bottom line: This was a very good report. The strange thing about Wright is why its shares didn’t do anything for the first few months of the year. Going back to last September to up until a few weeks ago, WXS mostly bounced between $28 and $32. Then two weeks ago, out of the blue, WXS started to break out. Who knows what traders are thinking? The shares are down again this morning. That’s OK, I can deal with folks who don’t see a bargain. Wright Express continues to be an excellent buy.

After the closing bell, AFLAC (AFL) is due to report. This is one of my favorite Buy List stocks. The consensus estimate is that AFLAC will earn $1.32 a share.

-

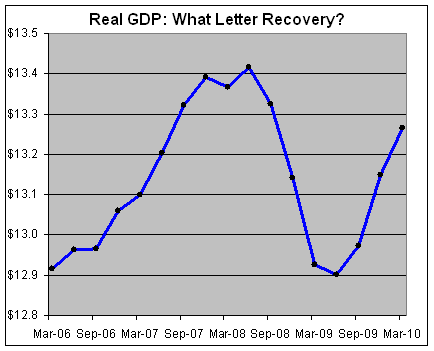

What Letter Would You Give This Chart?

Eddy Elfenbein, April 26th, 2010 at 1:45 pmOn Friday, the government will release its initial report on first-quarter GDP growth. The economy has grown for the last two quarters but it’s been far short of what should be expected when you emerge from a nasty recession.

Economists and market-watchers are debating what letter the recovery will look like — will it look like a V, a U or possibly a W? Here’s what the Real GDP chart looks like, but I’ve added a guess for Friday’s data point (3.6% growth).

To me it looks like a U. Or maybe a backwards J. I dunno. Possibly another letter? -

Buy List Earnings This Week

Eddy Elfenbein, April 26th, 2010 at 12:52 pmFive of our Buy List stocks will report earnings this week. Here they are along with Wall Street’s consensus:

AFLAC AFL 27-Apr $1.32 Wright Express WXS 27-Apr $0.57 SEI Investments SEIC 28-Apr $0.27 Becton, Dickinson BDX 29-Apr $1.23 Fiserv FISV 29-Apr $0.97 -

What If the Fed Delivers a Surprise Rate Increase?

Eddy Elfenbein, April 26th, 2010 at 11:38 amThe stock market continues to climb. The S&P 500 has made up all it lost after the Goldman news, and we’re on our way to the highest close since Lehman Brothers went belly up.

My feeling has been that as long as interest rates are low and profits are growing, then the market will rally. Still, the market is nearing B-Day. This will be the day when Ben Bernanke and the Federal Reserve finally decide to raise interest rates. The futures market currently thinks the Fed will have rates at 0.25% sometime this summer (that’s really not much of an increase since the current range is 0% to 0.25%) and 0.5% by the end of the year.

But what if the Fed decides to surprise everyone by raising rates by 50 basis points or more before? This would be a dramatic move. Gold would plunge and the stock rally might halt in place. The benefit for the Fed is that it’s not much of a move but it would send a strong signal to investors that the economy is getting better and that the central bank is determined to unwind its dramatic policy moves of the past two years.

I doubt a surprise rate hike would have a long-term impact of stock prices, but it would certainly change the tone of the market. A surprise hike is a long shot, but it’s not out of the question. No one can ignore the fact that earnings have been improving quite dramatically. This has been a great earnings season so far. Profits are running 22% ahead of estimates and this is leading analysts to raise their forecasts:The earnings upgrades come as income beats Wall Street estimates at the fastest rate ever for the third time in four quarters. More than 80 percent of the 173 companies in the S&P 500 that reported results have topped estimates, compared with 79.5 percent in the third quarter and 72.3 percent in the three- month period before that, Bloomberg data show.

It looks very likely that the S&P 500 is on track to earn $80 for 2010 and possibly $95 for 2011. That’s my view but UBS is even more optimistic. They just upgraded their target for the S&P 500 to 1,350. They see EPS coming in at $92 for this year and $100 for 2011. UBS writes: “Moreover, the “junk trade” has re-emerged, with the most economically-sensitive companies and lower quality stocks outpacing the broader market.”

This is exactly what I noted last week.

One final note, Netflix (NFLX) is up another $8 a share today. I think I know how this story ends. I just don’t know when the last act will start. -

Barron’s: Fiserv Could Jump 20% From Here

Eddy Elfenbein, April 26th, 2010 at 7:32 amFiserv (FISV), one of our Buy List stocks, gets some love from Barron’s:

Earnings are on track to rise to $4 per share this year from $3.66 in 2009, and to gain nearly 10% in 2011 to $4.44, placing the price/earnings multiple at 13.4 times 2010 projections and 12.1 times 2011 expectations. (Per-share earnings are reported “as adjusted” for the adding back of goodwill amortization, for a clearer gauge of the underlying business.) This is cheap for such a high-quality, industry-leading business, which merits a multiple equal to or better than the Standard & Poor’s 500’s 15-plus times ’10 forecasts. Also, it suggests at least 20% upside for Fiserv shares.

Because Fiserv’s business is so steady, many investors value it on free cash flow, which has exceeded reported earnings in recent years — a favorable trend. Free cash flow hit $668 million in 2009, up from $603 million in ’08. The company is guiding Wall Street to expect more than $700 million this year. With a market value of $8.2 billion, investors are getting a free-cash-flow “yield” of nearly 9%, at a time when corporate-bond investors are happy to accept 5% or 6%. The stock historically has traded above 14 times free cash flow. With nearly $5 a share of free cash penciled in for 2011, that multiple suggests a price target near 70.The next earnings report is due this Thursday after the bell. The Street is expecting 97 cents per share, up from 88 cents a year ago. Here are the annual EPS results for the past few years:

2003: $1.61

2004: $1.92

2005: $2.31

2006: $2.53

2007: $2.66

2008: $3.29

2009: $3.66

That’s what I like to see — nice steady increases. I think EPS for 2010 will come in around $4.05, give or take. Fiserv is an excellent buy.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His