Author Archive

-

RIP: Georges Yared

Eddy Elfenbein, September 8th, 2008 at 4:54 pmI wanted to express my condolences to the family and friends of Georges Yared. I always enjoyed Georges’ market commentary and found him to be a sane voice in often insane times. He will be missed.

-

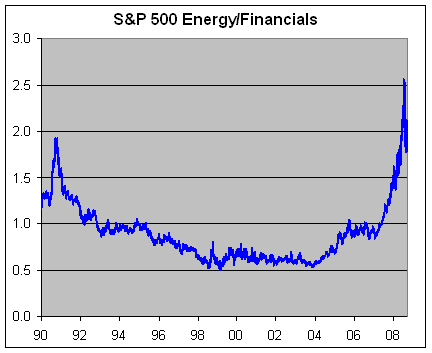

Chart of the Day

Eddy Elfenbein, September 8th, 2008 at 11:32 amHere’s the S&P 500 Energy Index divided by the S&P 500 Financial Index.

-

The Fannie and Freddie Take Over

Eddy Elfenbein, September 8th, 2008 at 11:01 amJohn Hempton at Bronte Capital has an excellent summary of the takeover of Fannie and Freddie. It’s odd to say this, but the markets forced the government’s hand. The WSJ looks at the events leading up to the takeover.

In the end, Fannie Mae and Freddie Mac had no choice.

Summoned to separate meetings on Friday with Treasury Secretary Henry Paulson and other top officials, the two mortgage giants were told they could either agree to a government takeover or one would be foisted upon them.

“We have the grounds to do this on an involuntary basis, and we will go that course if needed,” Mr. Paulson told senior executives at the two companies, who had little idea such a move was coming, according to three people familiar with the meetings.

There was no dramatic trigger, nor was there fear of imminent collapse. Instead, the sweeping government intervention stemmed from a growing realization by Treasury and Federal Reserve officials that the two companies couldn’t survive in their present forms, and that any collapse would be devastating to the economy.

The decision was hashed out over weeks of meetings. They included a conclave of Federal Reserve officials during their annual retreat at Jackson Hole, Wyo.; a mid-August polling of bond-market players by Morgan Stanley bankers advising Treasury; and a marathon session over the Labor Day weekend, fueled in part by Diet Coke and Coke Zero.

Dozens of bankers and lawyers were involved in the process. One junior banker joked that the round-the-clock schedule was tougher than prison — at least there, you got three square meals a day.

In the end, Mr. Paulson, Federal Reserve Chairman Ben Bernanke and James Lockhart, head of the companies’ regulator, the Federal Housing Finance Agency, concluded that the two companies had lost the confidence of the markets and couldn’t survive as currently structured. No one could say how much money from the Treasury, either via a loan or an equity investment, would be enough to get them through the housing mess. Hence, the need for the government to step in and stabilize what has become a vital cog for the housing and mortgage market.I’m not against the government’s move and I see that it had to happen. Don’t believe any of the nonsense that this will “cost the taxpayer” fill-in-the-blank billions of the dollars. It won’t at all. What the companies needed as much as money is time and that’s what the government has given them.

This is sorta of like sausage-making. I only care about the end result and I’d rather not know how it happens. My problem is that the takeover should (must!) lead to full privatization. This can’t be a trip to the repair shop because the problem will happen again. That’s not a prediction. It will happen again. -

I’m Back

Eddy Elfenbein, September 8th, 2008 at 10:51 amI’m back to blogging after a great week at the beach. Although I had to leave the Outer Banks a bit early to escape Hurricane Hanna.

So what did I miss? Sarah Palin turned the McCain campaign around. The feds took over Fannie and Freddie and the Panthers stunned the Chargers on the last play of the game!

The Buy List did pretty well in my absence. We had good earnings from both Donaldson (DCI) and Jos. A Banks (JOSB). I’ll have more once I catch up on all my email. -

I am Outta Here

Eddy Elfenbein, August 30th, 2008 at 11:18 amI’m off to the Outer Banks for the week. I’ll be returning next Monday–tan, rested and ready.

In the meantime, please check out the many fine bloggers on my blogroll. Before I go, I’ll leave you with this:

Have a happy and safe Labor Day! -

Ouch!

Eddy Elfenbein, August 29th, 2008 at 3:57 pmFrom the FT:

Merrill Lynch’s losses in the past 18 months amount to about a quarter of the profits it has made in its 36 years as a listed company, according to Financial Times research that highlights the extent of the global banking crisis.

Since the onset of the credit crunch last year, Merrill has suffered after-tax losses of more than $14bn as its balance sheet has been savaged by almost $52bn in writedowns and credit-related losses.

