Author Archive

-

Earnings Preview: Bed Bath & Beyond

Eddy Elfenbein, September 24th, 2007 at 4:30 pmFrom the AP:

Home accessories retailer Bed Bath & Beyond Inc. reports earnings for the fiscal second quarter on Wednesday. The following is a summary of key developments and analyst opinion related to the period.

OVERVIEW: Home furnishings and accessories retailers are being pressured as the housing market sags, and consumers curb discretionary spending due to widening credit problems and high energy costs.

Bed Bath & Beyond Inc. is no exception. In June, the Union, N.J., company said its full-year profit would miss analyst expectations due to uncertain economic trends.

BY THE NUMBERS: Analysts polled by Thomson Financial expect a profit for the fiscal second quarter of 52 cents per share on revenue of $1.77 billion.

ANALYST TAKE: Bear Stearns analyst Christopher Horvers said in a note to investors on Monday that he remains cautious on the sector.

“Home furnishings remains one of the most challenging spaces in retail given the difficulties in housing, the fragmentation of the market, the discretionary nature of the products and the inventory build that has occurred across the retail landscape,” he wrote.

He said he believes Bed Bath & Beyond will continue to “encounter near-term headwinds” and said he expects a few more quarters of difficult trends.

For the quarter, he expects its gross margin to fall less than 1 percent to 41.4 percent of sales, driven by an increase in inventory acquisitions costs, a shift in merchandise mix and a heightened promotional environment.

WHATS AHEAD: In a note to investors on Monday, Deutsche Bank North America analyst Mike Baker said he is “concerned” about analyst estimates for fiscal 2008 in the home furnishings sector overall, including Bed Bath & Beyond. Analysts polled by Thomson Financial expect, on average, a profit of $2.47 per share.

“The company will not give its 2008 guidance until December, but at that time, we would not be surprised if BBBY guides to a number below the current consensus,” Baker wrote.

A profit of $2.47 per share in fiscal 2008 implies a same-store sales improvement of 3 percent and a slight increase in operating margins, Baker said.

“But, with our concerns regarding high inventories industry wide, demand environment would need to improve considerably over the next year to drive that kind of recovery,” Baker wrote. “The recent Fed easing could help us get there, but that’s not without risk, in our view.”

The Federal Reserve approved a half-point reduction in interest rates on Thursday, in an effort to ease concern about the economy.

STOCK PERFORMANCE: Shares fell nearly 15 percent during the quarter. -

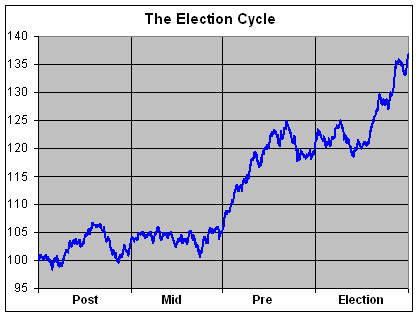

The Presidential Election Cycle

Eddy Elfenbein, September 24th, 2007 at 2:35 pmOut of boredom, this weekend I looked at all the Dow daily closings for the last 111 years (about 28,000 points of data) for a closer examination of the Presidential Election Cycle’s impact on stock prices. (What the hell was I thinking?) I did this before, but that only for the data from 1930 to mid-2006. This time, I looked at the every day from 1896 to last Friday.

I don’t put much faith in these types of trading rules, but there are some interesting results. Historically, the Dow has gained an average of 24.1% from September 30 of the mid-term election year to September 6 of the pre-election year, which we recently passed.

This means that nearly two-thirds of the Dow’s four-year gain (24.1% of 36.7%) comes in less than one-quarter of the time. That’s a pretty stunning stat.

After September 6 of the pre-election year, the Dow has historically pulled back 5.2% to May 29 of the election year. After that, it puts on a nice 23.2% climb to August 3 of the post election year. Then trouble starts. After August 3, the Dow then pulls back 5.6% and we’re back at our starting point, September 30 of the mid-term election year.

Also, Leap Day is a positive day for the Dow, up an average of 0.1256%. -

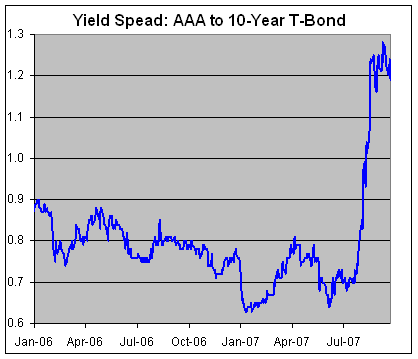

Looking at Long-Term Credit Spreads

Eddy Elfenbein, September 24th, 2007 at 10:06 am

If you’re confused by the credit crunch that happened last summer, here’s a good graph showing you some of the details. This chart shows the spread between Moody’s AAA Corporate yield index and the 10-year Treasury yield.

Since lending to the government is pretty low risk, they own the printing press after all, the lower the spread signifies greater confidence the free market has in corporations paying back their loans. When the difference widens, that signifies that investors have become much more afraid of loaning to corporations. In other words, they’ve become more afraid of taking risks.

In mid-July, the spread was around 70 basis points, which was close to some of the lowest levels in the past 15 years. Then, very suddenly, the spread exploded to over 120 basis points in less than one month.

