Author Archive

-

Forbes Names Signature Bank as America’s Best Bank

Eddy Elfenbein, January 7th, 2015 at 8:36 amFrom Forbes:

The top U.S. bank this year is New York-based Signature Bank SBNY -1.17%. The full-service commercial bank started in 2001 and has grown to $26 billion in assets with 27 private client offices throughout the New York-metro area. “There is a lot of runway in the New York metro area for us to grow,” says CEO Joe DePaolo in extolling the NYC market. There are $1.4 trillion in deposits in New York banks, almost three times the next biggest metro of Philadelphia.

Signature focuses primarily on the needs of privately owned businesses with at least $20 million in revenue. But DePaolo says the bank will also target a law firm with $2 million in billings because it has a $35 million escrow account. “This is where we thrive because that client gets lost with the big institution,” he says. Signature’s attention to law firms helped it get named Best Business Bank by the New York Law Journal this year in their annual reader survey.

Signature has racked up an impressive financial performance. It has posted 20 straight quarters of record earnings. Return on average equity of 13.8% over the last 12 months ranks fifth among the 100 largest banks. The bank also ranks in the top five for nonperforming assets as a percent of total assets (0.1%), nonperforming loans (NPLs) as a percent of total loans (0.15%) and reserves as a percent of NPLs (634%). While many banks are struggling to increase revenue, Signature posted growth of 21% over the past year. Wall Street recognizes the level of Signature’s asset quality and performance, as the stock trades at 2.5 times book value, third most expensive among the 100 biggest banks.

-

Looking Ahead to Friday’s Jobs Report

Eddy Elfenbein, January 7th, 2015 at 8:14 amThe big December jobs report is due out on Friday morning. The government will release several key figures regarding the employment situation including nonfarm payrolls, labor force participation and the unemployment rate.

This report will be one of the first times in a long time that I’m not so concerned about non-farm payrolls. Those have been growing at a steady clip for several months, and I expect that to continue. What I’m looking for now is to see an increase in average hourly earnings (AHE).

Until now, workers haven’t seen much of an increase in their wages. In fact, AHE has largely tacked 2% growth which is basically inline with inflation. The AHE for November wasn’t too bad. I’ll be very curious to see if there was more in December.

The other number to see will be hours worked. This is one of those reports that sounds counter-intuitive. You might think you’d want to see fewer hours worked, but in terms of the macro economy, we want to see more. More hours and at higher wages.

While inflation is still quite modest, an increase in wages will probably foreshadow an increase in consumer prices. As long as oil and other commodities are plunging, inflation isn’t a problem. The strong dollar has probably given the Fed a few more months to forego raising rates, but any sign of inflation will change that.

During the recession, the U-6 unemployment rate got a lot of attention. This is the regular unemployment rate plus part-time for economic reasons and marginally attached workers. This was considered a broader and more accurate gauge of the jobs market. In April 2010, it hit 17.2%%. It’s been dropping and for November, the U-6 was 11.4%. It’s taken a while but the jobs market is beginning to get back to something vaguely normal.

-

Morning News: January 7, 2015

Eddy Elfenbein, January 7th, 2015 at 7:06 amParis on Terrorism Alert After 11 Killed in Magazine Attack

Deflation Hits Eurozone as Energy Prices Fall

Bank of England Minutes Underscore Turbulence of Financial Crisis

Unemployment at Record Low in Germany, Record High in Italy

Deal-Maker Macron Woos Vegas by Pledging France Can Change

Greece 10-year Borrowing Rate Tops 10% on Eurozone Exit Fears

Iran Accuses Saudis of Oil Conspiracy

How $50 Oil Changes Almost Everything

Solutions Needed in India For A Better Society

J.C.Penney Proves Skeptics Wrong With A Holiday Sales Surprise

Boeing Reports Record Orders, Deliveries to Airlines in 2014

Intel Budgets $300 Million for Diversity

Why Your Cable Bill Is Going Up Again in 2015 – Sports

Cullen Roche: The Austerity That Never Happened

Roger Nusbaum: How Can The Bond Bull Keep Going?

Be sure to follow me on Twitter.

-

The 10-Year Is Back Below 2%

Eddy Elfenbein, January 6th, 2015 at 3:24 pmAnother strange trading day. The S&P 500 dropped as low as 1,992.44 which was a loss of 1.39%, but it’s recovered some since then. The major banks have been hit especially hard. The Financial Sector was down the most, although our own Wells Fargo ($WFC) was one of the better banks, meaning down the least. Small-caps are also feeling the pain.

But the real action has been in the bond pits. I used to think there was no way that bond yields would come back to their July 2012 lows. Those were multi-decade lows. Now I’m not so sure. The 10-year yield is back below 2%. The 10-year got as low as 1.89% today. The 30-year got down to 2.47%. The spread between the 10- and 30-year is now less than 60 basis points which it hasn’t been in five years. My favorite indicator, the 2-10 spread, is at a two-year low (but still far from pre-recession levels).

