Author Archive

-

Time to Ditch the Extra-Point?

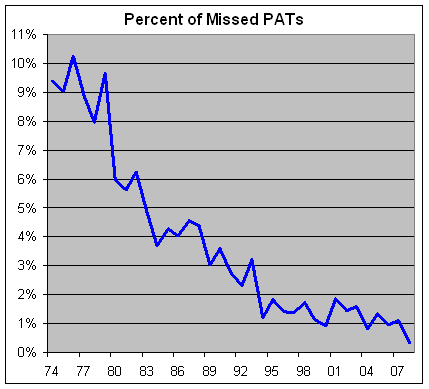

Eddy Elfenbein, December 2nd, 2008 at 10:23 pmExtra-points are getting out of hand this year. The PAT success rate is normally very high, but this year it’s reaching absurd levels. Through week 13, only 3 extra-point attempts failed out of 884 tries. That’s a success rate of 99.66%. Sheesh, that’s even higher than Ivory Soap.

Sorry, but anything that consistent isn’t a game anymore. To put it in context, the number of missed PATs is down by about 90% from 20 years ago. Remember, football is a game. That means it’s supposed to be, you know, fun to watch. Well, 99.66% ain’t fun to watch. It’s a mockery of sports. The PAT has become a useless play that could only cause injuries.

So should we just get rid of it? Nah, it’s been around forever, so let’s try modifying it.

How about moving the extra-point line back? Well, let’s look at the data. In the 20 to 29-yard range, kickers have made 203 of 206 attempts this year for a 98.54% success rate. I’m assuming that’s a median attempt of 24.5 yards, meaning the line of scrimmage is about the 7 or 8. Remarkably, that lower success rate is still higher than the league’s extra-point success rate until 15 years ago.

One idea would be to move the PAT line back to, say, the 10-yard line. Of course, that would make a two-point conversion much harder. The problem is that the 2-point conversion already can’t compete from the 2-yard line. The success rate runs at 44% which makes it inefficient compared to the 1-point try. The 2 is only used when it has to be. (Do the one- and two-point attempts have to take place at the same place? Hmmm. For simplicity’s sake, I’d say yes).

Here’s a look at the percent of missed PATs going back to 1974 when the NFL moved the goalposts to the back of the endzone. I should note that there have been some rule changes. For example, running “leaps” by the defense were banned in 1984. Cool to watch but probably a bit dangerous.

The rule change I’d support wouldn’t be to move the extra-point line back, but moving it in a little bit. Perhaps to the one-yard line, or maybe the four- or five-foot line. That would make the 2-point try more competitive while having no impact on the 1-point try. Just like in economics, it’s all about incentives.

Update: Brian Burke has more. He says to narrow the goal posts.

-

Hoofy and Boo Win an Emmy

Eddy Elfenbein, December 2nd, 2008 at 10:10 pmCongratulations to everyone at Minyanville:

Minyanville Media, the fast growing financial information and entertainment company, today won a Business and Financial Reporting Emmy for its animated news show “Minyanville’s World in Review with Hoofy and Boo.”

The show was honored by The National Academy of Television Arts and Sciences, in the New Approaches to Financial Reporting category for its groundbreaking weekly show starring the animated icons of finance, Hoofy the Bull and Boo the Bear.

“It is a humbling honor for us, to be recognized as a leader of business news reporting,” said Minyanville Founder and CEO Todd Harrison. “We continue to do our part in helping narrow the gap between what people know about managing their money and what they need to know,” he added. -

Victoria Secret Model Gets all Pottymouth on CNBC

Eddy Elfenbein, December 2nd, 2008 at 3:35 pmSorry for the commercial intro. The clip starts at 16 seconds.

Here’s the clip with Victoria Secret’s CEO. Later, Michelle Caruso Cabrera asks who “did the lovely tease for us.” -

10-Year Yield Drops to 50-Year Low

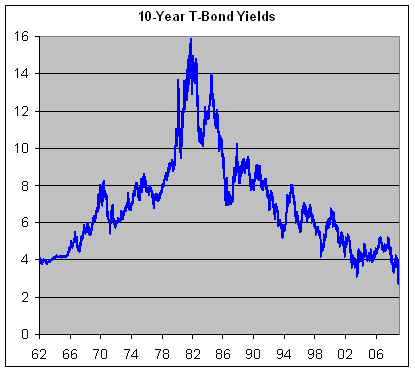

Eddy Elfenbein, December 2nd, 2008 at 12:49 pmThe yield on the 10-year Treasury fell below 2.7%. That’s lowest on the daily records which go back to 1962. The monthly records go back further so it’s the lowest since 1955.

With the S&P 500 currently around 845, this means that index only needs to get to 1073 over the next ten years to beat the Treasury bond. That doesn’t include dividends and the yield on stocks may be higher than 2.7%. (Some in the media have said that the S&P’s yield is already above long-term Treasuries, but I’d rather see how dividend payouts fare in the coming months before I’d say it’s true.) -

Kudlow on the Recession

Eddy Elfenbein, December 1st, 2008 at 4:06 pmFrom December 5, 2007:

The Recession Debate Is Over

There ain’t no recession.

Today’s ADP private jobs survey of 189,000 could produce a 200,000 non-farm payroll job gain for November. I don’t know — these wacky BLS numbers are subject to huge revisions. But the ADP was a huge number. In fact, jobs seem to be picking up major steam from their August low, rising in September and October. And now I’m expecting a good increase in November to be reported by the BLS this Friday.

Plus, profits are stronger than people seem to understand. The ISMs are fine. Productivity, reported out today, soared to over 6 percent annually in the third quarter. That’s the best productivity number in four years for output per person.

