Author Archive

-

Morning News: March 23, 2022

Eddy Elfenbein, March 23rd, 2022 at 7:06 amGlobal Bond Plunge Wipes Out $2.6 Trillion, Exceeding Losses of 2008 Financial Crisis

Wall Street Is Scrambling for the Exits in Moscow — and Billions Are at Stake

Hedge Fund Up 3,000% in Five Years Can’t Buy Enough China Stocks

The U.S. Scales Back Metal Tariffs as Britain Lifts Duties on American Whiskey and Jeans

Will War Make Europe’s Switch to Clean Energy Even Harder?

Dutch Bank ING Ends Financing for New Oil and Gas Projects

TotalEnergies Says It Will Stop Buying Oil from Russia by the End of the Year

Surveillance Risks Shape How Central Banks Test Digital Currencies

The ‘Great Retirement’ Disconnect That Puzzles U.S. Economists

The Education Department Says Owners Will Have to Pay If Their Colleges Collapse

Student-Loan Freeze Saves Borrowers Nearly $200 Billion

Home Appreciation Is a Sign You May Live In a Feudal Society

Amazon Union Vote Set to Begin in New York, Which Has Challenged Company in Past

Disney Workers Walk Out to Protest Company’s Response to Florida Bill

U.S. SEC to Elon Musk: Regarding Your Tweets, a Deal is a Deal

The Morphe Beauty Saga Isn’t Pretty

Be sure to follow me on Twitter.

-

CWS Market Review – March 22, 2022

Eddy Elfenbein, March 22nd, 2022 at 7:35 pm(You can sign up for our premium newsletter for $20 per month or $200 per year. Sign up here.)

The stock market continued an unusual streak today. For 23 straight days, the S&P 500 has not had a daily gain of less than 1%. To be sure, the market had several positive days over that span—nine to be exact—but all nine produced gains of more than 1%, and four were more than 2%.

The reason isn’t hard to find. Such is the stock market at war. Most of the days have been volatile and negative. Fortunately, the stock market has had an impressive bounce over the past few days. The good news is that the S&P 500 closed above its 50- and 200-day moving averages.

Still, I’m suspicious of this latest move.

For one, the recent uptick has been inordinately strong. In just six days, the S&P 500 has added more than 8%. Last week, the S&P 500 rose by over 1% for four days in a row. In all its history, the index has never risen by more than 1% for five straight days. Alas, last week was no exception.

Also, the rally has been almost exclusively confined to high beta stocks. That’s not a good sign. Check out this chart. Since March 7, the S&P 500 High Beta Index is up over 11.5% while the S&P 500 Low Volatility Index is up just 0.85%.

The Federal Reserve Needs to Wake Up

Last week, the Federal Reserve decided to raise interest rates for the first time in more than three years. I’ve been critical of the Fed as I believe the central bank is behind the curve on combatting inflation. The Fed’s recent economic forecasts bear out my fears as the Fed apparently believes that inflation will soon fall back to modest levels. Eh…I’m not so sure.

Yesterday, Federal Reserve Chairman Jerome Powell spoke before an economic policy conference and tried to alleviate fears that the Fed isn’t being aggressive enough. Specifically, Powell said that the Fed is open to raising rates by 0.5% increments if needed. (It’s needed.)

Prior to last week’s meeting, there had been some speculation that the Fed would raise rates by 0.5%. Eventually, the Fed made it clear to the market that it would only raise by 0.25%. The market seemed pleased.

Since Powell’s comments, the futures market has noticeably shifted its tone. While we never know exactly what the Fed is thinking, we can do the next best thing: look at how traders are betting.

According to the latest prices, traders think the Fed will hike by 0.5% in May and again in June. Goldman Sachs just said it expects that as well. Ultimately, traders expect the Fed to raise rates by 2% by the end of the year. That may not be enough.

Next, I’m going to bring up some economic theory. No, I promise it won’t be boring. Well, it will be boring but let’s say it’s relevant. Anyway, I’ll make it simple.

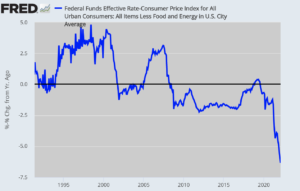

There’s the idea that there’s a magic, invisible, natural interest rate. If the Fed goes below the natural rate, that causes inflation. If they go above it, that chokes off the economy. The hard part is that we don’t know exactly what the natural interest rate is. It’s like the invisible man in the room. While we can’t see it, we can feel its effects.

Here’s a look at the inflation-adjusted Fed funds rate, based off core inflation. The important point is that you can see how dramatically low interest rates are right now.

