Author Archive

-

Bove: Bear Will End Up Costing JPM $65 a Share

Eddy Elfenbein, March 25th, 2008 at 10:04 amRichard Bove said that when you add it all up, Bear will eventually cost JPMorgan Chase $65 a share.

While some may think that JPMorgan is getting Bear Stearns at a bargain price, “I do not,” Bove said in a note to clients. “Bear Stearns is a deeply troubled company which would have no value if the Federal Reserve had not stepped in to bail it out.”

JPMorgan does not need Bear Stearns mortgage operation, has a “much stronger investment banking business,” and the Bear Stearns New York headquarters is “just another piece of Manhattan real estate that it must rid itself of,” Bove said.

While JPMorgan Chase may want Bear Stearns’ prime brokerage business, it is likely that the unit’s best customers have already left for Goldman Sachs, he said.

Bove currently has a “Market Perform” rating and $44 price target on JPMorgan Chase. The target implies he expects shares to drop about 6 percent over Monday’s $46.55 close.

“What is most disturbing about this deal is that it uses a great deal of Morgan capital to buy a company that is losing market share, in a series of businesses that are declining in size, with a top management team that is best described as sclerotic,” he said. -

Pot Takes Out Ad on Kettle

Eddy Elfenbein, March 24th, 2008 at 8:14 amFox Business Network has taken out a big ad in the NYT and WSJ to question Cramer’s credibility over his Bear Stearns call. Here’s the PDF.

(Via: The Stalwart) -

Boozing British Bankers

Eddy Elfenbein, March 21st, 2008 at 10:16 amThe Independent is on the scene:

Rumour-mongering and rogue traders; buy-outs and bonus cuts: it’s been quite a week for bankers. And, yesterday, as drizzle fell and storm clouds gathered over the capital, the pub was the only place the nervous denizens of Canary Wharf wanted to be.

They emerged from their offices, loosening their ties, to toast a long Easter weekend which, regardless of the turmoil which preceded it, will at least bring respite to anxiety. “We are meant to be at work but we’ve come here for some solace,” a group of Lehman analysts said.

Lunchtime had just begun but they, along with many other suited drinkers, were on their fourth round of beers at the packed All Bar One branch under Reuters’ FTSE-100 ticker.Well done, lads. Well done.

-

JPMorgan offers Bear Stearns staff bonuses

Eddy Elfenbein, March 21st, 2008 at 7:59 amJPMorgan Chase & Co is offering bankers at Bear Stearns Cos bonuses to stay and support the controversial takeover, a person familiar with the situation said on Thursday.

JPMorgan Chief Executive Jamie Dimon met with hundreds of Bear Stearns executives late Wednesday, his first meeting with bank employees since the takeover was agreed to on Sunday.

At the meeting, Dimon, aiming to head off an exodus of Bear Stearns staff, proposed incentives to bank employees who stay and support the deal. He also expressed confidence that the deal would be completed as proposed, said the source, who was briefed on the meeting and is familiar with JPMorgan’s thinking.

Employees who are offered jobs by JPMorgan would receive a bonus that includes JPMorgan shares. Employees who are not offered jobs will receive at least a cash bonus of about 30 percent of their 2007 compensation if they stay through the completion of the deal, the source said.

It is unclear whether Bear Stearns employees, who own about 30 percent of the firm, were swayed by the offer.Well, allow me to clear it up—yes, they were swayed. The only question now is how much.

The most important number to consider in this deal is that JPM’s stock is up 25.8% this week. That’s an increase of $32 freakin billion, which is far more than Bear was ever worth. The BSC folks don’t want to hold on to their stock, they want JPM’s. -

Why Is the Stock Market Closed for Good Friday?

Eddy Elfenbein, March 21st, 2008 at 7:39 amToday is Good Friday and the stock market is closed. I have no idea why this is since most of the rest of the country is open for business. I live in Washington, DC and the Feds will shut down for practically anything. But not today—it’s only Wall Street.

When I got my first job as a broker, I remember my branch manager saying that it was some sort of ancient inter-confessional deal to have one Friday off for the Easter/Passover season. That could be right but I’ve never found anything to back it up. Today, however, a closed market on Good Friday is more likely so traders can follow their brackets without interruption.

