Author Archive

-

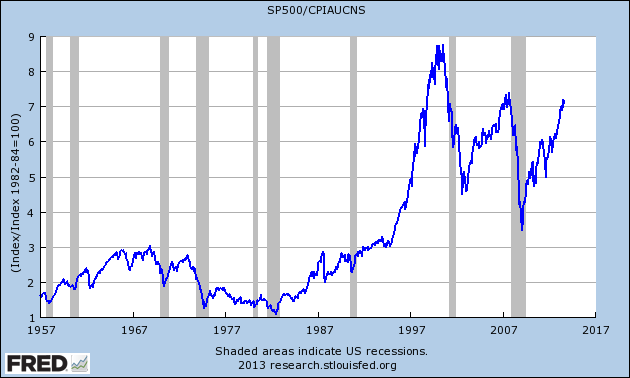

The S&P 500 Matches Inflation-Adjusted High

Eddy Elfenbein, October 30th, 2013 at 11:56 amGreat news! Adjusted for inflation, the S&P 500 has done nothing in the past six years! And it’s taken a lot for us to get there.

This morning, the government released the inflation report for September. I had to do a little massaging of the numbers, but if we assume the inflation trend that we had in September continues in October, then the S&P 500 just surpassed its inflation-adjusted peak from October 2007.

Note that this is just the S&P 500 and it doesn’t include dividends. All things being equal, you can expect the market’s dividend rate to follow the inflation rate fairly closely. While we’re above the 2007 peak, the S&P 500 is still about 18.5% below the inflation-adjusted peak from 2000.

We can never say for certain where the inflation-adjusted index is because there’s some lag time before the inflation report comes out. Here’s the latest FRED chart which goes from 1957 through September 2013. The next data point should reflect the six-year high.

It’s interesting to see that the 2009 low nearly matched the 1966 high.

-

WEX Inc. Earns $1.29 Per Share

Eddy Elfenbein, October 30th, 2013 at 10:57 amMore good earnings news today. This morning, WEX Inc. ($WEX) reported Q3 earnings of $1.29 per share. That’s 10 cents more than estimates. Three months ago, WEX said that earnings for Q3 would be between $1.16 and $1.23 per share.

Quarterly revenue jumped 19% to $191.5 million. These are very good numbers. The shares are currently up 5% this morning. WEX’s CEO had good things to say in today’s report.

“We continue to experience momentum throughout our business, driven by the solid execution of our long-term strategy. For the quarter, revenue increased 19% year-over-year and was towards the high-end of our guidance, while adjusted net income, increasing 20%, exceeded our expectations. Our results were driven by robust volume growth, Other Payments growth, foreign exchange rate contributions and expense management,” commented Michael E. Dubyak, WEX’s chairman and chief executive officer.

“We continue to see ongoing expansion in our domestic fleet business as we realize synergies from Fleet One and further bolster our competitive position. Furthermore, investments in our virtual card product are continuing to generate positive returns as we penetrate attractive geographies including Europe, Asia Pacific and South America. Looking towards the future, we expect to continue to leverage the foundations we are building and our dynamic pipeline to drive growth as we close out the year,” concluded Mr. Dubyak.

For Q4, WEX sees earnings coming in between $1.04 and $1.12 per share. Wall Street had been expecting $1.11 per share. WEX also raised their full-year guidance range to $4.37 to $4.44 per share. The earlier range was $4.27 to $4.37 per share.

-

Morning News: October 30, 2013

Eddy Elfenbein, October 30th, 2013 at 6:47 amChina Official PMI Seen Hitting 18-Month High in October

Spain Exits Two-year Recession as Rajoy Seeks Recovery

German Unemployment Rises a Third Month as Growth Slows

RBS Said to Review Currency-Trading Practices Amid Probe

World’s First Bitcoin ATM Launched in Canada

Chocolate Factory, Trade War Victim

Consumer Confidence in U.S. Slumps by Most Since August 2011

The President Wants You to Get Rich on Obamacare

Housing Prices in U.S. Cities Rise by Most Since Early 2006

Barclays Profit Rises to $1.2 Billion But Fixed Income Trading Slumps

Linkedin’s Conservative Forecast Gives Pause To Sizzling Stock Surge

Sears Weighs Spinoff of Lands’ End

Honda Q2 Net Up 42% on U.S. Sales Rise, Slightly Below Forecast

Joshua Brown: The Starbucks Global Takeover

Howard Lindzon: Being Wrong Works at Scale…Hedge Funds and Bank of America

Be sure to follow me on Twitter.