Current thinking on the Fed is that the natural rate is 0.5% above inflation. According to the Fed’s preferred stats, inflation is currently running at 6.1%. So that means that interest rates will have to go up to 6.6%? That’s a huge increase, and that’s just to be neutral!

It gets a little more complicated because the Fed sees inflation falling quickly. By the end of this year, the Fed sees inflation cooling off to 4.1%. As a pleasant side effect, the Fed projects that its current policies will work just fine. Again, I’m skeptical.

By 2024, the Fed forecasts inflation of 2.3% and interest rates of 2.8%. In other words, they think we’ll hit the natural rate in a mere 21 months. I hope that’s true, but that strikes me as a very optimistic forecast. Too optimistic.

The Yield Curve Starts to Flatten

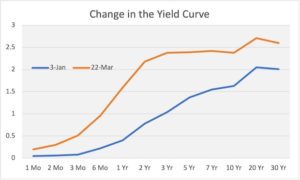

The bond market has already reacted to the Fed’s aggressive tone. Today, the 20-year Treasury closed at 2.71%. That’s up 52 basis points since earlier this month. You may have noticed that 30-year mortgage rates are closing in on 5%. The bond market is having one of its worst downturns in several years.

The mid-maturity Treasury yields have risen the most. Since January 4, the date of the stock market’s high, the yield on the five-year Treasury has increased by 102 basis points. The yield on the three-year has increased by 136 basis points.

Here’s what the yield curve looks like today compared with the end of the year:

Notice the big bump the orange line now has. That’s due to the Fed. Beyond five years out, the yield curve is very nearly flat, and a negative yield curve is one of the warning signs of a recession.

Not surprisingly, several economic forecasts have been pulled back in recent days. The Atlanta Fed’s GDP Now model now projects Q1 GDP growth of just 1.3%. That’s actually higher than where it had been. A few weeks ago, the forecast was for negative growth. Bank of America sees Q1 GDP growth of 1.6%. Goldman Sachs is at 0.5%.

We’re nearing the end of Q1 and that means that earnings season will start up in mid-April. Wall Street expects the S&P 500 to report Q1 earnings of $51.28 per share. That’s the index-adjusted figure. If that forecast is accurate, it would represent an increase of 8.2% over last year’s Q1. I’m afraid that’s too high.

For all of 2022, Wall Street sees earnings of $225.03 per share. That’s an increase of $25 in the past year. That means the S&P 500 is going for about 20 times this year’s earnings. That’s a little high but nothing extreme.

By the way, tomorrow is the second anniversary of the Covid low. The S&P 500 plunged 33.9% in 23 trading days. The index reached its closing low of 2,237.40 on March 23, 2020. That was a scary time but we’ve more than doubled since then. Even measuring from the February 2020 high, the S&P 500 is still up more than 32%. To quote Peter Lynch, “The real key to making money in stocks is not to get scared out of them.”

Heico Breaks Out to a New High

Last week, I highlighted one of our Buy List stocks, Silgan Holdings (SLGN). I’m pleased to report that the stock broke out to a new high today.

That’s not the only Buy List stock hitting a new high. Heico (HEI) did, too. This is a wonderful company that still isn’t very well known. Heico is the kind of niche business I love. With investing, the only thing better than a monopoly is a near-monopoly. (The full-on monopolies tend to get too much government attention.)

Heico makes replacement parts for the airline industry. If a commercial aircraft needs some obscure new part, the airline can’t run down to the local hardware store. Instead, it needs to special-order it. Moreover, there’s a great deal of cost pressure on the airlines to keep the older planes serviceable.

Also, the aircraft parts often need to meet strict regulatory guidelines. The part maker really has to know what it’s doing. That’s where Heico comes in. The business is lean and well-run.

I can’t tell the Heico story without mentioning the Mendelson family. Larry Mendelson is the current chairman and CEO. In the 1950s, he took a finance class taught by David Dodd. Fans of value investing will recognize Dodd’s name. He was the co-author of Security Analysis with Ben Graham. Security Analysis is probably the foundational text of value investing.

Mendelson took those lessons to heart. He made a good deal of money in real estate and wanted to diversify his holdings. That led him to invest in an under-performing industrial company. He really didn’t care what he bought, as long as it was cheap and had potential to be retooled for future growth. He chose well.

Heico was originally founded in 1957 by Dr. William Heinicke as Heinicke Electronics. By the 1980s, Mendelson controlled a sizeable share in the company and was able to make himself CEO. The Heinicke family still owns a large chunk of the voting shares, and several family members hold key positions within the company.

