Author Archive

-

Bed, Bath & Beyond’s Q3 Earnings

Eddy Elfenbein, January 7th, 2009 at 4:20 pmFor their third-quarter (ending November 29), Bed Bath & Beyond (BBBY) just reported earnings of 34 cents a share. That’s pretty ugly, but honestly, it’s not bad considering the crappy environment they’re in. The earnings were a penny below the Street’s consensus, and the company earned 52 cents a share for last year’s Q3. Sales came in at $1.783 billion which was slightly below last year’s Q3. Same-store sales were just ugly, down 5.6%.

The company sees Q4 EPS coming in at 40 to 46 cents which is less than the 49 cents the Street was expecting.

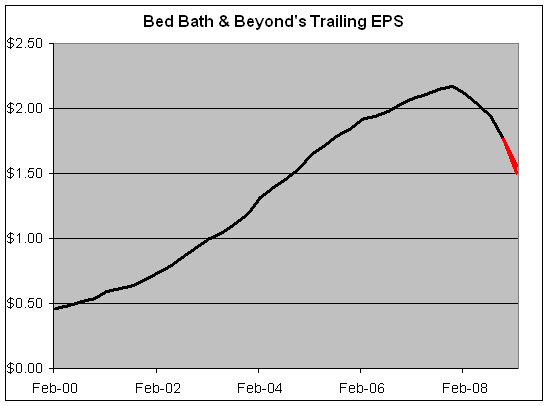

Here are the earnings results going back a few years:Quarter Sales Gross Profit Operating Profit Net Profit EPS $356,633 $146,214 $28,015 $17,883 $0.06 $451,715 $185,570 $53,580 $33,247 $0.12 $480,145 $196,784 $50,607 $31,707 $0.11 $569,012 $238,233 $77,138 $48,392 $0.17 $459,163 $187,293 $36,339 $23,364 $0.08 $589,381 $241,284 $70,009 $43,578 $0.15 $602,004 $246,080 $64,592 $40,665 $0.14 $746,107 $311,802 $101,898 $64,315 $0.22 $575,833 $234,959 $45,602 $30,007 $0.10 $713,636 $291,342 $84,672 $53,954 $0.18 $759,438 $311,030 $83,749 $52,964 $0.18 $879,055 $370,235 $132,077 $82,674 $0.28 $776,798 $318,362 $72,701 $46,299 $0.15 $903,044 $370,335 $119,687 $75,459 $0.25 $936,030 $386,224 $119,228 $75,112 $0.25 $1,049,292 $443,626 $168,441 $105,309 $0.35 $893,868 $367,180 $90,450 $57,508 $0.19 $1,111,445 $459,145 $155,867 $97,208 $0.32 $1,174,740 $486,987 $161,459 $100,506 $0.33 $1,297,928 $563,352 $231,567 $144,248 $0.47 $1,100,917 $456,774 $128,707 $82,049 $0.27 $1,273,960 $530,829 $189,108 $120,008 $0.39 $1,305,155 $548,152 $190,978 $121,927 $0.40 $1,467,646 $650,546 $283,621 $180,980 $0.59 $1,244,421 $520,781 $150,884 $98,903 $0.33 $1,431,182 $601,784 $217,877 $141,402 $0.47 $1,448,680 $615,363 $205,493 $134,620 $0.45 $1,685,279 $747,820 $304,917 $197,922 $0.67 $1,395,963 $590,098 $148,750 $100,431 $0.35 $1,607,239 $678,249 $219,622 $145,535 $0.51 $1,619,240 $704,073 $211,134 $142,436 $0.50 $1,994,987 $862,982 $309,895 $205,842 $0.72 $1,553,293 $646,109 $154,391 $104,647 $0.38 $1,767,716 $732,158 $211,037 $147,008 $0.55 $1,794,747 $747,866 $203,152 $138,232 $0.52 $1,933,186 $799,098 $259,442 $172,921 $0.66 $1,648,491 $656,000 $118,819 $76,777 $0.30 $1,853,892 $739,321 $187,421 $119,268 $0.46 $1,782,683 $692,857 $136,374 $87,700 $0.34 Here’s their trailing four-quarter earnings-per-share. The two red lines show the upper and lower band of the company’s projection.

