Author Archive

-

eBay Earned 69 Cents Per Share for Q2

Eddy Elfenbein, July 16th, 2014 at 4:30 pmFor Q2, eBay ($EBAY) earned 69 cents per share which beat estimates by a penny per share. Quarterly revenue rose 13% to $4.37 billion. The stock initially dropped after-hours, but now seems to be up a bit.

For Q3, eBay expects earnings between 65 and 67 cents per share, and revenue between $4.3 billion and $4.4 billion. Wall Street had been expecting 70 cents per share on $4.42 billion.

For the full year, eBay reiterated their guidance of $2.95 to $3.00 per share. They lowered the top-end of their revenue guidance to $18.3 billion from $18.5 billion. The low-end is still $18 billion.

-

Humphrey–Hawkins on SNL

Eddy Elfenbein, July 16th, 2014 at 1:03 pmJanet Yellen has been giving her Humphrey-Hawkins testimony this week. The name comes from the Humphrey-Hawkins Full Employment Act which mandates that the Fed Chair go to Capitol Hill twice a year and explain what they’re doing.

Interestingly, the bill started out as a Keynesian effort, but it gradually became taken over by monetarist ideology. The bill lasted in Congress for a few years, and was eventually passed after Hubert Humphrey died in 1978.

The bill was referred to in a classic Saturday Night Live skit:

SNL-No-Math from Dez on Vimeo.

-

IBM Is Starting to Break Out

Eddy Elfenbein, July 16th, 2014 at 12:13 pmIBM ($IBM) has not been a strong performer this year, but it’s perked up recently. Earnings are due out tomorrow.

The stock is getting a nice bounce today on news that it’s teaming up with Apple on business software:

In a deal that could deepen Apple’s sales to corporations and strengthen IBM’s position in business software, the two companies announced a wide-ranging partnership intended to spread advanced mobile and data analysis technology in the corporate world.

IBM and Apple have been working together on the venture for several months, and they are jointly working on more than 100 business software programs developed exclusively for Apple’s iOS operating system and for use on iPhones and iPads. The applications will be tailored for use in industries including retail, health care, transportation, banking, insurance and telecommunications.

“We’ve already seen some unbelievable work,” Timothy D. Cook, Apple’s chief executive, said in an interview conducted along with Virginia M. Rometty, IBM’s chief executive. Mr. Cook described the venture with IBM as “a landmark partnership” for both companies.

-

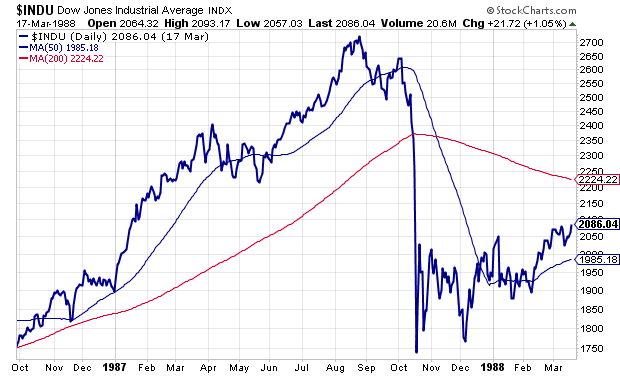

For the Patient, the Crash Wasn’t a Crash

Eddy Elfenbein, July 16th, 2014 at 10:52 amWhenever the stock market rallies, we start hearing how the current environment is “just like 1987.” These comparisons are pretty silly because the investing environment is always changing. It’s never the same.

But even if we consider a major crash, we have to remember how strongly the market rallied before the 1987 crash, and how well it recovered. If we dial back the clock to a year prior to Black Monday, and go out five months after the crash, the market looks just fine. If a modern Rumpelstiltskin has slept for several months, he would not have been surprised by the market’s move.

Consider these numbers: From September 29, 1986 to March 17, 1988, the Dow rose by 18.8%. Sure, that includes an historic drop in between. You can also say I’m cherry-picking, but so is looking at a one-day crash.