While the spread is still wide compared with last summer, it’s still moderate compared with the long-term. Consider that after 9/11, it ballooned to over 260 basis points. Looking at last ten years, the current spread is within the lowest 37th percentile. -

Playmate of the Year Talks Investing

Eddy Elfenbein, September 24th, 2007 at 8:45 am -

A Lesson on Data Mining

Eddy Elfenbein, September 24th, 2007 at 8:42 amHere’s a cute stat I saw over at Motley Fool. Cal Tech professor David Leinweber crunched the numbers and found that the singe-best predictor of stock prices is butter production in Bangladesh. “When butter production was up 1%, the S&P 500 was up 2% the next year. Conversely, if butter production was down 10%, you could predict the S&P 500 would be down 20%.”

Coincidence? Well, yes. But this isn’t too far from the kind of research that’s been driving many hedge funds. -

Beware the Emerging Hegemonic Canadian Superpower

Eddy Elfenbein, September 21st, 2007 at 3:14 pmFor the first time in three decades, the loonie reaches parity.

-

Civics Quiz

Eddy Elfenbein, September 21st, 2007 at 2:29 pmI pride myself on being a civics geek. I got 58 out of 60 on this quiz. (I missed #36 and #58.)

How did you do? -

The Fed’s Irresponsible Move

Eddy Elfenbein, September 21st, 2007 at 2:20 pmHere’s a dissenting view from Vitaliy N. Katsenelson:

I’ve seen this movie before, and it doesn’t end pretty. That’s what I thought on Sept. 18 when Federal Reserve Chairman Ben Bernanke took the road so often traveled by his predecessor, Alan Greenspan, and threw the financial markets a sop in the form of a big cut in interest rates. It was clearly what the markets wanted, as the immediate 336-point jump in the stock market confirmed. But popular decisions are not always the right decisions. (Just consider Greenspan’s popular 2001 interest rate cuts, which actually caused the current housing bubble.)

Indeed, at the core of today’s credit mess—whether in housing or the now battered markets for commercial paper—lies a glut of global liquidity. That has dramatically altered our perception of risk and fueled an unwillingness to accept traditional credit limits. If a homeowner couldn’t qualify for a conventional mortgage, brokers were more than happy to offer an exotic loan the borrower could never realistically pay off. If a loan was too risky to be sold as investment-grade, investment banks could always concoct elaborate bundles of good and toxic credits that (supposedly) eliminated the risk.

Nowhere was this disregard of financial reality more apparent—or damaging—than in housing. The housing bubble was fueled by many years of low interest rates, which eventually priced many people out of their dream homes. But instead of settling for less or renting, people pursued their American dream (the house with a white picket fence, 2.7 kids, and 1.2 dogs) with a vengeance, taking out adjustable-rate, interest-only—or even worse, negative-amortization loans. -

Wall Street Turns 20

Eddy Elfenbein, September 21st, 2007 at 12:54 pm

The iconic movie turns 20.Since its release in December, 1987, “Wall Street” has been required viewing for anyone working in finance and a standard way of framing the go-go ’80s of junk bonds and power ties – an era that some say has returned during the recent private equity-led mergers and acquisitions boom.

With a twentieth-anniversary DVD released on September 18 and a sequel currently in development, “Wall Street” is again a topic of conversation.

The film is best-known for its lasting character, Gordon Gekko, played by Michael Douglas, who netted an Academy Award for Best Actor for the role. And its most famous line -“Greed, for lack of a better word, is good,” typically shortened to just “Greed is good” – is a favorite of headline writers and Wall Streeters alike.Here’s an interesting tidbit about the famous “greed is good” line. The original source comes from a speech by Ivan Boesky, but it was hardly in the form of macho Nietzschean posturing. What Boesky said was “Greed is all right; by the way, I think greed is healthy. You can be greedy and still feel good about yourself.”

Feel good about yourself? It’s interesting that he framed it terms of self-image, as if that’s the most important standard. He’s being more Oprah than Michael Milken. The iconic statement from the 1980s is more closely related to the self-absorption of the 1990s. -

Questions for Greenspan

Eddy Elfenbein, September 21st, 2007 at 10:28 amCaroline Baum has some questions for Alan Greenspan. Here are a few:

4. In that same vein, you write you were “struck by how relatively easy it was to bring inflation down.” When you assumed the Fed chairmanship in August 1987, the consumer price index was rising at an annual rate of 4.3 percent. In January 2006, the month you left, the CPI was rising 4 percent.

You inherited a core CPI, which excludes food and energy, of 4.2 percent and cut it in half. That computes to a decline of 0.1 percentage point a year. If lowering inflation was such a chip shot, why don’t you have more to show for your effort?

5. When you were Fed chairman, you wondered out loud about “irrational exuberance” in the stock market, even though Bob Rubin, whom you call one of your “foxhole buddies” (the other was Larry Summers), said such comments were inappropriate for a government official.

When Leslie Stahl asked you about your personal investments, you refused to comment on the stock market. Aren’t you confusing your role as a public servant and private citizen?

6. You say it’s improper for a president to comment on monetary policy, yet you actively tried to influence fiscal policy. You told Leslie Stahl you were an “economic consultant” to Bill Clinton, that you are “very knowledgeable about lots of different subjects.” And no one else is?

You told Al Hunt you “give advice because they ask me.” Your successor, Ben Bernanke, has made a point of not offering pronouncements on fiscal policy. What part of “no comment” don’t you understand?

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His