Author Archive

-

CWS Market Review – September 28, 2018

Eddy Elfenbein, September 28th, 2018 at 7:08 am“Investing without research is like playing stud poker and never looking at the cards.” – Peter Lynch

The big news this week was that the Federal Reserve raised interest rates by 0.25%. The stock market responded with a big yawn. The S&P 500 is still very close to its all-time high.

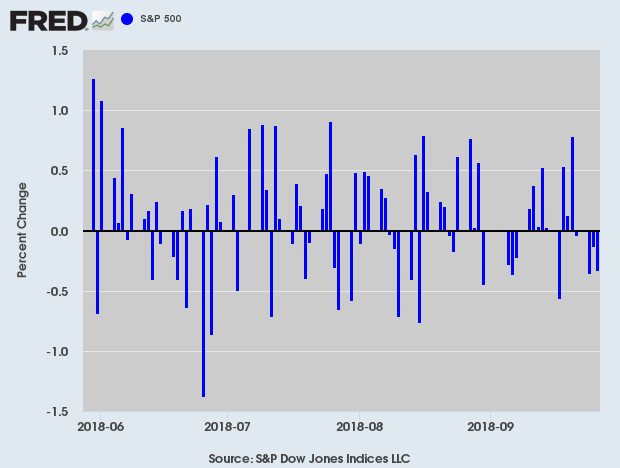

In fact, not much has bothered the S&P 500 lately. Not the Fed. Not approaching elections. Not even Elon Musk getting sued by the SEC. Ryan Detrick, one of my favorite numbers guys, recently noted that the past few months have been some of the least volatile on record. You probably wouldn’t have guessed that by looking at the headlines, but the S&P 500 has now gone 66-straight days without a daily move of more than 1% either up or down.

Will the calm market last? I think so. In this week’s CWS Market Review, we’ll take a closer look at this week’s Fed news and what it means for us. We’ll also take a look at the recent earnings report from FactSet. We’ll also preview next week’s earnings report from RPM International. First, though, let’s look at what the Fed’s game plan is.

The Federal Reserve Raised Rates—What Does It Mean for Us?

On Wednesday, the Federal Reserve raised interest rates. The move was almost universally expected. This was the Fed’s third increase this year and the eighth of the current cycle. The Fed’s target range for overnight interest rates is now 2% to 2.25%. This means that interest rates are basically in line with inflation. We haven’t had positive real rates in a decade.

The reason for the Fed hike is actually good news. It means that the economy has been improving. One bit of news was that in the Fed’s policy statement, the FOMC dropped the word “accommodative” in describing its policy stance. There are folks who pore over every letter of every Fed statement, looking for clues. Fed Chairman Jay Powell cut off any speculation. He said the new language doesn’t reflect any change in the path policy. Powell reiterated that the Fed still sees itself following the same path as before: gradual rate hikes.

Here’s the key part of the policy statement:

Information received since the Federal Open Market Committee met in August indicates that the labor market has continued to strengthen and that economic activity has been rising at a strong rate. Job gains have been strong, on average, in recent months, and the unemployment rate has stayed low. Household spending and business fixed investment have grown strongly. On a 12-month basis, both overall inflation and inflation for items other than food and energy remain near 2 percent. Indicators of longer-term inflation expectations are little changed, on balance.

I know it sounds dry, but that’s about as optimistic as central bankers get. Frankly, I wouldn’t read too much into the Fed’s latest move. In terms of the stock market, higher short-term rates erase some of the allure of high-dividend stocks. That’s only natural. But it’s a mistake to think that a rising rate environment is bad for all value stocks.

I suspect that the Fed’s policy will cause investors to not be as open to risk as they’ve been. When rates are low, it’s not a big deal to get in on a hi-flying stock. Other financial assets aren’t offering much competition. That’s not so true anymore. (In fact, I suspect that the lack of competition helped drive alternative assets like Bitcoin. That was the only game in town.)

Members of the Fed also updated their economic projections. This is where things get interesting, because we can assume that the cycle of rate increases is probably closer to its end than its beginning. The Fed sees one more rate hike coming this year. After that, they forecast three hikes next year, one more in 2020 and none in 2021.