-

AFLAC Earns $1.47 Per Share, Raises Dividend 5.7%

Eddy Elfenbein, October 30th, 2013 at 12:04 amAfter the closing bell, AFLAC ($AFL) reported Q3 earnings of $1.47 per share which was one penny below Wall Street’s forecast. In July, the company gave us a range for Q3 of $1.41 to $1.51 per share, so at least AFLAC is hitting its own guidance. The problem continues to be the yen/dollar exchange rate which knocked 21 cents per share off AFLAC’s earnings last quarter.

If you ignore the exchange rate issue, AFLAC’s operations are doing just fine. The company also gave forward guidance which assumes a yen/dollar rate between 95 and 100. Here are the details: AFLAC narrowed its full-year 2013 guidance to $6.16 to $6.21 per share. The previous range was $5.83 to $6.37 per share. For Q4, AFLAC expects earnings between $1.38 and $1.43 per share. Wall Street had been expecting $1.42 per share. Excluding the exchange rate, AFLAC aims to grow operating earnings by 4% to 7% this year.

AFLAC also gave its first guidance for 2014, again assuming a 95 to 100 exchange rate. For next year, they see earnings coming in between $6.28 and $6.52 per share. They’re aiming to grow operating earnings by 2% to 5% next year.

I have to stress that this is all in earnings-per-share because AFLAC plans to buy back a whole lot of shares. The company plans to buy $800 million of shares this year, and another $800 million to $1 billion next year.

AFLAC also raised their dividend by 5.7%. The quarterly payout rises from 35 to 37 cents per share. This is the 31st year in a row that AFLAC has raised their dividend.

-

Fiserv Earns $1.56 Per Share

Eddy Elfenbein, October 29th, 2013 at 4:31 pmFiserv ($FISV) just reported third-quarter earnings of $1.56 per share which was five cents more than Wall Street’s consensus.

From the CEO:

“Results for the quarter were solid across the board and in-line with our performance expectations for the full year,” said Jeffery Yabuki, President and Chief Executive Officer of Fiserv. “Strength in our payments businesses along with continued strong sales is compelling evidence of the market-leading differentiation and value embedded in our solutions.”

More highlights from the quarter:

Adjusted earnings per share increased 24 percent in the quarter to $1.56 and increased 18 percent in the first nine months of 2013 to $4.39, as compared with the prior year periods.

Free cash flow grew 21 percent in the first nine months of 2013 to $598 million compared with $496 million in the prior year period.

Adjusted operating margin was 30.5 percent in the quarter, an increase of 60 basis points compared with the third quarter of 2012, and increased 50 basis points to 29.8 percent in the first nine months of 2013, compared with the prior year period.

Now the important stuff — forward guidance:

Fiserv expects its full year 2013 adjusted earnings per share from continuing operations to be in a range of $5.94 to $6.02, or growth of 17 to 19 percent over 2012. The company expects full year adjusted revenue growth of approximately 10 percent, and adjusted internal revenue growth of approximately 3 percent.

“We remain on track to achieve our 2013 financial objectives and have meaningful momentum as we head into 2014,” said Yabuki.

That’s an increase of ten cents per share to the low-end of their range. Fiserv has already made $4.39 per share for the first three quarters, so that implies a range of $1.55 to $1.63 per share for Q4. The shares are up a bit after hours.

-

Earnings Call Harris Corp.

Eddy Elfenbein, October 29th, 2013 at 1:08 pmHere are some highlights from today’s earnings call from Harris ($HRS):

Operating income was $64 million and operating margin was strong at 15.5%, as a result of very good program performance.

Turning to Slide 8. Free cash flow was strong at $139 million versus $77 million last year, and capital expenditures were $33 million compared to $44 million in the prior year.

During the quarter, we repurchased about 1.7 million shares of our common stock for a total cash outlay of $100 million, and our effective tax rate for the quarter was 32.2%.