My point is that if an investor is patient, even major crashes don’t look so bad.

-

Industrial Production Rose 0.2% in June

Eddy Elfenbein, July 16th, 2014 at 9:59 amThe stock market is up in early trading today. The S&P 500 has been as high as 1,983.94 which is just below its intra-day high of 1,985.59 from July 3. Yesterday we got as high as 1,982.52.

I don’t claim to be a technical analyst but chart readers pay attention to these “resistance levels.” If an index isn’t able to break through, that can be a negative sign. But the big news this week is earnings season. According to numbers from Bloomberg, the S&P 500 is expected to show an earnings increase of 4.5% for Q2, while sales are expected to rise by 3.1%.

On the economic front, the Federal Reserve reported that Industrial Production rose by 0.2% in June. They also revised the May number up to 0.5%. IP rose at an annualized rate of 5.5% during Q2, and Manufacturing Production increased at a 6.7% annualized clip.

The big news for our Buy List today will be eBay’s (EBAY) earnings which are due after the close. Wall Street expects 69 cents per share. Time Warner (TWX) is doing very well today after the company shot down a buyout offer from Rupert Murdoch (aka Twentieth Century Fox). He’s offering $85 per share for TWX which closed yesterday at $71.01. It’s been as high as $83.20 today.

-

Morning News: July 16, 2014

Eddy Elfenbein, July 16th, 2014 at 7:35 amWhy the BRICS Development Bank Trumps Even the World Bank

EU Readies Russia Sanctions Amid U.S. Pressure on Ukraine

British Pay Growth Slows to Record Low Even as Jobless Rate Falls

Fed Tries New Role as Lines Judge for Markets

F.C.C. Is Deluged With Comments on Net Neutrality Rules

Time Warner Shares Soar on Report of Murdoch Bid

Bank of America’s Earnings Decline 43% on Legal Costs

Goldman Sachs Q2 Earnings Impress Investors on Higher Revs

Imperial Tobacco to Snag U.S. E-Cig Lead Thanks to Deal

BlackRock Second-Quarter Profit Climbs 11% as Assets Rise

Slump in Advertising Sales Dragged Quarterly Revenue Down at Yahoo

Gtech Agrees to Buy Slot-Machine Maker IGT for $4.7 Billion

Red Flags: Alibaba’s Ma and Ma’s Private Equity Firm

Cullen Roche: Thoughts on “Artificial Interest Rates”

Jeff Carter: Who Is Right; Santelli or Liesman?

Be sure to follow me on Twitter.

-

Janet Yellen’s Testimony

Eddy Elfenbein, July 15th, 2014 at 10:53 amTwice a year, the Chair of the Federal Reserve heads to Capitol Hill to testify on monetary policy. Each time, it’s for two days — once in the House and again in the Senate.

One year, I went down to see it in person. I even got the seat directly behind Bernanke. It’s actually pretty dull in person, and our members of Congress ask rather pointless questions.

Here’s a look at Janet Yellen’s testimony for today:

Chairman Johnson, Ranking Member Crapo, and members of the Committee, I am pleased to present the Federal Reserve’s semiannual Monetary Policy Report to the Congress. In my remarks today, I will discuss the current economic situation and outlook before turning to monetary policy. I will conclude with a few words about financial stability.

Current Economic Situation and Outlook

The economy is continuing to make progress toward the Federal Reserve’s objectives of maximum employment and price stability.In the labor market, gains in total nonfarm payroll employment averaged about 230,000 per month over the first half of this year, a somewhat stronger pace than in 2013 and enough to bring the total increase in jobs during the economic recovery thus far to more than 9 million. The unemployment rate has fallen nearly 1-1/2 percentage points over the past year and stood at 6.1 percent in June, down about 4 percentage points from its peak. Broader measures of labor utilization have also registered notable improvements over the past year.