In my opinion, 2021 is way too far out to make a reasonable prediction. But in the near term, the Fed’s forecasts tell us that the economy is very likely on a sound footing. Earlier this week, we learned that consumer confidence is at an 18-year high. This is a very good environment in which to be a stock investor. Now let’s look at our Buy List earnings report from this week.

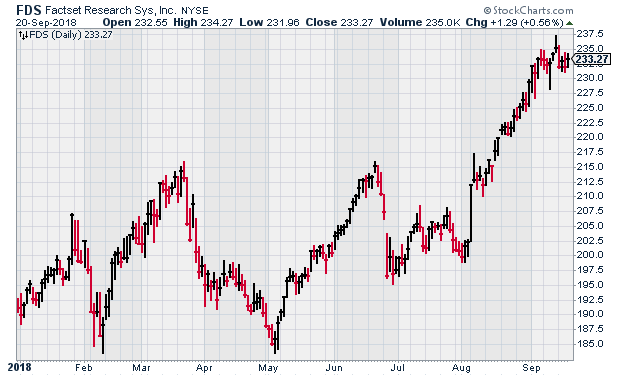

FactSet Earned $2.20 per Share for Its Fiscal Q4

On Tuesday, FactSet (FDS) said it earned $2.20 per share for its fiscal Q4 which ended in August. If you’re not familiar with FactSet, they help Wall Street professionals crunch all the numbers they need to make investment decisions. It’s a very profitable business.

The Q4 earnings were one penny below expectations. Personally, I had been expecting even more. In the after-hours market, FDS was down sharply. Once trading started on Wednesday, FDS was down as much as 6.2%. But as the day wore on, the shares acted better. By the closing bell, FDS had lost 1.9%.

Let’s dig into the numbers a little bit, because they’re not so bad. For the quarter, organic revenue rose 5.3% to $347.1 million. Annual Subscription Value (ASV), which is the key stat for FDS, increased to $1.39 billion. Organic ASV was up 5.7%. FDS noted that the increase for Q4 was $38.6 million which is the highest in the company’s history. Adjusted operating margin, another key stat I like to watch, inched up to 31.3% compared with 31.2% last year.

“We are proud to have reached many milestones in fiscal 2018. We celebrated 40 years as a company with 38 years of consecutive revenue growth and 22 years of consecutive adjusted EPS growth. This quarter we had the highest reported quarterly ASV in our history. We enter fiscal 2019 with strong momentum and an expanding suite of innovative workflow solutions to drive our growth plans,” said Phil Snow, FactSet CEO.

For Q4, FactSet’s effective tax rate was 18.0% compared with 25.3% a year ago. That’s largely due to the tax cuts. Their client count now stands at 5,142. That’s an increase of 167 in the past three months. User count increased by 2,391 to 91,897. Annual client retention is greater than 95% of ASV. As a percentage of clients, annual retention is 91%. Net cash provided by operating activities was $106.3 million, compared with $100.2 million a year ago. Quarterly free cash flow rose 2.1% to $91.2 million.

For the entire year, FactSet’s organic revenues rose 5.6% to $1.35 billion while ASV rose 5.7% to $1.39 billion. Earnings increased 16.7% to $8.53 per share. Previously, the company said its earnings range was $8.37 to $8.62 per share, so things seem to be working according to plan.

Annual client count increased by 8.4% or 398 during the year while users grew by 3.4% or 3,051 from the prior year. Free cash flow increased 24.1% to $352.1 million.

Now let’s look at guidance for fiscal 2019 (ending next August). FactSet expects earnings to range between $9.45 and $9.65 per share. That’s not a bad increase over this year. Wall Street had been expecting $9.61 per share. FactSet sees organic ASV rising by $75 million to $90 million in 2019, and they see operating margins between 31.5% and 32.5%. That’s pretty good.

Shares of FDS have pulled back over the last few days, but I’m not particularly concerned. The stock had a very strong rally during much of August. FactSet remains a buy up to $242 per share.