Moving to Slide 9. Fiscal 2014 guidance remains unchanged at a range of $4.65 to $4.85 per diluted share for our income from continuing operations, and a revenue decline of 1% to 3% compared to the prior year. We’ve also made no changes to segment information, which is detailed on this slide.

It sounds a little dull, but I like to hear companies say that guidance is unchanged. That just means they’re executing as expected. That’s good news.

-

What Happened to Exxon Mobil?

Eddy Elfenbein, October 29th, 2013 at 10:16 amWhat happened to Exxon Mobil ($XOM)? The oil giant used to dominate the market, but the stock has been a major laggard during this bull market. It’s not just the sector; XOM has lagged the XLE as well (see below).

Exxon is still a big kid. They have a market cap of $390 billion which is second only to Apple ($AAPL) in the S&P 500. But it’s not that far ahead of Google ($GOOG) which comes in at $340 billion. If XOM had merely kept pace with the S&P 500, their market cap would be over $700 billion today.

Is XOM a good buy here? That’s hard to say. The stock is probably lower than where it ought to be, but it’s not clear how much long-term potential there is. XOM is going for 11 times next year’s earnings, but those earnings are projected to be less than last year’s profit.

You can often find good buys by looking at what strong stocks have lagged the market for a few years. XOM certainly fits that. But I’m not convinced the stock is a bargain just yet.

-

Harris Earns $1.18 per Share

Eddy Elfenbein, October 29th, 2013 at 9:51 amNice earnings beat for Harris ($HRS) this morning. For its fiscal Q1, the company earned $1.18 per share which was five cents more than expectations. Quarterly revenues dropped 5.5% to $1.19 billion which was $30 million below consensus.

Harris also reaffirmed their guidance for this year (their fiscal year ends in June). They see full-year earnings ranging between $4.65 and $4.85 per share. Wall Street expects $4.74 per share.

The company generated free cash flow (net cash provided by operating activities less capital expenditures) of $139 million in the first quarter compared with $77 million in the prior year. Free cash flow was 109 percent of income from continuing operations.

“First quarter operating performance provided a positive start to our fiscal year,” said William M. Brown, president and chief executive officer. “Previous restructuring actions together with our continuing progress on operational excellence allowed us to post solid results in the quarter, despite the tough government spending environment.”

HRS has been as high as $61.94 this morning which is up 4.3% from yesterday’s close. The stock is currently off its high.

AFLAC ($AFL) and Fiserv ($FISV) are due to report after the closing bell.

-

Morning News: October 29, 2013

Eddy Elfenbein, October 29th, 2013 at 6:29 amRajan Raises Key Rate to Fight Inflation as Cash Curbs Eased

EU Delays Bank Capital Rule Following Nordic Protest

Hopes of Market Reforms in China Tempered by Political Realities

The White House May End US Spying On Friendly Foreign Leaders

Medicare Chief Is About to Get Grilled on Obamacare

UBS Profitability Goal Delayed by Capital Demands

Ron Paul: Son Will Hold Up Yellen to Get Fed Bill Vote

Deutsche Bank Profit Slumps 94% on 1.2 Billion-Euro Charge

Lloyds Looks to Reinstate Dividend

Infosys Said to Reach Settlement With U.S. on Visa Probe

Apple’s Profit Falls Despite Higher Sales of iPhones

BP Ups Asset Sales, Dividend as Big Oil Q3 Kicks Off

Goldman Pushes Junior Investment Bankers to Take Weekends Off

Roger Nusbaum: Are We A Country of Moochers?

Cullen Roche: The Debt Bad Guys

Be sure to follow me on Twitter.

-

Updates on CR and CMI

Eddy Elfenbein, October 28th, 2013 at 1:09 pmEarlier this month, I noted that Global Payments ($GPN) rose sharply. I had highlighted GPN thirteen months ago, and the stock has done very well since then.

In that same post from September 2012, I wrote: “Cummins ($CMI) seems to be a very attractive stock. I’m surprised the stock is so low. The same could be said for Crane ($CR).”

Not exactly sophisticated analysis, but I was right again. Here’s how those stocks have performed compared with the S&P 500:

As of today, both stocks are about fairly priced. I no longer see a big bargain here.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His