-

Hurray for Spin-Offs

Posted by Eddy Elfenbein on September 10th, 2010 at 11:13 amIn general, I like spin-offs and hate mega-mergers: which leads me to smoking stocks and they’ve been smoking lately. Altria (MO) is at a 52-week high and it’s close to an all-time high.

The company spun-off Kraft (KFT) in 2007. Kraft was already publicly traded but MO decided to ditch its remaining 88% in the company. Then in 2008, MO spun-off Philip Morris (PM).

Here’s a look at how they’ve done:

Every stock has beaten the S&P 500 which is the gold line at the bottom. Kraft is the red line, Philip Morris is the blue and Altria is the black.

Mega-mergers sound great. They make a lot of news, but the results are usually pretty unimpressive. Spin-offs, however, can often be good places to find cheap stocks. I should add that after the spin-off, MO was kicked out of the Dow which is another index it has outperformed. -

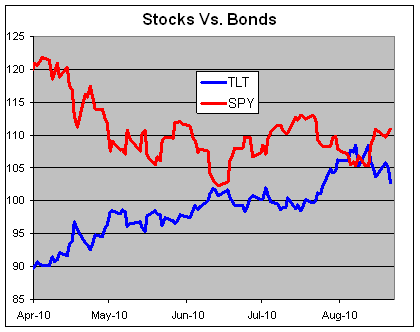

Stocks Aganst Bonds

Posted by Eddy Elfenbein on September 10th, 2010 at 10:10 amHere’s an interesting chart. This shows how the S&P 500 ETF (SPY) has done compared with the Long-Term Treasury ETF (TLT). Since April, they’ve become almost mirror images of each other.

I ran the numbers and found that since April 21, the daily correlation between the two is -0.55. In other words, when stocks go up, long-term bonds go down. When bonds go down, long-term stocks go up. Now let’s place “generally” before those last two statements, but you get the idea.

What does it mean for the market? It’s hard to say. It usually means that capital is undecided. Money has a simple rule: It goes where it’s treated best. Right now, equity and debt are slugging it out.

The 10-year bond has been taking a hit recently but that’s hardly a shocker considering how low the yield went. On August 25, the intra-day yield dropped to just 2.42%. Think about that for a moment. At that rate, even after 10-years, you still won’t have made 25% on your dough. The yield has crept up and it just jumped above 2.8% today.

I’m happy to see the market go up, but we need to bear in mind that it’s only coming at the bond market’s expense. Personally, I can live with that. But if I had my preference, I’d like to see new money come in from commodities that would fuel both asset classes. -

Morning News: September 10, 2010

Posted by Eddy Elfenbein on September 10th, 2010 at 9:41 amFOREX-Dollar bounce loses steam, Swissie slides

Nokia Hires Microsoft’s Elop as CEO to Reverse Losses to Apple

China Posts $20 Billion Trade Surplus as U.S. Seeks Yuan Gains

Goolsbee to Lead Panel on Economy

Dubai World Close to Agreement on Debt

Ozawa win may push Bank of Japan to buy government bonds

Deutsche Bank Said to Weigh Share Sale of Up to $11.4 Billion

SEC Examines Funds of Hedge Funds -

Oh Melissa

Posted by Eddy Elfenbein on September 9th, 2010 at 11:26 am

(HT: TBI) -

Stick a Fork In Us, We’re Done

Posted by Eddy Elfenbein on September 9th, 2010 at 10:20 amToday’s must-read item is “Paradise Lost: Why Fallen Markets Will Never Be the Same” by Ian Bremmer and Nouriel Roubini. Be warned: It checks in at over 4,000 words.

I’m generally pretty skeptical of these kinds of things, but I wanted to pass it your way. If I have any brilliant insights, I’ll add them later.

I’m afraid I’m not swayed by their argument: or rather, I supposed I’m relieved.

Update: Ok, I just finished the article. For one, the title seems to clash with the body. Far from telling us that markets will never be the same, they simply list many changes and problems in the world economy.

I also think they have a very “guys-in-suits-centric” view of the world. Just because the kind of folks invited to G-20 meetings disagree with one another or don’t have answers to the world’s problems doesn’t mean these problems are intractable. Nor does it even mean the problems will last.

The problem with this article is that it’s long on concepts and flushed out with strawmen, trendy buzzwords (nonpolar!) and the assumption that current trends will last: but it’s very short on support.

Felix Salmon has more. -

Stocks Up on Jobless Claims

Posted by Eddy Elfenbein on September 9th, 2010 at 9:49 amIt doesn’t seem like Thursday. Such are the joys of holiday shortened weeks. The stock market is doing well so far this morning.

As I mentioned before, we seem to be stuck in a trading range. The S&P 500 has bobbed between 1020 and 1130 for over three months. Thanks to the last few days, plus today, we may soon challenge the upper end of that range. Let’s hope we do because nearly everything the market gained in July was taken away by August. I don’t want September to be another July (doesn’t that sound like the title of an old song?).