When airplane owners need a new part and go back to the original equipment manufacturer (OEM) to get replacements, they’re often charged a steep price. The profit margins can exceed 30%. That provides enormous opportunity for Heico. Consider that many aircraft are over 20 years old.

The aviation industry is broadly diversified, and Heico is also able to get sales from commercial and military customers. That means that if there’s a drop-off on one end of the business, the other side can pick up the slack. Wherever there’s a demand to cut costs, Heico has the potential to do well.

In some respects, I see Heico’s role as similar to that of a generic drugmaker. Heico provides a low-cost copy of the original product, which is regulated by the Federal Aviation Administration. By the way, Heico does more than aircraft parts. They also supply parts for satellites, rockets, missiles and even medical instruments.

Since 1995, shares of Heico are up a cool 51,000%:

Despite rising nearly 10-fold, the S&P 500 looks like a flat line next to Heico.

Heico is in an enviable position and nearly dominates its market. The company sells to 19 of the top 20 airlines in the world, and their customers love them. Like nearly everyone else, though, Heico has felt the squeeze of the economy, and COVID was especially rough on the airline industry.

Still, Larry Mendelson managed Heico well during a rough patch. One month ago, Heico reported fiscal Q1 earnings of 63 cents per share. That’s up from 51 cents per share one year before. Wall Street had been expecting 61 cents per share. Net sales rose by 17% to $490 million, and operating income increased by 23%.

Heico noted that while Covid has been impacting its business, that impact has been gradually declining over time. Heico has now seen “six consecutive quarters of sequential growth in net sales and operating income at the Flight Support Group.”

Heico’s consolidated operating margin improved to 20.2% in the first quarter of fiscal 2022, up from 19.2% in the first quarter of fiscal 2021. EBITDA increased 18% to $122.3 million in the first quarter of fiscal 2022, up from $104.0 million in the first quarter of fiscal 2021.

Heico’s business is divided into two groups: the Flight Support Group and the Electronic Technologies Group. For Q1, the Flight Support Group had sales of $272.7 million, while the Electronic Technologies Group had sales of $222.3 million.

For fiscal Q1, Flight Support saw its operating income soar by 103% and net sales rise by 37%. That was driven by a 48% increase in organic net sales for its commercial-aerospace parts and services. Flight Support’s operating margin improved to 19.2%. That’s up from 13.0% in the first quarter of fiscal 2021.

Electronic Technologies’s sales for Q1 dropped a small amount. That was due to “decreased demand for our defense and space products.” Electronic Technologies had a Q1 operating margin of 25.0%.

The stock hit a new high today of $155.45 per share. If you want to learn more about Heico and the other stocks on our Buy List, please sign up for our premium service.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

-

Morning News: March 22, 2022

Eddy Elfenbein, March 22nd, 2022 at 7:08 amCentral Banks Grapple With Dual Threat of Slowing Growth, Rising Inflation

Powell Says Fed Will Consider More-Aggressive Interest-Rate Increases to Reduce Inflation

Shale Companies Drilling More, but Oil Output Growing Little

Bitcoin Miners Want to Recast Themselves as Eco-Friendly

East Coast Ports Rushed to Attract Mega Ships. Now, One Is Stuck Outside D.C.

The S.E.C. Moves Closer to Enacting a Sweeping Climate Disclosure Rule

For Companies Still Selling in Russia, ‘Essential’ Is a Loose Term

LME in Talks with Governments on Whether to Block Russian Metal

Arcelormittal Removes Russian Materials from Steel Supply Chain

How One Oligarch Used Shell Companies and Wall Street Ties to Invest in the U.S.

Cattle Ranchers Take Aim at Meatpackers’ Dominance

Buffett Thumbs Nose at Goldman Bankers With Quirky Deal Price

Alibaba Upsizes Share Buyback by Two-Thirds to Record $25 Billion

‘Red Flags’ as Some China Property Developers Say They Can’t Release Earnings On Time

Boeing Faces New Upheaval After Crash of Chinese Airliner

Be sure to follow me on Twitter.

-

Powell Strikes a Hawkish Tone

Eddy Elfenbein, March 21st, 2022 at 2:32 pmFederal Reserve Chairman Jerome Powell spoke today before an economic policy conference. Powell sounded markedly more willing to use interest rates to combat inflation.

In particular, he said that the Fed could start using 0.5% rate increases. Before last week’s increase, which was the first in more than three years, there had been some speculation that the Fed would increase by 0.5%. Ultimately, the Fed raised rates by just 0.25%.

I think the Fed is making two errors. The first is that the inflation threat is more serious than they realize. Their latest economic projections are evidence of that. The other issue is the threat of an economic slowdown, though not necessarily a recession.