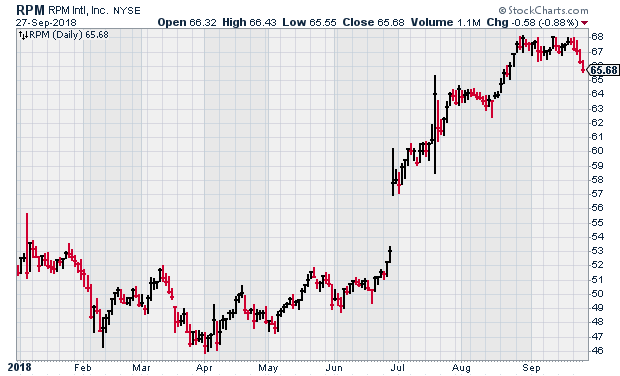

RPM International Earnings Preview

RPM International (RPM) is due to report its fiscal Q1 earnings on Wednesday, October 3 before the opening bell. Speaking of stocks giving us a head-fake after earnings, RPM was a perfect example three months ago.

After the last earnings report, RPM opened down 4%. This is why we eschew trading. It’s too irrational. Fortunately, the market came to its senses, and RPM closed higher by 5.3%. The difference between the daily high and low price was nearly 12%.

For fiscal Q4, RPM earned $1.05 per share which was 13 cents below Wall Street’s consensus. The company blamed “higher raw-material costs and extended winter weather.” Rust-Oleum had to shutter two manufacturing facilities. RPM’s consumer segment was especially weak, while the industrial unit fared better.

As part of the deal with Elliott Management, RPM is going to unveil a comprehensive business plan later this year. I think that may involve major divestments. Because of this, the company will forgo any EPS guidance. Sales-wise, for 2019, RPM expects a mid-single-digits sales increase for its industrials unit. For the consumer unit, they see an increase of mid- to upper-single digits.

The consensus on Wall Street expects Q1 earnings of 88 cents per share which is a slight increase over the 86 cents per share they earned in last year’s Q1.

One last note. I’m dropping the Buy Below on Carriage Services (CSV) down to $24 per share. This move reflects the stock’s recent weakness.

That’s all for now. The fourth quarter kicks off next week. With the start of the new month, we’ll get some key economic reports. On Monday, the ISM report comes out. The last ISM was the strongest in 12 years. Then on Wednesday, ADP will release its report on private payrolls. Then on Friday we’ll get the September jobs report. The unemployment rate is close to a multi-decade low. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Syndication Partners

I’ve teamed up with Investors Alley to feature some of their content. I think they have really good stuff. Check it out!

Buy These 3 High Yield Clean Energy Stocks While They’re Still Cheap

Renewable energy sources are a growing part of the total energy sector assets. In the first half of 2018 solar and wind projects accounted for 42% of new power capacity in the U.S. Overall, solar and wind have grown to provide 10% of the total U.S. electric power generation. The power industry uses high yield investment vehicles as one funding source for the growth in renewable energy. These stocks can put a solar powered lift in your dividend income.

A type of income stock often called a Yieldco has been widely used to own renewable power producing assets. These companies have been formed by energy project developers and electricity utilities to help fund development.

The system roughly works like this. A company constructs a new wind power windmill project or solar array. Once it is near completion the development company will sell the projects future power production on a long term contract with a utility company or other energy user. Once its up and operating, with power contracted to an end user, the new project will be sold to a Yieldco that is affiliated with the developer. The Yieldco gets an asset with a long term revenue stream to support dividend payments. The developer gets paid back for the development and can put the capital to work developing another project.

The result is that Yieldco stocks are steady dividend payers with good prospects for dividend growth.

Here are three to consider for your income portfolio.

Are Charismatic Founders a Curse or a Blessing For Investors?

Throughout U.S. corporate history, there have been some very memorable company founders such as JP Morgan and Henry Ford. Fast forward a few decades and we have Bill Gates and Steve Jobs.

I suspect though that history will less kindly remember the current batch of founders including the likes of Travis Kalarick of Uber, John Schnatter of Papa John’s and Elon Musk of Tesla. These entrepreneurs succeeded initially, but failed to come up with a succession plan to transition to a professional management. And worse, they’ve stayed on too long, becoming both an embarrassment and a hindrance to their respective companies.

In the case of Musk and Tesla, he may have let his strong dislike of people pointing out the flaws in his company’s finances go so far that he may have committed a crime with his “funding secured” tweet. The U.S. government has launched a criminal investigation into Tesla.