Crude oil is down yet again. The black stuff for February delivery got down to $47.55 per gallon.

-

Morning News: January 6, 2015

Eddy Elfenbein, January 6th, 2015 at 7:02 amEuro Area Menaced by Relapse Risk as ECB Weighs Action

Samaras Faces Greek Voters Skeptical of His Euro-Exit Warnings

Japan’s Big Firms Celebrate Cheaper Crude

As Oil Drops Below $50, Can There Be Too Much of a Good Thing?

Free Money in Bond Markets Shows Global Economy Still Struggling

Goldman Sachs Says JPMorgan Chase Should Be Broken Up

Verizon Is Said to Approach AOL for Possible Takeover, Venture

Amazon Again Emphasizes Sellers’ ‘Record-Setting Year’ But Fails To Open Kimono

Hyundai Motor to Spend $74 Billion Over 4 Years on Facilities, R&D

Dish Network Unveils Sling, a Streaming Service to Rival Cable (and It Has ESPN)

Coach to Buy Luxury Shoe Maker Stuart Weitzman

Hackers Steal $5 Million From Major Bitcoin Exchange

Why New Credit Cards May Fall Short on Fraud Control

Jeff Carter: When Will US Companies Scream About The Dollar?

John Hempton: A Comment on Current Chinese Vs. WWII Iron Ore Demand

Be sure to follow me on Twitter.

-

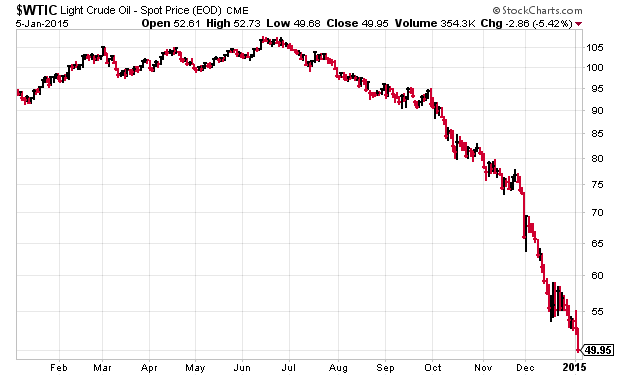

Oil Drops Below $50

Eddy Elfenbein, January 5th, 2015 at 10:18 pmIt’s not over yet for oil. Spot West Texas closed below $50 per barrel today. The close was $49.95. This is the first time oil has closed below $50 in five-and-a-half years.

It was a rough day for stocks as well. The S&P 500 dropped for the fourth day in a row, something it had not done all of last year.

The S&P 500 lost 1.83% today but the losses were heavily concentrated in energy. The Energy Sector of the S&P 500 lost 3.99% today. In contrast, Consumer Staples were down just 0.77% and Healthcare was down 0.61%. This is, of course, why they’re called defensive sectors.

There are also renewed worries that Greece might leave the euro. As an interesting historical side note, in the mid-19th century, there was an attempt at monetary union among several European countries.

The Latin Monetary Union grew to include France, Belgium, Italy, Switzerland, Spain, Greece, Romania, Bulgaria, Venezuela, Serbia and San Marino. In 1908, Greece was temporarily kicked out of the union for diluting its gold coins.

-

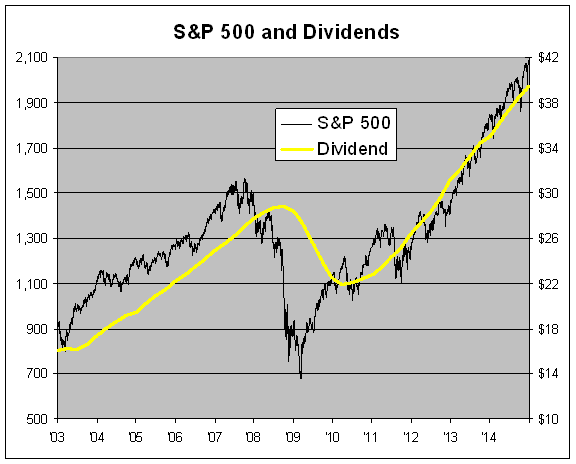

Dividends Rose 10% in Q4

Eddy Elfenbein, January 5th, 2015 at 1:08 pmI often tell investors that dividends are easily the most important and most overlooked part of investing. Dividends tend to grow and reinvesting those dividends gets you more shares which begets you still more dividends. The effect may be small each week, but it adds up. Consider that in the last 20 years, the S&P 500 price index is up 348%. But the Total Return Index, which includes dividends, is up 555%.

The numbers are in for the fourth quarter and dividends paid out by companies in the S&P 500 rose by 9.96% over last year’s Q4. That’s actually the second-slowest growth rate in the last 16 quarters. The slowest was Q4 of 2013 which came one year after the big dividend surge in late 2012 to pay out dividends before the tax rate went up. In the last four years, dividends paid out by the S&P 500 are up more than 73%.