Merrill’s total inflation-adjusted profits between its 1971 listing and 2006 were about $56bn, according to figures from Thomson Reuters Fundamentals and an FT analysis of reported earnings.

The $14bn in losses for 2007 and the first two quarters of 2008 equal half of Merrill’s profits since the beginning of the decade. -

A Sell Signal

Eddy Elfenbein, August 29th, 2008 at 1:10 pmFrom Marketwatch:

Afterward, he walked the next five traders.

-

Did the Political Markets Fail?

Eddy Elfenbein, August 29th, 2008 at 11:50 amBarry and Felix weigh in on Intrade’s call on the Palin selection. As I’ve said many times, the futures markets are not predictions markets. They’re really odds setting markets.

The markets didn’t “fail” simply because a low-priced contract paid off. Did the markets fail when Google was at $100 a share? Not at all, the long-shot paid off.

Futures markets aren’t particularly useful in this instance because the Veep pick is entirely the selection of one person. They’re more useful with events that are transparent, like an election or the Super Bowl. The markets can’t read Senator McCain’s mind, particularly when he’s trying to give off false signals (hence the dance with Lieberman) and go for an unconventional pick.

The political markets work because they can process lots of information very quickly. With a Veep selection, however, there’s no information. So with these types of events, you have to expect hyper-volatility as the decision time approaches. -

What If There Was a Recession and Nobody Came?

Eddy Elfenbein, August 29th, 2008 at 11:42 amFrom today’s IBD:

We keep looking for the much-anticipated recession, but it doesn’t seem to have gotten here yet. Could it be that many of those expecting a downturn were wrong, and the economy’s not going into the tank?

Going out on a limb to predict what the economy will do is a tricky business. It’s possible, though by no means likely, that the economy briefly lapsed into recession late last year or early this year, based on weak GDP data, falling home sales, rising oil prices and a jump in unemployment. We won’t know for sure until months — maybe years — after it ends.

Even so, we were struck by Thursday’s news that second-quarter GDP was revised up from 1.9% to 3.3%, more in line with boom than bust. The consensus estimate was for 2.7% growth.

As more than one economist has noted, nearly all of that growth — some 3.1% of it — came from stronger exports, a result of the weak dollar. The rest came from inventories. Take those away, and the economy crawled at a weak 0.2% pace for the quarter.

Fair enough. But we did our own calculations. The slowdown in the economy is mainly due to one thing: housing. We indexed overall GDP to housing GDP back to 2000.

As the chart shows, it’s a very stark picture. We crunched even more numbers. Since 2006, the economy minus the ailing housing sector has grown at an average 3.3% rate. Add housing back in, and GDP growth has averaged just 2.4%. So housing’s collapse has cost us roughly 1% of GDP.

Housing is still weak, with sales off 35% year over year and values depreciating at double-digit rates. Banks can’t boost lending much, since they’re writing off old loans and have to shrink capital. This will take time.

But listening to the media and the Democrats in Denver, you’d think the economy was in a depression. Well, it’s not. In fact, we’re modestly optimistic. By the end of this year, all the really bad year-to-year comparisons in growth will be over. Sales and prices will start to look more normal. And the panic will leave the market.

As noted, exports have supported the economy this year. To critics, a stronger dollar means export growth will slow. Maybe so. But falling oil prices mean our import tab will also drop.

Moreover, oil demand now is falling. The Energy Department recently reported a shocking statistic that got little attention: U.S. demand in June plummeted 1.17 million barrels a day from last year, and a spokesman said prices could fall below $100 a barrel due to rising output in the U.S., Brazil and Canada.

Other data also suggest grounds for optimism. Just this week, the Census Department reported median household income hit $50,233 in 2007, after inflation, a gain of 1.6% since 2001.

Despite the slowdown in growth, the number of people without health insurance fell one million last year, while the poverty rate was unchanged at 12.5% of the population. And believe it or not, the average unemployment and poverty rates under President Bush have been slightly lower than under President Clinton.

Sure, bad things can happen. But we don’t have to will them into existence. As it stands, the much anticipated recession — thanks to Bush’s tax cuts and timely Fed actions — might just be a no-show. -

My Boldest Prediction Yet

Eddy Elfenbein, August 28th, 2008 at 10:22 amWrite down this time and day, and note that I’m calling a bottom in Pakistan’s stock market.

In other news, Pakistan has barred stocks from trading below yesterday’s close.

One more prediction, this won’t end well.

(Via: Birthday Boy Joseph Weisenthal).

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His