All of the above examples are companies that failed at the very important task of planning for the replacement of an executive who serves not only as the company’s manager but also as its pitchman and inspiration. These companies should all have planned for a staged withdrawal with the elevation of several key executives to key positions. But Tesla for example, cannot seem to keep an executive for more than a few months.

However, there are companies that have done things right. Here are two examples.

-

Morning News: September 28, 2018

Eddy Elfenbein, September 28th, 2018 at 7:03 amGlobal M&A Volume Flattens in Third Quarter as Trade Tensions Loom

Corbyn Went to Brussels and Forgot to Bring Euros

Japan’s Embrace of Bilateral Trade Talks With U.S. Spares It From Tariffs

Hank Paulson Says China Trade War Risks Long-Term U.S. Pain

Leveraged-Loan Buyers Clamor for Crumbs as Market Heats Back Up

Tesla CEO Elon Musk Is Sued by the SEC in a Move that Could Oust Him

Tesla’s Board Backs Musk After SEC Sues, Seeks His Ouster

Insider Trading’s Odd Couple: The Goldman Banker and the NFL Linebacker

Why Comcast Is Paying Dearly for Britain’s Sky

How Apple Thrived in a Season of Tech Scandals

Arby’s Former CEO is Building a Fast-Food Empire

Lawrence Hamtil: The Remarkable Resilience of the Refining Industry

Joshua Brown: Should Retail Investors Get Expanded Access to Private Markets?

Jeff Carter: Sometimes A Quest to “Do Good” Does A Lot of Bad

Be sure to follow me on Twitter.

-

Morning News: September 27, 2018

Eddy Elfenbein, September 27th, 2018 at 7:14 amWhy India Will Struggle to Join Iran’s Sanctions Busters

Italy Budget Uncertainty Returns to Haunt Europe

For the Fed, Ignoring Trump Is Good Policy

Google Dodges Questions About China During Senate Privacy Hearing

Watchdogs Can’t Handle Wall Street’s Riskiest Loans

Jeff Bezos’s Space Startup to Supply Engines for Boeing-Lockheed Rocket Venture

Apple: Is Warren Buffett Right?

Ford, BP Call Out Costs of Trump Administration’s Trade Policies

The World’s Leading Electric-Car Visionary Isn’t Elon Musk

McDonald’s President Reveals How the Chain is Managing a Potential Fast-Food Identity Crisis

The Hot Property That’s Next on Tech’s Agenda: Real Estate

Cheaper Battery Is Unveiled as a Step to a Carbon-Free Grid

Cullen Roche: 2 Reasons the Surging Deficit Worries Me

Michael Batnick: Animal Spirits: Looming Disaster

Howard Lindzon: Make Me Laugh and Smile and Facebook is The New Tobacco

Be sure to follow me on Twitter.

-

The Fed Raises Rates

Eddy Elfenbein, September 26th, 2018 at 2:04 pmOnce again, the Federal Reserve raises interest rates. Here’s the policy statement:

Information received since the Federal Open Market Committee met in August indicates that the labor market has continued to strengthen and that economic activity has been rising at a strong rate. Job gains have been strong, on average, in recent months, and the unemployment rate has stayed low. Household spending and business fixed investment have grown strongly. On a 12-month basis, both overall inflation and inflation for items other than food and energy remain near 2 percent. Indicators of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that further gradual increases in the target range for the federal funds rate will be consistent with sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective over the medium term. Risks to the economic outlook appear roughly balanced.

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 2 to 2-1/4 percent.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

Voting for the FOMC monetary policy action were: Jerome H. Powell, Chairman; John C. Williams, Vice Chairman; Thomas I. Barkin; Raphael W. Bostic; Lael Brainard; Richard H. Clarida; Esther L. George; Loretta J. Mester; and Randal K. Quarles.

Here are the Fed’s updated economic projections.