Real gross domestic product (GDP) is estimated to have declined sharply in the first quarter. The decline appears to have resulted mostly from transitory factors, and a number of recent indicators of production and spending suggest that growth rebounded in the second quarter, but this bears close watching. The housing sector, however, has shown little recent progress. While this sector has recovered notably from its earlier trough, housing activity leveled off in the wake of last year’s increase in mortgage rates, and readings this year have, overall, continued to be disappointing.

Although the economy continues to improve, the recovery is not yet complete. Even with the recent declines, the unemployment rate remains above Federal Open Market Committee (FOMC) participants’ estimates of its longer-run normal level. Labor force participation appears weaker than one would expect based on the aging of the population and the level of unemployment. These and other indications that significant slack remains in labor markets are corroborated by the continued slow pace of growth in most measures of hourly compensation.

Inflation has moved up in recent months but remains below the FOMC’s 2 percent objective for inflation over the longer run. The personal consumption expenditures (PCE) price index increased 1.8 percent over the 12 months through May. Pressures on food and energy prices account for some of the increase in PCE price inflation. Core inflation, which excludes food and energy prices, rose 1.5 percent. Most Committee participants project that both total and core inflation will be between 1-1/2 and 1-3/4 percent for this year as a whole.

Although the decline in GDP in the first quarter led to some downgrading of our growth projections for this year, I and other FOMC participants continue to anticipate that economic activity will expand at a moderate pace over the next several years, supported by accommodative monetary policy, a waning drag from fiscal policy, the lagged effects of higher home prices and equity values, and strengthening foreign growth. The Committee sees the projected pace of economic growth as sufficient to support ongoing improvement in the labor market with further job gains, and the unemployment rate is anticipated to continue to decline toward its longer-run sustainable level. Consistent with the anticipated further recovery in the labor market, and given that longer-term inflation expectations appear to be well anchored, we expect inflation to move back toward our 2 percent objective over coming years.

As always, considerable uncertainty surrounds our projections for economic growth, unemployment, and inflation. FOMC participants currently judge these risks to be nearly balanced but to warrant monitoring in the months ahead.

Monetary Policy

I will now turn to monetary policy. The FOMC is committed to policies that promote maximum employment and price stability, consistent with our dual mandate from the Congress. Given the economic situation that I just described, we judge that a high degree of monetary policy accommodation remains appropriate. Consistent with that assessment, we have maintained the target range for the federal funds rate at 0 to 1/4 percent and have continued to rely on large-scale asset purchases and forward guidance about the future path of the federal funds rate to provide the appropriate level of support for the economy.In light of the cumulative progress toward maximum employment that has occurred since the inception of the Federal Reserve’s asset purchase program in September 2012 and the FOMC’s assessment that labor market conditions would continue to improve, the Committee has made measured reductions in the monthly pace of our asset purchases at each of our regular meetings this year. If incoming data continue to support our expectation of ongoing improvement in labor market conditions and inflation moving back toward 2 percent, the Committee likely will make further measured reductions in the pace of asset purchases at upcoming meetings, with purchases concluding after the October meeting. Even after the Committee ends these purchases, the Federal Reserve’s sizable holdings of longer-term securities will help maintain accommodative financial conditions, thus supporting further progress in returning employment and inflation to mandate-consistent levels.

The Committee is also fostering accommodative financial conditions through forward guidance that provides greater clarity about our policy outlook and expectations for the future path of the federal funds rate. Since March, our postmeeting statements have included a description of the framework that is guiding our monetary policy decisions. Specifically, our decisions are and will be based on an assessment of the progress–both realized and expected–toward our objectives of maximum employment and 2 percent inflation. Our evaluation will not hinge on one or two factors, but rather will take into account a wide range of information, including measures of labor market conditions, indicators of inflation and long-term inflation expectations, and readings on financial developments.