Finally, what will it take to restore price stability? The ultimate responsibility for price stability rests with the Federal Reserve. Price stability is essential if we are going to have another sustained period of strong labor market conditions. I believe that the policy approach that I have laid out is well suited to achieving this outcome. We will take the necessary steps to ensure a return to price stability. In particular, if we conclude that it is appropriate to move more aggressively by raising the federal funds rate by more than 25 basis points at a meeting or meetings, we will do so. And if we determine that we need to tighten beyond common measures of neutral and into a more restrictive stance, we will do that as well.

That’s good to hear that they are aware of the problem. However, too often Fed chairs rely on tough talk rather than concrete action. Powell also said that the Fed could soon start unwinding its ginormous balance.

-

Bonds Hit the Skids

Eddy Elfenbein, March 21st, 2022 at 9:43 amThe stock market has had a nice rally over the last four days. The S&P 500 managed to close above its 50-day moving average on Friday. Still, I’m skeptical that this burst will last.

For one, it’s been a dramatic spike upward. That’s usually not a good sign of lasting strength. Also, it’s heavily tied to high beta stocks. The low volatility names haven’t moved that much. I’d much rather see a rally that lifts many boats.

This morning, Berkshire Hathaway said it’s buying insurance company Alleghany for $11.6 billion. That works out to $848.02 per share in cash. By the way, Alleghany has one of the coveted single-letter ticker symbols, “Y.” I wonder if anyone will go for it.

The real action lately hasn’t been in the stock market but in the bond market. Bonds are having one of their worst stretches in years. Here’s a chart of the Treasury Bonds ETF (TLT):

-

Morning News: March 21, 2022

Eddy Elfenbein, March 21st, 2022 at 7:09 amPressed to Choose Sides on Ukraine, China Trade Favors the West

Agriculture Giants Stay in Russia Despite Calls to Exit Over Ukraine War

Wheat Prices Soar on Ukraine Fears, but U.S. Growers Can’t Cash In

Fleeing War in Ukraine, They’re Met With Employers Offering Paychecks

Silicon Valley’s Wealthiest Russian Is Carefully—Very Carefully—Distancing Himself From Putin

How to Fight Inflation in Wartime

With Inflation Surging, Biden Targets Ocean Shipping

Gas Prices Upend Small Business

Chevron Pulls Union Workers from California Refinery Ahead of Strike

One of Wall Street’s Most Vocal Bears Says Sell the Rally

U.S. Home Sales Tumble; Higher Prices, Mortgage Rates Eroding Affordability

The Latecomer’s Guide to Crypto

New York City’s Renewed Vibrancy Is Hiding Deep Economic Pain

Toronto, the Quietly Booming Tech Town

Warren Buffett to Buy Alleghany for $11.6 Billion in Return to Dealmaking

Thoma Bravo to Buy Anaplan for $10.7 Billion

Be sure to follow me on Twitter.

-

Morning News: March 18, 2022

Eddy Elfenbein, March 18th, 2022 at 6:18 amJapan Parts Makers Halt Output After Quake, Another Blow To Supply Chain

Russia’s War in Ukraine Is Choking the World’s Supply of Natural Resources

How the War in Ukraine Could Slow the Sales of Electric Cars

Retreat From Russia Riddled With Risks For Western Banks

Amid Invasion of Ukraine, I.R.S. Aims to Police Oligarch Sanctions

China’s Information Dark Age Could Be Russia’s Future

Gig Workers Say High Gas Prices May Be a Breaking Point

Stock Traders Brace for a $3.5 Trillion ‘Triple Witching’ Event

USAA is Fined $140 Million For Bad Money Laundering Controls

The King of Block Trades Is Entangled in a U.S. Probe of Morgan Stanley

Apple’s Latest iPhone Sidelines Carriers From Buying Process

Apple’s Hold on App Store Set to Face Significant Challenge From New European Law

Amazon Closes Deal to Acquire MGM

GameStop Shares Fall on Surprise Loss

The 9-to-5 Schedule Should Be the Next Pillar of Work to Fall

Be sure to follow me on Twitter.