-

Morning News: September 26, 2018

Eddy Elfenbein, September 26th, 2018 at 7:16 amIn a U.S. Manufacturing Hub, No Illusions About Tariffs and Jobs

Nafta’s Fate Hangs on a Four-Letter Word: Milk

Fed Dots to Harden Views for December Move: Decision-Day Guide

Trump Has a Weapon to Lower Oil Prices and It’s Not His Twitter

As Debt Rises, the U.S. Government Will Soon Spend More on Interest Than on the Military

One Reason for Slow Wage Growth? More Benefits

The Man Behind a $1 Trillion Wealth Fund Braces for Trade Rupture

Instagram Founders’ Exit Means No One to Challenge Zuckerberg

The Continental Shock of the Kors-Versace Deal

Daimler Names R&D Head as Next CEO, Zetsche to Become Chairman

Nike Buzz Created Tough Expectations

Hold the Donuts, Says Newly Named Dunkin

Nick Maggiulli: Why You Don’t Know the Price Until You Sell

Ben Carlson: Undervalued Financial Advice

Be sure to follow me on Twitter.

-

FactSet Earned $2.20 per Share

Eddy Elfenbein, September 25th, 2018 at 8:10 amFactSet‘s (FDS) earnings are out, and the company earned $2.20 per share for their fiscal fourth quarter. That was one penny below expectations.

Let’s dig into the numbers a little bit because they’re not so bad. For the quarter, organic revenue rose 5.3% to $347.1 million. Annual Subscription Value (ASV), which is a key stat for FDS, increased to $1.39 billion. Organic ASV was up 5.7%. FDS noted that the increase for Q4 was $38.6 million, which is the highest in the company’s history. Adjusted operating margin, another key stat, inched up to 31.3% compared with 31.2% last year.

“We are proud to have reached many milestones in fiscal 2018. We celebrated 40 years as a company with 38 years of consecutive revenue growth and 22 years of consecutive adjusted EPS growth. This quarter we had the highest reported quarterly ASV in our history. We enter fiscal 2019 with strong momentum and an expanding suite of innovative workflow solutions to drive our growth plans,” said Phil Snow, FactSet CEO.

For Q4, FactSet’s effective tax rate was 18.0% compared with 25.3% a year ago. That’s largely due to the tax cuts. Their client count now stands at 5,142. That’s an increase of 167 in the past three months. User count increased by 2,391 to 91,897. Annual client retention is greater than 95% of ASV. As a percentage of clients, annual retention is 91%. Net cash provided by operating activities was $106.3 million compared with $100.2 million a year ago. Quarterly free cash flow rose 2.1% to $91.2 million.

For the entire year, FactSet’s organic revenues rose 5.6% to $1.35 billion while ASV rose 5.7% to $1.39 billion. Earnings increased 16.7% to $8.53 per share. Previously, the company said their earnings range was $8.37 to $8.62 per share, so things seem to be working out according to plan.

Annual client count increased by 8.4% or 398 during the year, while users grew by 3.4% or 3,051 from the prior year. Free cash flow increased 24.1% to $352.1 million.

Now let’s look at some estimates for fiscal 2019 (ending next August). The company expects earnings to range between $9.45 and $9.65 per share. That’s not a bad increase over this year. Wall Street had been expecting $9.61 per share.

FactSet sees organic ASV rising by $75 million to $90 million in 2019, and they see operating margins between 31.5% and 32.5%.

Update: FDS dropped sharply today. At one point, it was down 6.2% on the day. The shares recovered some and closed down 1.90%.

-

Morning News: September 25, 2018

Eddy Elfenbein, September 25th, 2018 at 6:57 amJamie Dimon Says It Will Take 25 Years for Bailouts to Be Forgiven

Future of Last U.S. Nuclear Plant Remains Uncertain Amid Talks

Despite Big Merger, Investors Still Cautious on Gold Mining Companies

The Future of 5G Mobile Data Could Hinge on a Battle Over Utility Pole Fees

Instagram’s Co-Founders to Step Down From Company

Comcast Knows What It Is. Investors Aren’t So Sure.

Sears CEO Proposes Plan to Avoid Bankruptcy, as Options and Cash Run Low

Fish-Oil Heart Medicine Is Rarest of Drug Breakthroughs

Starbucks Plans ‘Significant Changes’ to Company’s Structure

Walmart Requires Lettuce, Spinach Suppliers to Join Blockchain

Why Tilray’s Plunge Continued Today

Tokyo Whale Sells $230 Million of Bitcoin in Mt. Gox Wind-Down

Michael Batnick: The Next Generation

Howard Lindzon: Momentum Monday…The Calm Before The Calm?