(By the way, there’s some doctoral dissertation waiting to written on the effect of fantasy sports on finance. Every trader I’ve ever known has had several fantasy football or baseball teams going. Wall Street is quite good at alternate reality; real reality is still a bit iffy.)

The stock exchange closed for two hours in honor of the death of J.P. Morgan (the man, not the stock—that’s doing fine, thank you very much).

The stock exchange used to have a brief Saturday session that was discontinued in 1952. Interestingly, the Saturday sessions have nearly been erased from history. If you look at many data files, like the Dow or S&P historical data at Yahoo Finance, the Saturday sessions aren’t there.

Poor Saturday, it’s gone down the memory hold. -

Pop!

Eddy Elfenbein, March 20th, 2008 at 3:17 pmGold has not had a good week. The April contract closed at $1004.30 on Tuesday. It dropped $59 yesterday and it’s down another $25.30 today.

From Karl Marx in 1867:A commodity appears at first sight an extremely obvious, trivial thing. But its analysis brings out that it is a very strange thing, abounding in metaphysical subtleties and theological niceties.

-

Santelli TV

Eddy Elfenbein, March 20th, 2008 at 2:49 pmI love this guy. Santelli needs his own reality show. This needs to happen.

-

The Long Shot

Eddy Elfenbein, March 20th, 2008 at 7:47 amMatthew Yglesias comments on the absurdity of John Meriwether blowing up, yet again. He includes this parable:

Imagine I find a kind of gambling machine somewhere that works kinda sorta like an enormous roulette wheel. It has 100,000 possible outcomes, and on 99,999 of those outcomes it pays off at a 1:1 ratio. But on the 100,000th outcome, you lose at a 1:300,000 ratio. Obviously, placing a bet on that machine would be foolish.

Not to me.

I’d lay down $1,000, let it roll for 20 spins and walk away a billionaire.

Addendum: Or there’s a very remote chance that I’d go in the roulette business. I’d be cool with either outcome. -

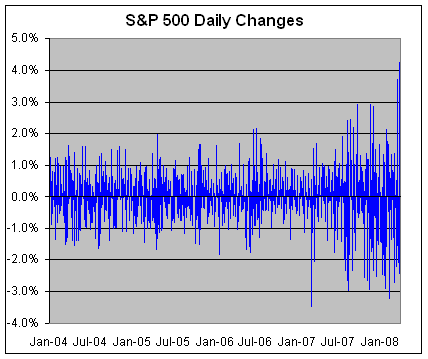

The Return of Volatility

Eddy Elfenbein, March 20th, 2008 at 7:42 am

According to a recent report by S&P, market volatility is at a 70-year high. I think that’s merely going by 1% daily changes. Other measurements indicate that volatility has indeed risen, but it’s more accurate to say that volatility has returned to normal from an unusually calm period.

The VIX still hasn’t reached the heights of 1998 to 2002. The index has closed above 30 for a few times recently, but it did it fairly regularly a few years ago.

I think the effect of volatility on equity returns is not very strong. The current VIX seems to have an effect on the dispersion of returns, but not the direction. -

How NCAA Tournament Seeds Have Fared

Eddy Elfenbein, March 19th, 2008 at 7:45 pmThe Chicago Tribune looks at how the NCAA tournament seeds have fared since 1985. I love the idea of a big tournament that invites a huge number of teams. It seems the most democratic, but there are some gaps in justice. For example, the #8 or #9 seed is really screwed because they always must play a #1 in the second round. Only 12 #8 or #9 teams have made it past the second round.

On the other hand, #12 is a pretty good seed. Those teams have a losing, but respectable record against the #5 seeds. A total of 14 number #12 seeds have made it past the second round.

My guess is that the seeds increase linearly while quality increases geometrically. The difference between a #12 and a #5 is probably about the same as a #1 and a #3.

If we wanted to be hard-headed, we could really make it a 12-team tournament and the results would be almost the exact same. Twenty of the 23 winners have been #1, #2 or #3 teams. Of course, that would ruin a lot of the fun.

I’ve noticed that no matter what happens, the media talks about how the first weekend was a “Cinderella Weekend.” But going by history, there’s nothing that surprising by having at least one #14 beat a #3, or having a #2 or #3 lose in the second round.

It’s fun to root for the Cinderella teams (we have a couple of local teams ranked in the double-digits), but history says that the odds are against them.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His