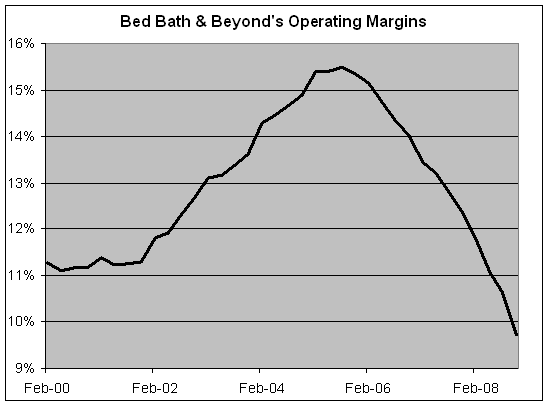

It’s not hard to find the squeaky wheel. Take at look at their operating margins:

That’s based on trailing four quarter numbers. This means the company is doing a lot of price-cutting. -

The End of Times

Eddy Elfenbein, January 7th, 2009 at 11:45 amMichael Hirschorn says the New York Times could go bankrupt, by May.

It’s certainly plausible. Earnings reports released by the New York Times Company in October indicate that drastic measures will have to be taken over the next five months or the paper will default on some $400million in debt. With more than $1billion in debt already on the books, only $46million in cash reserves as of October, and no clear way to tap into the capital markets (the company’s debt was recently reduced to junk status), the paper’s future doesn’t look good.

“As part of our analysis of our uses of cash, we are evaluating future financing arrangements,” the Times Company announced blandly in October, referring to the crunch it will face in May. “Based on the conversations we have had with lenders, we expect that we will be able to manage our debt and credit obligations as they mature.” This prompted Henry Blodget, whose Web site, Silicon Alley Insider, has offered the smartest ongoing analysis of the company’s travails, to write: “‘We expect that we will be able to manage’? Translation: There’s a possibility that we won’t be able to manage.” -

Mean Automakers Dash Nation’s Hope For Flying Cars

Eddy Elfenbein, January 6th, 2009 at 4:56 pm -

Earnings Preview: Bed Bath & Beyond

Eddy Elfenbein, January 6th, 2009 at 1:20 pmBed Bath & Beyond Inc. reports results for its fiscal third quarter on Wednesday. The following is a summary of key developments and analyst opinion related to the period.

OVERVIEW: In early December, Bed Bath & Beyond pre-released results for the third quarter, saying same-store sales slipped amid a tough economic climate and liquidation sales by a major competitor.

The Union, N.J.-based housewares retailer it expects earnings to range between 31 cents and 35 cents per share for the quarter ended Nov. 29. That’s down from previous guidance of 41 cents to 47 cents a share the company gave in September. It also represents a drop from 2007, when the company earned 52 cents a share in the same period.

The company said its net sales for the quarter fell 0.7 percent from the same period the previous year, when it reported sales of $1.79 billion.

Same-store sales for the quarter declined about 5.6 percent. Same-store sales, or sales at stores open at least a year, are a key indicator of a retailer’s health because they measure revenue at existing locations rather than newly opened ones.

During the quarter, the retail chain saw shares sink to an eight-year intraday low as government figures show home furnishing sales fell.

BY THE NUMBERS: Analysts polled by Thomson Reuters estimate a profit of 33 cents per share on revenue of $1.79 billion for the quarter.

ANALYST TAKE: After the retailer pre-released lower-than-expected third quarter figures in early December, analysts said the company was facing increasing pressure from a difficult sales environment and the ongoing bankruptcy liquidation sales of items by competitor Linens ‘N Things.

“While we expect consumer spending will likely remain weak, Bed Bath & Beyond may well be one of the few retailers to show earnings growth next year,” SunTrust Robinson Humphrey analyst David Magee told investors in early December. “Moreover, once the macro environment improves, Bed Bath & Beyond should emerge stronger than most and could benefit from some ongoing consolidation in the space along the way.”

WHAT’S AHEAD: Investors will be looking for an update on how the company’s holiday sales fared and more details about what executives expects business trends to be in the coming year.

STOCK PERFORMANCE: During the quarter, which ended Nov. 29, shares fell about 34 percent to end the period at $20.29. -

Where Do You Place Johnny Cash?

Eddy Elfenbein, January 6th, 2009 at 12:11 pmTyler Cowen asks: “Where is the geographic center of Johnny Cash’s moral and musical universe?”