Jeff Carter: You Always Will Have a Job if You Can Sell

Be sure to follow me on Twitter.

-

The Silent Bear Market

Eddy Elfenbein, September 24th, 2018 at 10:59 amWhile the S&P 500 continues to be near all-time record highs, there’s a group of stocks, many related to trade, that are languishing well below their highs.

The Wall Street Journal notes that stocks like Harley-Davidson, Whirlpool, Stanley Black & Decker and Caterpillar haven’t done much of anything. The list also includes consumer staples like General Mills and our own, J.M. Smucker. Apple and Amazon make up 30% of the S&P 500’s gain so far this year.

Investors have ranked a trade war as the top tail risk to the markets for four consecutive months, Bank of America Merrill Lynch said in its September survey of global fund managers. Fears that tighter trade policies could crimp growth also have hit fund managers’ global outlooks, with 24% of investors expecting global growth to slow in the next year, up from 7% in August.

“There’s a number of money managers who’ve been hesitant to be involved with the [companies] that are going to be potentially affected by the tariffs, whether they’ll be able to export fewer goods or be buying less from China,” said Mark Grant, managing director and chief global strategist at B. Riley FBR Inc.

Sentiment towards tech may be changing. September could be the worst month for tech stocks since March. In the modern economy, it’s hard to draw a bright line between trade stocks and non-trade stocks. To a certain extent, they’re all trade stocks.

-

Morning News: September 24, 2018

Eddy Elfenbein, September 24th, 2018 at 7:04 amApp-Only Banks Rise in Europe and Aim at Traditional Lenders

America’s Libor Alternative Is Gaining Traction on Wall Street

Home Modems, Routers Hit by U.S. China Tariffs as ‘Smart’ Tech Goods Escape

JPMorgan Is Strategizing in Case of ‘a Major Miscalculation From Sanctions’ by Trump

Congress May Force Airlines to Install Bigger Seats, Ban Involuntary Bumping

In Beating Disney for Sky, Comcast Remains in the Game

Barrick Gold, Randgold in Advanced Talks on Merger

Singapore Imposes Fines, Restrictions Over Uber-Grab Deal

Google CEO: ‘We Do Not Bias Our Products to Favor Any Political Agenda’

Dell to Interview Banks for IPO in Lieu of Tracking-Stock Acquisition

Michael Kors Is Close to Buying Versace for $2 Billion

Harley Is Winning in Europe—Without a Trade War

Ben Carlson: The New Gilded Age?

Howard Lindzon: BTFD China? and Congrats Microsoft

Jeff Carter: Democratizing Food

Be sure to follow me on Twitter.

-

CWS Market Review – September 21, 2018

Eddy Elfenbein, September 21st, 2018 at 7:08 am“Investing is the intersection of economics and psychology.” – Seth Klarman

On Thursday, the S&P 500 closed at 2,930.75, another record high. In the last 31 months, the index is up over 60%. But here’s an interesting fact about this rally. Despite steadily rising share prices, the bull market hasn’t had much impact on public opinion. My friend Gary Alexander recently noted:

A survey by Betterment Research from July 31 to August 6, 2018 polled 2,000 Americans over age 18 and found that 48% believed that stocks had been flat (had gained nothing) over the past 10 years. Another 18% believed stocks had declined. The truth? The S&P and the Dow are both up over 120% from July 31, 2008 to July 31, 2018, and the Nasdaq is up 230%.

That’s amazing. How can so many people be so wrong? I honestly don’t know, but my hunch is that the public is still turned off by Wall Street. I can certainly understand why. The financial crisis was bitter and painful. I also think the media shares in the blame. Unfortunately, fear and alarmism sell.

As disciplined investors with a long-term focus, we should always maintain a healthy skepticism of the market, but that can’t lead us to ignore basic facts: this is a very good time to be a patient investor. The economy is improving. Jobless claims just fell to another 49-year low, and our world-famous Buy List is up over 10% YTD. Our strategy is working.