-

Morning News: March 17, 2022

Eddy Elfenbein, March 17th, 2022 at 7:04 amChina Finds a Way to Do Covid Zero While Keeping Factories Open

New Covid Wave in China Hits Sellers of ‘Quarantine Insurance’

Tencent, Alibaba, Meituan Extend Stunning Surge as Traders Cheer Support Vows

This Tropical Island’s Economy Is Being Crushed by War in Ukraine

Broke Oligarch Says Sanctioned Billionaires Have No Sway Over Putin

Nickel Traders Awake to Fresh Mayhem as LME Glitches Again

Inflation vs. Recession: The Fed Is Walking a Tightrope

What the Fed’s Rate Increase Means for You

What You Might Misunderstand About Interest-Rate Hikes

The U.S. Yield Curve Has Been Flattening: Why You Should Care

Best Way To Tackle Inflation: Confirm Biden’s Fed Nominations

Shoppers Reach Their Limits on Some Price Increases

Carbon-Capture Startup Using Dirt Cheap Material Raises $53 Million

Former Starbucks CEO Howard Schultz to Return as Chain Faces Union Push, Rising Costs

Netflix Plans To Start Charging For Password Sharing, And Customers Aren’t Happy

Examining AMC’s ‘Embarrassingly Stupid’ Investment In A Literal Gold Mine

Be sure to follow me on Twitter.

-

The Fed Hikes

Eddy Elfenbein, March 16th, 2022 at 2:06 pmIt’s official. The Federal Reserve has raised interest rates. The new range for the Fed funds rate is 0.25% to 0.50%.

Looking at the Fed’s projections, the median Fed member sees seven rate hikes this year. That works out to a 0.25% increase at every meeting this year.

James Bullard was the lone dissenter.

Here’s the statement:

Indicators of economic activity and employment have continued to strengthen. Job gains have been strong in recent months, and the unemployment rate has declined substantially. Inflation remains elevated, reflecting supply and demand imbalances related to the pandemic, higher energy prices, and broader price pressures.

The invasion of Ukraine by Russia is causing tremendous human and economic hardship. The implications for the U.S. economy are highly uncertain, but in the near term the invasion and related events are likely to create additional upward pressure on inflation and weigh on economic activity.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. With appropriate firming in the stance of monetary policy, the Committee expects inflation to return to its 2 percent objective and the labor market to remain strong. In support of these goals, the Committee decided to raise the target range for the federal funds rate to 1/4 to 1/2 percent and anticipates that ongoing increases in the target range will be appropriate. In addition, the Committee expects to begin reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities at a coming meeting.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals. The Committee’s assessments will take into account a wide range of information, including readings on public health, labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michelle W. Bowman; Lael Brainard; Esther L. George; Patrick Harker; Loretta J. Mester; and Christopher J. Waller. Voting against this action was James Bullard, who preferred at this meeting to raise the target range for the federal funds rate by 0.5 percentage point to 1/2 to 3/4 percent. Patrick Harker voted as an alternate member at this meeting.

-

February Retail Sales Rose by 0.3%

Eddy Elfenbein, March 16th, 2022 at 12:17 pmThe stock market is up strongly again today. The Nasdaq is up more than 2%. Finance and Tech are leading the way while defensive areas like Utilities and Staples are mostly unchanged.

There’s talk of a ceasefire but I’m skeptical. Today is another good example of a bounce off the bottom, or near bottom, but I’m suspicious of how long it will last.

At 2 pm, the Fed will release its policy statement. The Fed is widely expected to increase interest rates by 0.25%. After the meeting, Chairman Powell will hold a press conference.

We also got the retail sales report this morning. For February, retail sales rose by 0.3%. That was 1% below expectations. If we exclude autos, then sales were up just 0.2%. Expectations were for a gain of 0.9%.

The spending numbers were well below the rise in prices, which increased 0.8% in February, according to Labor Department data released last week. Retail spending numbers are not adjusted for inflation.

The biggest dent in February’s numbers came in online shopping, with nonstore sales down 3.7%.

One bright spot in the data released Wednesday is that January spending was revised up to an increase of 4.9%, a blistering pace that was even stronger than the initial estimate of 3.8%.

The two-month numbers “suggest that real consumption growth remains reasonably solid” though some headwinds are beginning to show, particularly from expected interest rate increases coming from the Federal Reserve, said Andrew Hunter, senior U.S. economist at Capital Economics.

“With real disposable incomes having already been falling since mid-2021, as earlier fiscal support was withdrawn, and the more general surge in prices took its toll, real consumption growth still looks likely to slow over the coming months, particularly when the personal savings rate is already below its pre-pandemic level,” Hunter wrote. “It also may not be long before Fed tightening starts to hit spending on big-ticket durables.”

Consumers, however, remain flush with cash, finishing 2021 with $1.4 trillion in savings though the personal savings rate, most recently at 6.4%, has been coming down steadily during the Covid pandemic era.

Demand has been extraordinary for goods over services, and supply has struggled to keep up. That has fueled inflation running at a 7.9% rate on a 12-month basis, the fastest pace in more than 40 years.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His