On top of that, business inflation is zero. Flat. Nada.

The recession debate is over. It’s not gonna happen. Time to move on.

At a bare minimum, we are looking at Goldilocks 2.0. (And that’s a minimum). The Bush boom is alive and well. It’s finishing up its sixth splendid year with many more years to come. -

Want to Know About Hedge Funds

Eddy Elfenbein, December 1st, 2008 at 2:43 pmDonald MacKenzie in the London Review of Books has a long article on hedge funds:

You could walk around Mayfair all day and not notice them. Hedge funds don’t – can’t – advertise. The most you’ll see is a discreet nameplate or two. An address in Mayfair counts in the world of hedge funds. It shows you’re serious, and have the money and confidence to pay the world’s most expensive commercial rents. A nondescript office no larger than a small flat can cost £150,000 a year. Something bigger and in the style that hedge funds like (glass walls, contemporary furniture) can set you back a lot more. It’s fortunate therefore that hedge funds don’t need a lot of space. Two rooms may be enough: one for meetings, for example with potential investors; one for trading and doing the associated bookkeeping. Some funds consist of only four or five people. Even a fairly large fund can operate with twenty or fewer.

-

Investing During a Recession

Eddy Elfenbein, December 1st, 2008 at 2:24 pmToday, the NBER made news by saying the recession officially started in December 2007. This is the fifteenth recession since 1926.

Of the 82 years from the beginning of 1926 through 2007, 182 months have been in recession which is about 18.5% of the time. During those 182 months, the stock market fallen at an annualized rate of 9.6% (including dividends and inflation).

Of the 802 months of expansion, the stock market has risen at an annualized rate of 11.3%. -

NBER: Recession Began in December 2007

Eddy Elfenbein, December 1st, 2008 at 1:42 pmI was wrong. I thought the National Bureau of Economic Research would date the beginning of the recession in May of 2008. The committee today pinpointed December 2007.

I understand that selection since that’s when employment peaked. The reason for my later date was that GDP numbers continued to look decent through the second quarter. I didn’t think the committee would “overrule” that data, but I guess they did.

NBER Announces December 2007 Peak in Economic Activity

Next question: When will it end?

-

Gasoline Down for 75 Straight Days

Eddy Elfenbein, December 1st, 2008 at 12:04 pmGas prices fell for the 75th consecutive day on Monday, and sold below $2 a gallon in all but three states and the District of Columbia, according to a daily survey of credit-card swipes at gas stations.

Gas prices slipped 0.5 cents to a national average of $1.82 a gallon, the cheapest price since January 2005, according to Monday’s survey from motorist group AAA. That price is $1.24 less than what gas cost on the same day last year.

Gas prices have fallen by more than 55% since hitting a record high of $4.114 a gallon on July 17. Concern about falling fuel consumption in the midst of the current economic crisis has driven the price of oil, a main component of gasoline, down more than 65% since July.

-

Profiting off the Liquidity Preference

Eddy Elfenbein, December 1st, 2008 at 11:14 amOne aspect of this market that I find fascinating is the dramatic yield spreads between short-term Treasury yields (^IRX) and just about everything else. Short-term Treasuries have one major benefit over all other securities and that is their safety. No matter what happens, an investor can be very confident that the U.S. Treasury will pay them back. The Feds, after all, own the printing press.

But what we’re seeing recently is being caused by another advantage of Treasuries and that is their liquidity. The Treasury market is one of the most liquid markets in the world. If need be, Treasuries can be dumped at a moment’s notice for something else. That factor is drawing lots more buyers. The short-term T-bill continues to trade as inches above 0%. Going further out, the 10-year Treasury is now down to 2.8%.

There’s an opposite reaction going on in less-liquid assets. I think this is partly why micro-cap stocks like Nicholas Financial (NICK) are so cheap. There’s an illiquidity discount. In other words, you can’t easily sell when no one is willing to buy. We’re also seeing nearly ridiculous yields for junk bonds.

There are a number of junk bond ETFs. For example, the PowerShares High Yield Corporate Bond (PHB) is yielding 13.8% based on its most-recent monthly dividend payment.

I think we saw a similar “gravitational pull” during the dot.com bubble. When sock puppet companies were going for over 100 times dreams, many high-quality REITs were paying dividends over 12%. The problem was the REITs had kept going down and the dot.coms kept rallying. It seemed as if the breaking point had already passed.

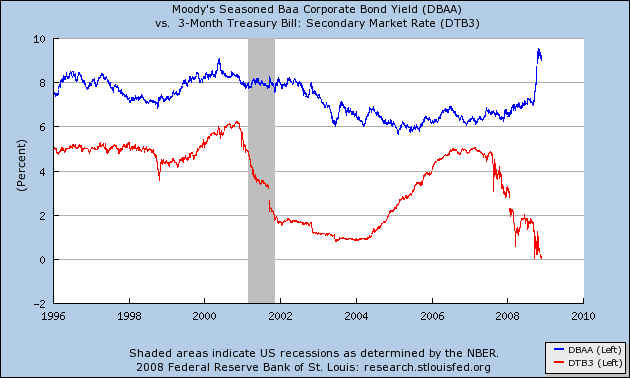

Here’s a look at BAA corporate yields, which still isn’t junk, compared with short-term Treasuries.

One advantage of the liquidity preference would be for the government to issue massive amount of short-term T-bills at their regular auctions. The proceeds could be used to by high-yielding preferred stock is locked-up companies. That way we could use the liquidity premium to the taxpayers’ advantage.

Arnold Kling has more.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His