In this week’s CWS Market Review, I want to help you sort out this mess and give you a plan for the rest of the year. First, we’ll focus on next week’s Fed meeting. The central bank will almost certainly raise interest rates. I’ll tell you what to expect and what it all means. I’ll also preview next week’s earnings report from FactSet. FDS is a 21% winner for us this year. Plus, I’ll update you on Wabtec’s dramatic week. But first, let’s see what Jay Powell and his friends at the Fed have in store for us.

What to Expect at Next Week’s Fed Meeting

The Federal Reserve meets again next week, on Tuesday and Wednesday, and this will be a biggie. This will be one of the Fed’s two-meetings, which means it will be followed by a press conference from Jay Powell, the Fed Chair. The Fed participants will also update their economic projections.

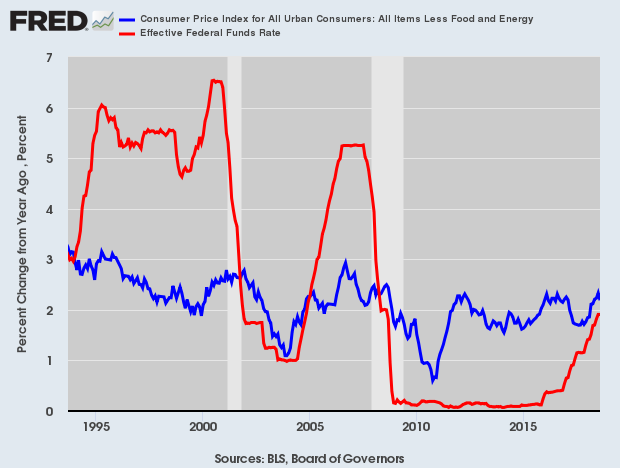

The Fed is widely expected to raise interest rates. This will be their eighth rate hike in the last three years. It will bring the Fed funds target range up to 2% – 2.25%. There are a few important points here. The first is that this rate hike will bring the real Fed funds rate (meaning after inflation) to 0%. Real Fed funds have been consistently negative since the economy went kablooey ten years ago. In fact, real Fed funds have been negative almost non-stop since 9/11 except for a three-year period before the financial crisis.

Here’s the Fed funds rate (in red) along with the core inflation rate (in blue):

The equation is very simple: when real short-term rates are low, especially negative, it’s very good news for stocks. And they have been. That won’t magically change next week, but the free-money window is beginning to close. We can also see the effect by looking at the yield curve. The spread between the two- and ten-year Treasury yields is now down to 26 basis points. In other words, about one more Fed rate hike. This week, the two-year Treasury yield got as high as 2.81%. It hasn’t been that high in more than a decade. For some context, at one point in 2011, the two-year was yielding just 0.16%. The world has come back to normal.

I want to be careful in how I word this. A negative yield curve is on balance bad for stocks and the economy, but it’s not a tripwire. Instead, it’s a warning sign. For example, the 2/10 spread went negative in late 2005. The stock market and economy chugged along for two more years. They key with a flat yield curve is to be more cautious but not run away at the first signs of trouble.

The other important aspect of this meeting will be the Fed’s economic projections. Let me preface by saying that the Fed’s predictions are notoriously bad. I mean, even for economists. Still, it’s important to know what the Fed is thinking.

In the last projections, a narrow majority at the Fed saw the need for two more rate hikes this year (meaning one in September and another in December). Frankly, I’ve been a doubter on a December hike, but it looks like I’ve been outvoted. The futures market places the odds at 90% for a December hike.

But what about 2019? Well, here’s where it gets a little tricky. The Fed sees three more hikes next year, but the futures market isn’t so sure, and I share their skepticism. The futures see a March hike, and maaaaybe another one before the end of the year. At next week’s meeting, it’s very possible that the Fed might pare back its forecasts for 2019. The distribution of the Fed’s projections are fairly dispersed, so it wouldn’t take a lot to bring the median vote down to two hikes for 2019. If that happens, it would be a good signal for the market.

The reason this is important is that an overly-vigilant Fed has historically been a big threat to bull markets. The Fed also always overdoes it. Once the yield curve goes negative, then we want to start paying close attention to knock-on effects. At the top of the list is the housing market. To reiterate, we’re in a good spot right now, but mistakes from the Fed could lead to unpleasantness in 2019. Now let’s take a look at our one Buy List earnings report for next week.