Based on its assessment of these factors, in June the Committee reiterated its expectation that the current target range for the federal funds rate likely will be appropriate for a considerable period after the asset purchase program ends, especially if projected inflation continues to run below the Committee’s 2 percent longer-run goal and provided that inflation expectations remain well anchored. In addition, we currently anticipate that even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the federal funds rate below levels that the Committee views as normal in the longer run.

Of course, the outlook for the economy and financial markets is never certain, and now is no exception. Therefore, the Committee’s decisions about the path of the federal funds rate remain dependent on our assessment of incoming information and the implications for the economic outlook. If the labor market continues to improve more quickly than anticipated by the Committee, resulting in faster convergence toward our dual objectives, then increases in the federal funds rate target likely would occur sooner and be more rapid than currently envisioned. Conversely, if economic performance is disappointing, then the future path of interest rates likely would be more accommodative than currently anticipated.

The Committee remains confident that it has the tools it needs to raise short-term interest rates when the time is right and to achieve the desired level of short-term interest rates thereafter, even with the Federal Reserve’s elevated balance sheet. At our meetings this spring, we have been constructively working through the many issues associated with the eventual normalization of the stance and conduct of monetary policy. These ongoing discussions are a matter of prudent planning and do not imply any imminent change in the stance of monetary policy. The Committee will continue its discussions in upcoming meetings, and we expect to provide additional information later this year.

Financial Stability

The Committee recognizes that low interest rates may provide incentives for some investors to “reach for yield,” and those actions could increase vulnerabilities in the financial system to adverse events. While prices of real estate, equities, and corporate bonds have risen appreciably and valuation metrics have increased, they remain generally in line with historical norms. In some sectors, such as lower-rated corporate debt, valuations appear stretched and issuance has been brisk. Accordingly, we are closely monitoring developments in the leveraged loan market and are working to enhance the effectiveness of our supervisory guidance. More broadly, the financial sector has continued to become more resilient, as banks have continued to boost their capital and liquidity positions, and growth in wholesale short-term funding in financial markets has been modest.Summary

In sum, since the February Monetary Policy Report, further important progress has been made in restoring the economy to health and in strengthening the financial system. Yet too many Americans remain unemployed, inflation remains below our longer-run objective, and not all of the necessary financial reform initiatives have been completed. The Federal Reserve remains committed to employing all of its resources and tools to achieve its macroeconomic objectives and to foster a stronger and more resilient financial system.Thank you. I would be pleased to take your questions.

-

Morning News: July 15, 2014

Eddy Elfenbein, July 15th, 2014 at 6:44 amGerman Bunds Rise as Confidence Gauge Drops More Than Forecast

BOJ Says Inflation to Stay Above 1% Despite Cut in GDP Forecast

China Taps Six State-Owned Firms for Reforms

Janet Yellen Steps Up to the Plate

Citi Reaches $7 Billion Pact on Mortgage Probe

Albemarle and Rockwood Announce Merger to Create a Premier Specialty Chemicals Company

Yahoo Set for Ho-Hum Q2 Report

Ping An Bank Seeks as Much as $4.8 Billion to Boost Capital

Airbus Secures $11.8 Billion SMBC Aviation A320 Order

Air Lease Said to Order 26 Jetliners From Boeing

Reynolds American to Buy Lorillard in $27.4 Billion Deal

Inequality Piketty Doesn’t Examine is U.S. Human Capital

Cullen Roche: The Importance of Learning to Be Wrong

Joshua Brown: Collision Course

Be sure to follow me on Twitter.

-

Pizza is Money

Eddy Elfenbein, July 14th, 2014 at 2:34 pm -

Liesman Vs. Santelli

Eddy Elfenbein, July 14th, 2014 at 2:21 pmHere’s a very silly discussion between Steve Liesman and Rick Santelli. I used to have respect for Santelli but this performance is embarrassing. He’s been wrong on everything.

(h/t Barry Ritholtz)

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His