I’m particularly pleased with my answer. Johnny Cash walks the line. -

More Financial History

Eddy Elfenbein, January 6th, 2009 at 12:06 pmThe Economist opens its vault:

Having fully admitted the disappointments, we find some justification for regarding 1928 as a year of no small promise for the future. Quite possibly it will be remembered in history as a year in which the foundations of recovery were laboriously laid.

-

Iceland to Sue Britain

Eddy Elfenbein, January 6th, 2009 at 11:05 amFrom the 1950s through much of the 1970s, Britain and Iceland were involved in the Cod Wars, which was an overgrown fishing dispute. Now the financial mess has brought these two rivals back to confrontation.

Iceland’s state-run Kaupthing bank will sue the British government for its decision to force the bank’s British subsidiary into a form of bankruptcy, the Icelandic Prime Minister’s office said Tuesday.

The committee appointed to run Kaupthing — which collapsed last autumn — is taking Britain to court because it forced the unit Kaupthing Singer & Friedlander into administration at the height of Iceland’s financial crisis, according to the prime minister’s press secretary, Kristjan Kristjansson.

”They are suing on the grounds of the actions taken by the Financial Services Authority,” Mr. Kristjansson told The Associated Press.

The F.S.A., Britain’s financial regulator, swooped in to protect British depositors shortly after Iceland’s banking sector fell under the weight of its bad debts, removing savings accounts from Kaupthing Singer & Friedlander and seizing assets from another Landsbanki, another Icelandic bank.

Britain said the moves were necessary to safeguard British savers’ deposits, but the actions strained relations between the north Atlantic neighbors. Iceland has repeatedly threatened to sue over the matter.

It was not clear whether damages would be sought in the Icelandic suit. The F.S.A. and Britain’s treasury did not immediately return requests for comment.

Prime Minister Geir Haarde said Monday that his government supported the lawsuit and could help fund it.

”We think that it is very important that we ascertain if U.K. laws were misused against Icelandic interests,” he said.Honestly, it’s hard for me to read that last sentence without laughing.

-

The Price of Forecasts

Eddy Elfenbein, January 6th, 2009 at 12:28 amHere’s Paul Farrel highlighting absurdly bullish forecasts from 10 years ago. Let me again make my claim that overly bullish forecasts are routinely held to account, but absurdly bearish ones are rarely held accountable.

Here’s some advice: If you ever go in the econ-predictions biz, be pessimistic and vague. Then claim anything that goes wrong as something you predicted.

By the way, are we allowed to start making fun of this? -

Prepayments and the Subprime Market

Eddy Elfenbein, January 6th, 2009 at 12:01 amHere’s the abstract of a recent paper:

This paper demonstrates that the reason for widespread default of mortgages

in the subprime market was a sudden reversal in the house price appreciation of

the early 2000s. Using loan-level data on subprime mortgages, we observe that

the majority of subprime loans were hybrid adjustable rate mortgages, designed

to impose substantial fi nancial burden on reset to the fully indexed rate. In a

regime of rising house prices, a fi nancially distressed borrower could avoid default

by prepaying the loan and our results indicate that subprime mortgages originated

between 1998 and 2005 had extremely high prepayment rates. Most important,

prepayment rates on subprime mortgages were extremely high (i) not just for ARMs

but FRMs as well, (ii) even before the reset dates on hybrid-ARMs and (iii) despite

prepayment penalties on the contract. However, a sudden reversal in house price

appreciation increased default in this market because it made this prepayment exit

option cost-prohibitive. In short, prepayments sustained the subprime boom and

the extremely high default rates on 2006-2007 vintages were largely due to the

inability of these mortgages to prepay (an option that was available for mortgages

of earlier vintages). -

Two Days in 2009 and We’re Kicking Butt

Eddy Elfenbein, January 5th, 2009 at 11:16 pmWith two days under our belt, the Buy List already has a lead over the S&P 500, 4.12% to 2.68%. Obviously, a two-day lead doesn’t mean much, but I mention it because the Buy List was helped out enormously today by the 27.7% jump in Nicholas Financial (NICK).

Since NICK is such a low-priced stock, the bid/ask spread can make a big difference on how well the Buy List does each day. Some days we’re punished, but some days, like today, it’s a big, big help.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His