Preview of FactSet’s Earnings Report

FactSet (FDS) has been a nice 21% winner for us this year (see below). Because the company follows an off-cycle reporting schedule (its fiscal year ends in August), it’s due to report its fiscal Q4 earnings on Tuesday, September 25.

I’m expecting more good news from FactSet. In June, they reported fiscal Q3 earnings of $2.18 per share, which beat Wall Street’s estimate by five cents per share. Q3 was a solid quarter for them. Revenues increased 8.9% to $339.9 million compared.

Thanks to those good numbers, FactSet also bumped up its full-year earnings forecast. The old range was $8.35 to $8.55 per share. The new range is $8.37 to $8.62 per share.

FactSet’s CEO said, “We are making progress integrating and cross selling our acquisitions resulting in important wins this quarter, particularly within Analytics. We continue to innovate with the launch of the Open:FactSet marketplace and enhancing our risk offering. We believe we have a solid pipeline for the fourth quarter and expect to finish fiscal 2018 in our guidance range.”

With FactSet, the key stat to watch is Annual Subscription Value or ASV. For Q3, ASV rose 5.3% to $1.36 billion. At the end of the quarter, FactSet had 4,975 clients. That’s an increase of 80 clients. User count rose by 860 to 89,506.

One weak spot is operating margin. For Q3, their operating margin fell to 31.0% compared with 31.9% a year ago. The company blamed the fall on restructuring actions and certain one-time administrative expenses.

The CEO said, “We made good progress on our annual and medium term goals this quarter. The restructuring actions we initiated this quarter help us to optimize costs and benefit margins in the future. With our balanced capital allocation framework including our robust share buyback program and an increase in dividends, we continued to return value to shareholders.”

Let’s run some math. For the first nine months of the fiscal year, FDS has earned $6.34 per share. The current outlook implies Q4 earnings of $2.03 to $2.28 per share. Wall Street had been expecting $2.19 per share, but they’ve now raised their expectations to $2.21 per share. I’m expecting something closer to $2.25 per share. I’ll be curious to hear what they have to say for Q1 guidance. FactSet remains a very solid stock.

Update on Wabtec

Shares of Wabtec (WAB) got slammed for a 12.4% loss last Friday after an analyst at JP Morgan questioned whether the math adds up on WAB’s merger deal with GE.

The company played it smart. They shot back with a press release on Friday stating that the merger deal “continues to make progress,” and that they expect it to be complete by early 2019.

Then on Monday, WAB amended their proxy which noted that they expect to see a “minor” (their word) $63 million adjustment in revenue and EBIT for next year. Bear in mind, WAB expects free cash flow of $6 billion from 2019 to 2022. They also said that adjustment will have “no material effect in future years.” They stood by their other financial targets for the deal. The stock rallied 7% on Monday.

Barron’s quoted two analysts who are optimistic on Wabtec. Both of them noted that the freight-rail business has been above expectations. I’m still a fan of this company. Wabtec remains a buy up to $111 per share.

One final note. Sherwin-Williams (SHW) keeps busting through our Buy Below prices. At the start of July, our Buy Below on SHW was $400. The stock ran straight through that, so I raised it to $414. Soon it crashed through that. I then raised our Buy Below to $460 per share. I thought that would give us some breathing room. Not quite. Here we are a few weeks later, and SHW is at $478. It’s not a bad problem to have. SHW is up $100 in four months. This week, I’m lifting my Buy Below on Sherwin-Williams to $498 per share.

That’s all for now. The third quarter comes to a close next week. The big story will be the Fed meeting. Look for the latest policy statement on Wednesday afternoon. We’ll also get updated economic projections. Then on Thursday, we’ll get the latest report on durable goods. Also on Thursday, the government will update the Q2 GDP report. The initial report showed growth of 4.1% which was later revised to 4.2%. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

P.S. Join me for next week’s “Alpha Call.” On Wednesday, September 26 at 4 pm ET, I’ll be talking markets with market veteran Louie Navellier. Follow this link to register.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His