We can never know exactly why the market is up on a certain day, but the good news this morning is that there was a drop in jobless claims. First-time claims fell to 451,000 last week from a revised 478,000 a week earlier. The Street had been expecting claims to fall to 470,000.

Frankly, I don’t put a great deal of faith in jobless claims. This number comes out every Thursday and it contains a lot of what stats folks call “noise.” On top of that, nine states didn’t give numbers this week due to the Labor Day holiday. I think this is simply a case of the market wanting to rally and if that’s the excuse, so be it.

I see that all of our Buy List stocks are rallying (except NICK and MOG-A haven’t traded yet). AFLAC (AFL) has been as high as $51.27 and it’s close to making a four-month high. -

Morning News: September 9, 2010

Posted by Eddy Elfenbein on September 9th, 2010 at 9:23 amBritish Regulators Fine Goldman over SEC Tourre Fraud Investigation

Britain Keeps Rates on Hold Amid Worries About Global Recovery

OECD Says Slowdown ‘More Pronounced’ Than Anticipated

Norway Buys Greek Debt as Sovereign Wealth Fund Sees No Default

Falling Rates Aid Debtors, but Hamper Savers

U.S. Slides in World Economic Forum’s Rankings

Bank of Korea Keeps Interest Rate Near Record Low

Verizon Guy Tells Me The Customer Is No Longer Always Right -

Intel’s Margins Under Pressure

Posted by Eddy Elfenbein on September 8th, 2010 at 2:07 pmHere’s a good segment from CNBC:

-

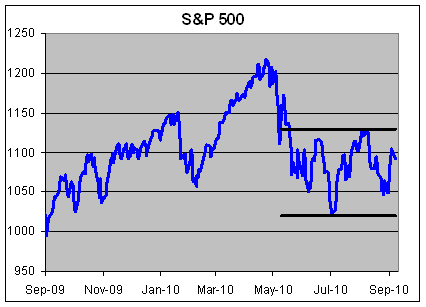

A Range-Bound Market

Posted by Eddy Elfenbein on September 8th, 2010 at 11:47 amFor 78 straight sessions, the S&P 500 has closed between 1022 and 1128.

It looks like today will be day #79. -

Hulbert: What Stocks Do Well from Deflation

Posted by Eddy Elfenbein on September 8th, 2010 at 11:10 amFrom MarketWatch:

By Tuesday’s close, the Dow Jones Industrial Average had fallen 107 points, erasing nearly half of its big gain during the previous session.

But are investors acting rationally when they dump stocks because of deflationary concerns?

Though it would certainly appear that they are, I’m not so sure. The job of a contrarian is to question widely-held assumptions, and the notion that deflation would be bad for stocks is so universally held these days that virtually no one appears to be subjecting it to any critical scrutiny.

One firm that has nevertheless done so is Ned Davis Research, the quantitative research firm. Lance Stonecypher, Senior Sector Strategist for the firm, recently analyzed sector performance during previous periods of significant deflation, both in this country as well as in Japan. Since there haven’t been many such periods, his conclusions of necessity must remain somewhat tentative.

But some fairly consistent themes nevertheless did emerge.

Perhaps the primary conclusion that Stonecypher reached was that, during past deflationary periods, the industry groups that performed the best fell into two categories Necessity and Defensive. Examples include Consumer Staples and Health Care.

Though Ned Davis Research doesn’t provide specific stock recommendations, examples of widely-held stocks in these two industry groups include Johnson & Johnson, Procter & Gamble, PepsiCo, Coca-Cola, and McDonald’s.

Digging further, Stonecypher also found that small-cap stocks have tended to markedly lag the large-caps during deflationary periods. The most pronounced periods of deflation in U.S. history came during the early 1930s, the late 1930s, and immediately after World War II. On average in those three cases, he found, small-cap stocks lagged the large caps by 13% per year.

Finally, Stonecypher suspects that the companies whose stocks perform the best during deflationary periods are those with the lowest debt/equity ratios. This makes sense in theory, he argues, because deflation makes it more difficult for debt to be repaid. (He was unable to confirm this theory, however, since he doesn’t have industry sector debt-to-equity data for the 1930s.)

The bottom line? It is possible to be gravely concerned about the prospects of outright deflation and still invest in equities. If you harbor such concerns but don’t want to give up completely on stocks, you might want to shift some of your equity holdings into the Consumer Staples and Health Care sectors, as well as shunning small-caps in favor of large-cap stocks with the lowest debt-to-equity ratios.During the 1960s and 1970s, stocks like Wal-Mart (WMT) did very well by offering price-conscious consumers a place to go in order to fight inflation. While WMT’s pricing policies are controversial now, the company prospered thanks to its market position during the U.S. economy’s 15-year bout with inflation. The overall U.S. stock market didn’t do well at all.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His