For the year, the S&P 500 paid out $39.44 in index-adjusted dividends. That’s an increase of 12.72% over 2013. But here’s what interesting: The S&P 500 price index rose 11.39% last year. In other words, dividends grew faster than prices. That means the S&P 500 ended the year with a slightly higher dividend yield than it started the year. Despite all the talk of a stock bubble, at least one measure of the market’s valuation moved lower.

As I’ve pointed out before, for most of the last 12 years, the S&P 500 hasn’t strayed very far from a trailing dividend yield of 2%. The only exception was during the worst of the financial crisis, but once the storm passed, the market quickly moved back to 2%. It’s also interesting that the dividend payout ratio (the percent of profits being paid out as a dividend) has hovered near 33% for the last two years.

-

Ford Down 3.5% Today

Eddy Elfenbein, January 5th, 2015 at 10:28 amShares of Ford are down 3.5% after the stock was downgraded by an analyst at Citigroup. The analyst kept the price target the same at $17 per share but lowered Ford to “neutral” from “buy.” Ford also reported December sales growth of 1%.

Ford Motor posted its best December sales figure since 2005. Ford’s U.S. sales rose 1% to 220,671 vehicles. But overall 2014 sales were flat vs. a year ago at 2.48 million vehicles on a planned 15% reduction in daily rental sales.

(…)

“Demand for the all-new F-150 also is very high, and it now is the fastest-turning vehicle in Ford showrooms, averaging just five days on dealer lots in December,” said John Felice, Ford vice president, U.S. Marketing, Sales and Service in the release.

F-Series sales total 74,355 vehicles in December and 753,851 vehicles for 2014 as lower gas prices helped boost demand for larger trucks and SUVs.

-

The Euro Falls to Nine-Year Low

Eddy Elfenbein, January 5th, 2015 at 9:46 amThe euro (aka the German peso) has fallen to a nine-year low against the dollar. The currency dropped down to $1.1924. Today we learned that German inflation is at its weakest since 2009. Brent crude just dropped below $55 per barrel, and West Texas is below $52.

-

Explaining Our Methodology

Eddy Elfenbein, January 5th, 2015 at 9:24 amI wanted to make a few comments about our Buy List’s methodology. As I’ve found out, if you have a publicly-available free Buy List that’s done very well, some unpleasant people will call you a fraud or a liar. They’ll question your math or a bunch of other things.

There’s not much you can do about cranks, but I’ve always gone out of my way to make our Buy List as transparent as possible. The set-and-forget rules are about as simple as you can get. I even take the extra step of making my new buys public two weeks before the changes take effect. You’d think that would mollify some people. Not so.

Long story short, it’s a good time to restate what my goal is with the Buy List. I want to show regular investors that a disciplined approach can prosper and even beat the market. That’s why I do a few other things with my Buy List that I don’t often highlight. For example, I try to make sure that the Buy List is easy to replicate. This characteristic doesn’t get as much attention as it should. We don’t select any oddball foreign stocks or trade in unusual commodities or currencies. We don’t use margin, options or ETFs. There’s no shorting. Nor do we speculate on the North Bulgarian exchange in New Zealand pesos or anything like that. Around here, we keep it straightforward.

Also, nearly all our companies are at least mid-caps, and many are large-cap blue-chip names. We don’t dabble in IPOs or thinly traded pink sheets. I always have the average investor in mind. The companies on our Buy List also have pretty standard operations. And of course, we keep our trading to a minimum.

At the beginning of each year, I assume the Buy List is equally weighted among the 20 stocks. I also treat each year’s Buy List as a separate entity. In other words, we start over again at 0% at the start of each year. Here I can understand how some people might disagree with this decision.

My rationale is this: if I treated the Buy List as one never-ending unit, I could show that we’ve made huge long-term gains in a stock like Fiserv, but very few blog readers have been following us the entire time. It’s a question of making things as comprehensible as possible for as many folks as possible. (Honestly, I can see tracking the Buy List either way, but I think the separate year-by-year approach is the easiest and fairest.)

Occasionally I list our full nine-year total returns, but that means an investor rebalanced the portfolio at the end of each calendar year. I don’t think it’s wrong to do this, but I want to make it clear what it means.

Every so often, we’ve had spin-offs or buyouts. I try to deal with these as best I can. Years ago, we got cash for our Biomet shares. I distributed that cash into the 19 remaining Buy List stocks. When Golden West Financial was bought out, we got shares of Wachovia, and that became a new member of the Buy List.

I’ve always been careful to detail on the blog how all the calculations are made. Later this year, eBay will hopefully spin off PayPal. If all goes well, we’ll get the shares, and I’ll decide what to do with them in December. As always, the decisions I make are designed to make investing as easy as possible for average investors.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His